just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

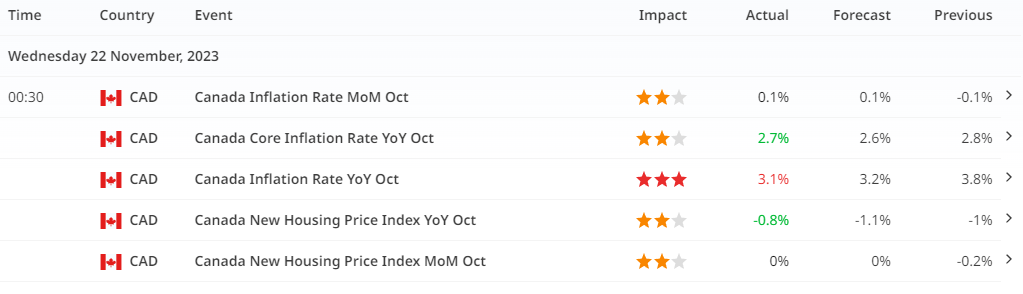

Canada CPI

Source: Finlogix Calander

In the month of October, Canada witnessed a further moderation in annual inflation, with the pace standing at 3.1%, aligning with consensus expectations. This marked a significant deceleration from the previous month's 3.8%, primarily attributed to a decline in gasoline prices. However, notable contributors to annual inflation remained consistent, with mortgage interest costs (MIC), rent, and food prices continuing to exert significant influence.

Delving into the Bank of Canada's preferred inflation metrics, both the CPI-trim and median indicators exhibited deceleration, registering at 3.5% and 3.6% year-on-year, respectively. This trend suggests a concentration of price increases, particularly in shelter costs. Examining CPI excluding food, energy, and MIC, the figure remained at 2.2% year-on-year and decelerated to 1.8% in three-month annualized change terms. Looking ahead, the prevailing weak economic conditions are expected to exert further downward pressure on these measures, potentially paving the way for the Bank of Canada to consider rate cuts as early as the second quarter of the following year.

The acceleration in service price inflation, rising to 4.6% year-on-year from 3.9%, can be attributed to various one-off factors unrelated to underlying demand. Property taxes, typically priced annually in October, increased by 4.9% year-on-year, while electricity prices in Alberta witnessed a significant surge of 45% year-on-year. Travel tour prices also experienced an 11% year-on-year increase, although this pace may not be sustained due to consumer constraints arising from higher interest rates and a rise in the unemployment rate. Disinflationary signals were evident in the airline industry, as airfares declined by 19% year-on-year.

On the goods front, prices decelerated to 1.6% year-on-year from 3.6%, and even when excluding food and energy, a notable deceleration occurred, dropping to 1.7% year-on-year from 2.4%. This deceleration reflects ongoing improvements in supply, as the inventory-to-sales ratio surpassed its pre-pandemic level in the second quarter, likely to rise further as constraints on production ease in the coming months. The deceleration is also indicative of fading demand, with retail sales exhibiting lacklustre performance as consumers allocate a greater portion of their income to higher interest payments.

The rental market experienced a surge in costs, rising by 8.2% year-on-year, driven by population growth and elevated interest rates attracting new entrants. This surge in rental costs further solidifies shelter as the primary source of inflation, as CPI excluding shelter maintains a 1.9% year-on-year pace.

Implications & actions

Regarding the economic forecast, it is anticipated that the headline Consumer Price Index (CPI) index may not exhibit significant progress by the end of the year. This expectation is based on the influence of base effects, which could lead to a notable jump in December following a temporary reprieve in November. The anticipated drop in energy prices from a year ago is expected to be a significant factor in this annual calculation.

However, despite potential fluctuations in the headline CPI index, the Bank of Canada is expected to place greater emphasis on its preferred core measures of trim and median. These core measures are anticipated to continue decelerating, primarily due to weakened domestic demand. This ongoing deceleration in core measures could provide policymakers with the necessary conditions to contemplate and potentially implement interest rate cuts, with a potential timeline as early as the second quarter of the following year.

The consideration of core measures underscores the central bank's focus on underlying inflationary trends, providing a more nuanced and stable view compared to the headline CPI, which can be influenced by temporary factors. The expectation of interest rate cuts in the coming quarters reflects a proactive stance by policymakers in response to prevailing economic conditions, with an emphasis on addressing weak domestic demand as a key factor in their decision-making process.

Concerning the markets' response to the economic data, it is noteworthy that there was minimal reaction observed. This lack of significant movement can be attributed to the fact that the reported figures were in line with the consensus expectation. Despite the data aligning with market forecasts, there remains a prevailing sentiment that markets are assigning insufficient probability to potential Bank of Canada (BoC) interest rate cuts in the upcoming year, at least according to the perspective being presented.

The market's seemingly subdued reaction could be indicative of a certain level of complacency or an underestimation of the likelihood of future policy adjustments by the BoC. This perspective suggests that, even with data falling within anticipated ranges, there may be factors or trends not fully priced in by market participants, potentially impacting their expectations for central bank actions.

This interpretation implies that market sentiment might be overlooking certain economic indicators or risks that could influence the BoC's decisions in the future. It underscores the importance of considering a broader range of factors beyond just the immediate data release when gauging market reactions and expectations.

The notion of potentially insufficient odds being placed on BoC cuts in the upcoming year implies a potential divergence between market sentiment and the expectations of those advocating for a more dovish stance. It will be interesting to observe how this dynamic evolves in the coming months and whether there will be an adjustment in market expectations in response to changing economic conditions or shifts in central bank guidance.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.