just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

After a strong run through early 2024, the US dollar is starting to show signs of fatigue and this time, it's not just about yields. Over the past week, the greenback has edged lower toward key technical support levels, with the DXY drifting back to its April lows. At the heart of the move is growing discomfort around US trade policy specifically, the return of tariff escalation under Donald Trump’s second-term agenda.

Markets had been cautiously optimistic in May, buoyed by hopes of de-escalation in the US-China trade standoff. But that narrative is quickly unravelling. Trump’s latest decision to double tariffs on steel and aluminium imports to 50%, effective from today (June 4), has rattled risk sentiment and reminded investors just how unpredictable the US policy landscape can be. Trade talks with Beijing have reportedly stalled again, and the lack of any meaningful progress has reintroduced uncertainty at a time when the global cycle is already under pressure.

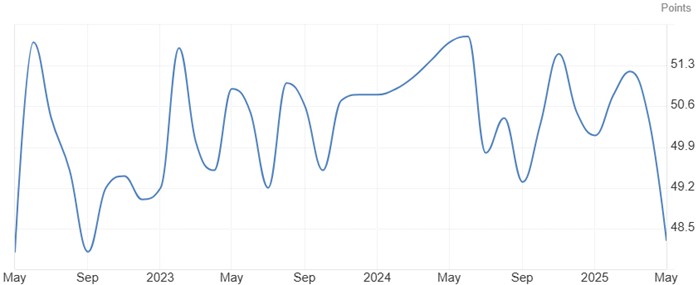

China’s economy is showing the strain. The latest Caixin manufacturing PMI fell sharply in May, dropping to 48.3 its lowest level since September 2022. The report blamed deteriorating external demand and mounting pressure on supply chains. In contrast, China’s official PMI showed a modest improvement. But that divergence likely reflects the different timing of the surveys one capturing the immediate shock of tariffs, the other picking up a more lagged sentiment bounce after the temporary US-China trade truce earlier in May.

Back in the US, the ISM manufacturing survey also disappointed. It slipped to 48.5 in May, the fourth consecutive decline, pointing to a cooling in business confidence. After a solid rebound late last year, momentum is now fading again undermined by cost uncertainty, slower hiring, and global demand softening. While some macro data has held up reasonably well (surprise indices have even flipped back into positive territory), traders are becoming more selective in pricing further Fed rate cuts.

At one point, markets were pricing in 75bps of easing this year. That’s now been trimmed to around 50bps, reflecting a Fed that’s cautious but not panicking. A decisive shift in expectations would likely require a material weakening in the labour market. This makes the upcoming US nonfarm payrolls report a critical data point consensus is looking for a softer 130k print for May, which would be below trend but not weak enough to force the Fed’s hand before September.

So, we find ourselves in an awkward middle ground: softer growth data but not a full breakdown, Trump reintroducing tariff risk, and a Fed that’s still playing the long game. This mix is proving toxic for the dollar especially against currencies like the yen.

After slipping to 146.28 last week, USD/JPY has now dropped back to the 142 handles. And it’s not just a dollar story. Japanese government bond (JGB) yields remain firm, especially at the long end. The 30-year yield is consolidating just below 3%, and recent auctions are pointing to healthy domestic demand. In fact, the latest 10-year JGB auction saw a bid-to-cover ratio jump to 3.66 well above its one-year average. That tells us investors are still willing to hold duration, even with rising yield risk globally.

There’s also growing speculation that the Ministry of Finance could tweak its issuance strategy. A recent survey sent to market participants asked for feedback on current issuance conditions a sign that Tokyo is open to changes as it tries to manage both fiscal goals and bond market stability. Meanwhile, the government has pushed back its primary surplus target to 2025 or even 2026, suggesting that fiscal consolidation may take a backseat to growth management.

On the monetary side, BoJ Governor Ueda has remained steady. His recent parliamentary comments showed no urgency to raise rates prematurely. The BoJ is expected to continue reducing its bond purchases in a gradual, predictable way, sticking with the current JPY400 billion quarterly taper paces. The next round of bond-buying plans will be announced on June 17. For now, the BoJ is walking a fine line reducing stimulus while making it clear they’re not hiking rates just to create room for future cuts.

That stance may frustrate the hawks, but it’s a smart move. The yen has been undervalued for a while, and now, as volatility returns and global uncertainty climbs, the yen’s safe-haven appeal is starting to reassert itself. Unless the BoJ pivots sharply which seems unlikely near-term USD/JPY could stay under pressure.

The global FX landscape is shifting. The dollar’s dominance is being tested by rising geopolitical noise, softer US data, and a recalibration of Fed expectations. Meanwhile, the yen is finding a bid not because Japan is roaring ahead, but because markets are rediscovering its defensive qualities at a time of global doubt.

What’s clear is that volatility is back, and macro narratives are fluid. As June unfolds, traders will need to stay agile. The US election cycle, trade war risks, and central bank path dependencies are all colliding. The easy carry trades are fading. This is a market where macro really matters again.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.