just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

In the lead-up to this week’s FOMC meeting, markets appear to be caught in a tug-of-war between the Federal Reserve’s communication strategy and a brewing sense of macroeconomic fragility. What’s clear from the latest positioning data and central bank commentary is that investors are preparing for multiple outcomes, but with a growing lean toward a short USD bias. This tension underscores a broader divergence in how policymakers and market participants interpret risks tied to inflation, labour markets, and global trade volatility.

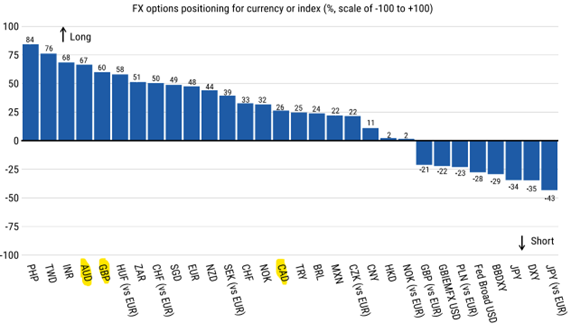

From an FX perspective, recent data from Morgan Stanley reveals that traders have begun dialling down their short NZD and CAD exposure in the futures market, while building moderate short positions against the USD. Option markets reflect a somewhat different reality, showing tactical preference for AUD and GBP longs, and a notable shift into short JPY territory. What we’re seeing is a nuanced repositioning rather than a full-on bet against the greenback, this is a hedge-heavy environment shaped by heightened uncertainty ahead of the Fed’s decision.

The MUFG team goes even further in highlighting that “inaction is action.” Their core message is that by delaying cuts, the Fed risks amplifying downside risks. While market expectations lean toward no immediate move this week, the absence of dovish signalling could easily be read as policy error, especially considering how fragile the post-tariff U.S. economy is proving to be. Q1 GDP came in negative driven largely by a surge in pre-tariff imports and yet Fed Chair Powell may well downplay that result, pointing instead to a “resilient” labour market and robust services activity.

But beneath the surface, warning signs are flashing. Labor market indicators including the Beveridge curve and NY Fed consumer sentiment suggest softening demand for workers and a growing fear among households about job security. Surveys reveal fewer firms are hiring, and government job cuts have started to bleed into the broader employment ecosystem, particularly for institutions reliant on public funding. If Powell chooses to ignore these signals, the Fed could find itself once again tightening financial conditions unintentionally through perceived inaction.

On inflation, the split is just as stark. Core goods prices are expected to rise as tariff impacts ripple through supply chains, while core services inflation is already cooling, thanks in part to wage moderation. The Fed should be “looking through” this form of supply-side inflation, yet history shows they often struggle to do so when political noise and market volatility cloud judgment. Meanwhile, housing inflation is set to moderate further, as new tenant rent growth turns negative a lead indicator that points toward easing shelter cost pressures in the CPI prints.

This puts the Fed in an awkward position: data is not unequivocal, but the bias of risks is. Waiting longer to ease could tighten liquidity further, especially with swap spreads showing signs of stress a reminder that structural issues like balance-sheet scarcity in bond markets are very much alive. As the MUFG team points out, only once in the past quarter century has the Fed paused for more than six months in an easing cycle. We’re nearly at that point again.

Back in the FX space, this context is crucial. AUD/USD has emerged as a contrarian long in Morgan Stanley’s model, driven partly by oversold conditions and improving sentiment toward China. Meanwhile, USD/CAD is seen as a preferred long, suggesting markets are less convinced by Canada’s resilience, even as CAD short positions were unwound. GBP, though still sensitive to political noise ahead of UK elections, remains a beneficiary of yield stability and investor interest, particularly as EUR longs begin to fade and sterling is seen as a relatively undervalued hedge.

The Japanese yen continues to puzzle option traders are betting against it, yet futures positioning remains long. This likely reflects a complex mix of carry trade dynamics and lingering fears that Japanese authorities might intervene. But the key here is that JPY weakness isn’t necessarily a reflection of confidence in global growth it’s more about interest rate differentials and market recalibration.

In short, we’re approaching this FOMC with positioning that is anything but neutral. Investors are cautiously leaning against the dollar, hedging their bets through AUD, GBP, and SEK, while avoiding overexposure to safe havens like JPY and CHF. The Fed’s messaging will either validate these tactical tilts or trigger a broad unwind.

If Powell opts for another non-committal “wait and see,” markets could react sharply. That doesn't necessarily mean a spike in the USD especially if the broader read is that the Fed is falling behind the curve. But it does imply another leg of volatility across G10 FX, as investors scramble to recalibrate for what now appears to be a longer, messier end to the U.S. tightening cycle than initially hoped.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.

Want to master the markets? A winning trading mindset beats a perfect strategy. Learn how emotional discipline helps you conquer fear and avoid heavy losses.