just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

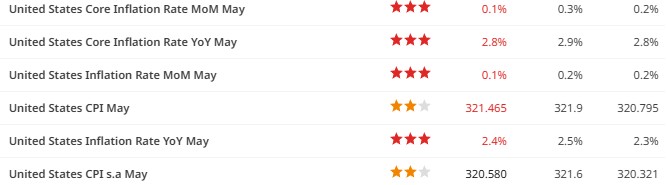

Headline CPI rose just 0.1% month-on-month in line with consensus, but the year-on-year figure softened to 2.4% against expectations for 2.5%. More notably, core CPI slowed to 2.8% YoY, missing the forecast of 2.9%. On a sequential basis, the 0.1% core MoM print helped confirm that inflation pressures while still present are not accelerating in the way some feared given the backdrop of newly reinstated tariffs.

This data weakens the immediate argument for inflation-driven rate hikes and reinforces the idea that the Federal Reserve can remain patient. In response, the dollar (DXY) sold off modestly, particularly against lower-beta currencies, while long-end Treasury yields slipped. Markets will now be watching for how Fed speakers interpret this in the days ahead, particularly given the previously elevated concern over tariff passthrough and inflation anchoring.

The lower CPI print is especially significant given it captures a full month of trade-related pricing pressures following the reintroduction of 10% reciprocal tariffs by the US administration. The absence of a significant price spike suggests businesses may still be absorbing cost increases or that the consumer’s willingness to tolerate higher prices is waning. Either way, the short-term inflation impulse from tariffs appears more muted than feared.

However, risks remain firmly on the table. The upcoming July 9 deadline for the expiration of the current tariff suspension could result in the US increasing reciprocal duties to 20% or even 50% on some EU goods. A court hearing scheduled for July 31 is unlikely to intervene in time, and as such, the inflation story is far from over. The market may have received temporary relief, but the structural backdrop is still one of fragility.

Meanwhile, demand for long-dated Treasuries continues to deteriorate. While Tuesday’s 3-year auction passed with only mild concern, the $39 billion 10-year and $22 billion 30-year auctions this week remain critical. Investor appetite is clearly thinning, driven by both inflation uncertainty and worsening debt sustainability sentiment. The sharp breakdown in correlation between 30-year yields and the US dollar which has fallen from +0.65 last year to near zero reflects this evolving risk perception.

On the currency front, two underperformers stand out.

The New Zealand dollar (NZD/USD) has weakened following confirmation that former RBNZ Governor Adrian Orr quietly resigned in March due to internal conflict regarding central bank funding. Although the change was not made public until now, it raises questions about the institution's internal stability and independence, particularly as the country navigates a high inflation environment with slowing growth.

The Japanese yen continues to drift lower, weighed down by speculation that the Bank of Japan will reduce the pace of its JGB purchases. While there were initial rumours of Ministry of Finance bond buybacks, these have since been denied. The JGB market remains broadly stable, and with inflation pressures building, there is a growing likelihood that the BoJ will adopt a more hawkish tone at next week’s meeting. While the yen may weaken in the near term due to dollar strength, we do not see significant scope for a sustained sell-off. A signal of another rate hike from the BoJ could quickly re-anchor the currency.

In Europe, the potential for a 50% reciprocal tariff on EU exports to the US remains a real concern. If enacted, it could accelerate the timing of ECB rate cuts and add downside pressure on the euro. As things stand, the ECB appears increasingly boxed in forced to weigh imported inflation risks against weakening domestic demand.

We are approaching a key inflection point. The combination of tariff-related inflation pressure, weakening bond demand, and deteriorating fiscal sentiment in the US has the potential to reprice the FX complex in a significant way. Today’s CPI print is not just another data point it is a temperature check on whether inflation expectations are becoming unanchored. If inflation surprises to the upside, we could see renewed USD strength, especially if rate cut expectations get pushed back.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.