just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

Central banks stole the spotlight this week as they reacted to persistent worries about inflation and indications of a slowing economy.

Among the various currencies, the New Zealand dollar emerged as the top performer, while the British pound struggled, impacted by the Bank of England's recent policy shift.

In case you didn't catch the most important forex updates, here's a summary of the FX market happenings from last week.

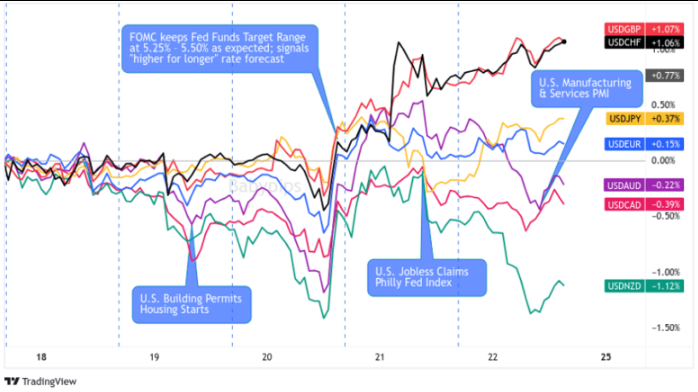

USD Pairs

Once again, the U.S. dollar found itself swayed by speculations concerning the Federal Reserve's actions. This time, those speculations were confirmed with the release of the latest monetary policy statement by the FOMC.

As expected, there were no alterations to the Fed funds target range. However, what caught many off guard was the committee's hawkish stance, signalling a strong likelihood of another interest rate increase in 2023 and a diminished likelihood of substantial rate reductions in 2024.

Initially, this development prompted the dollar to recover from a significant decline leading up to the event. Nevertheless, by the end of the week, the performance of the greenback was mixed, as upbeat U.S. weekly initial jobless claims data on Thursday seemed to spur some risk-on sentiment.

Bullish Headline Arguments

Bearish Headline Arguments

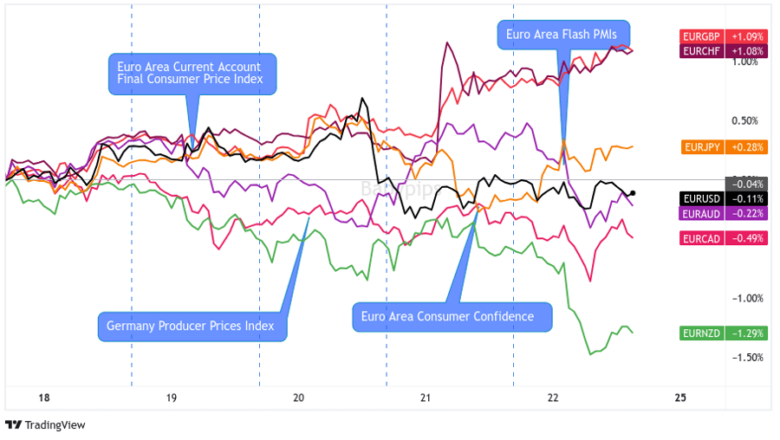

EUR Pairs

Throughout the week, the Euro's performance was a mixed bag, indicating that the actions of opposing currencies played a more substantial role than European news and data releases.

However, by Friday, the Euro sustained a consistent bearish trend due to disappointing updates regarding the Euro area Purchasing Manager's Survey data. This negative data seemed to overshadow any positive factors and added to the downward pressure on the Euro's value.

In the bigger picture, the Euro ended the week as a net loser when compared to most major currencies, with the exceptions being the Swiss franc and the British pound. Both currencies faced their own bearish pressure after their respective central banks unexpectedly opted not to raise interest rates.

Bullish Headline Arguments

Bearish Headline Arguments

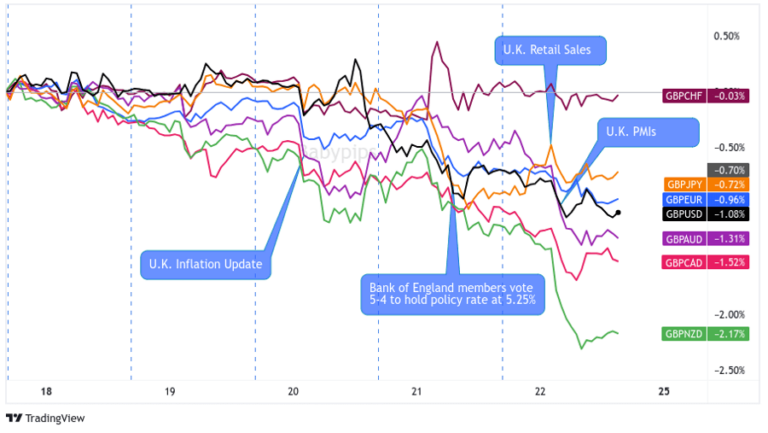

GBP Pairs

The British Pound had a tough week, to be blunt. It faced a continuous decline in value, primarily stemming from prior statements made by the Bank of England, which indicated that additional interest rate hikes were unnecessary. This cautious stance from the central bank raised concerns among investors and had a negative impact on the Pound's performance.

Two specific events exacerbated the pressure on the Pound. Firstly, the release of UK inflation figures on Wednesday disappointed, likely causing unease among investors about the state of the economy. Then, on Thursday, the Bank of England had a close vote of 5-4 to maintain interest rates at 5.25%. While the decision wasn't unanimous, it sent a mixed message and added to the challenges faced by the Pound.

Bullish Headline Arguments

Bearish Headline Arguments

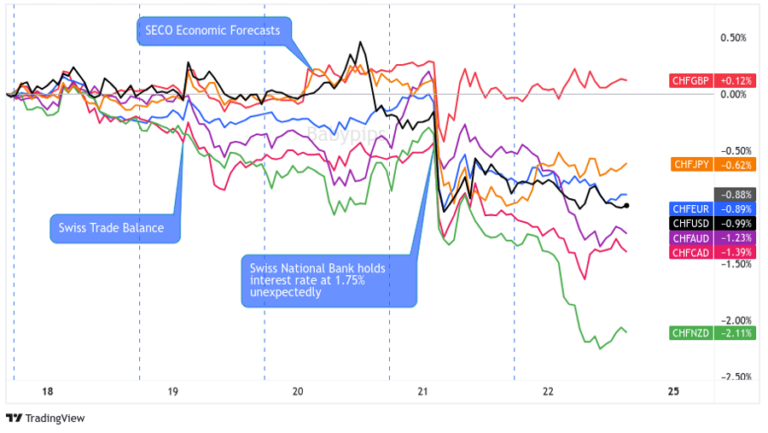

CHF Pairs

The Swiss Franc indeed faced a difficult week, and there's no need to sugarcoat it. The situation took a negative turn when the Swiss National Bank (SNB) decided to keep their key interest rate at 1.75%, going against the expectations of many who had anticipated a 25-basis point increase.

It was as if the SNB made an unexpected move, and this had a substantial impact on the value of the Swiss Franc. To be fair, some recent data had hinted at the possibility of the SNB delaying rate hikes, but it still caught many by surprise, resulting in a bearish sentiment surrounding the Franc's value throughout the week.

Bullish Headline Arguments

Bearish Headline Arguments

AUD Pairs

The Australian dollar had a robust week, primarily fuelled by the positive sentiment that had been gaining momentum ever since China implemented stimulative measures.

Nonetheless, there were some hurdles to overcome. The introduction of a hawkish tone by the Federal Reserve didn't sit well with Australian traders initially. However, the currency managed to rebound on Friday, aligning with the release of Australia's Composite Purchasing Managers' Index (PMI), which showed an increase. This uptick indicated an improvement in business sentiment in Australia.

In summary, the Australian Dollar had a volatile week but exhibited resilience in navigating through market fluctuations.

Bullish Headline Arguments

Bearish Headline Arguments

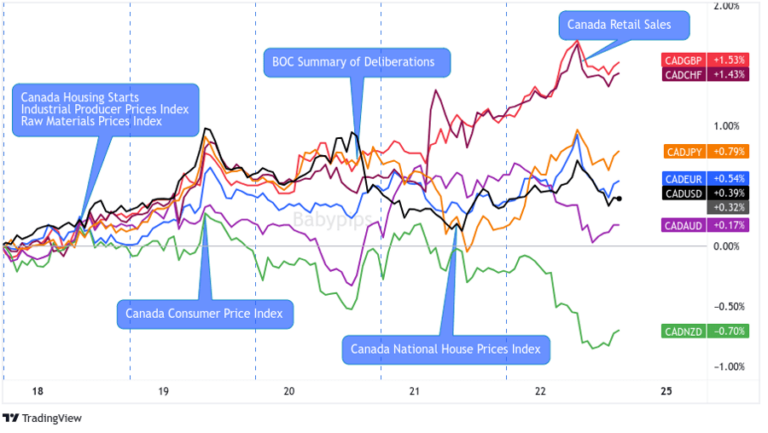

CAD Pairs

The Canadian Dollar kicked off the week on a strong note, outperforming major currencies, with only the New Zealand Dollar surpassing it in strength by the week's end. There was a minor setback on Tuesday following the release of higher-than-expected inflation data from Canada, potentially driven by profit-taking and a shift in focus towards declining oil prices.

On Wednesday, risk sentiment prevailed as a hawkish statement from the Federal Reserve impacted global markets. This led to some losses for the Canadian Dollar against major currencies, except for the Australian and New Zealand Dollars. However, the bullish momentum was swiftly regained, likely bolstered by the rise in oil prices after news emerged that Russia would temporarily halt fuel exports to bolster its domestic fuel economy.

Bullish Headline Arguments

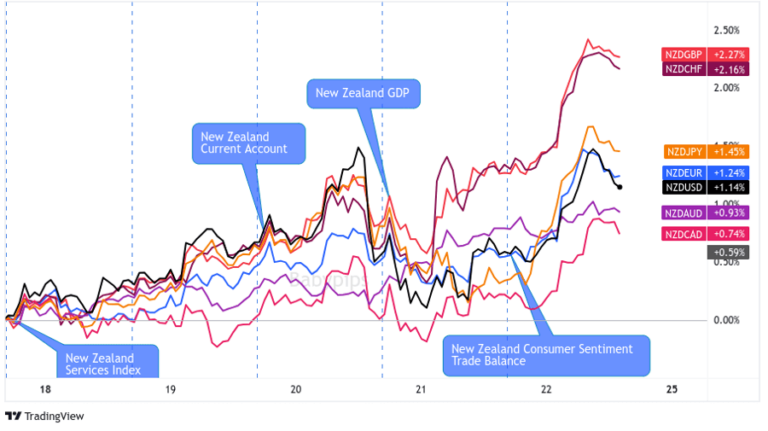

NZD Pairs

The New Zealand Dollar had a favorable week, with its strength likely influenced by the positive economic conditions in the Asia region, particularly driven by China's recent economic stimulus measures. Despite a mix of economic data updates, there were notable highlights that contributed to the Kiwi's robust performance.

Bullish Headline Arguments

Bearish Headline Arguments

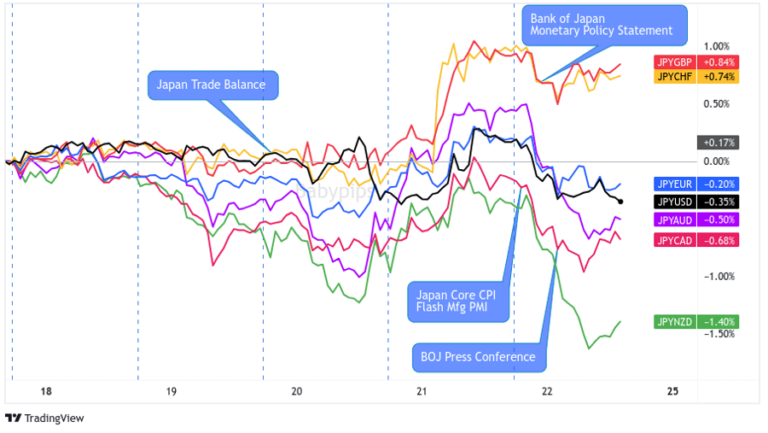

JPY Pairs

The Japanese Yen experienced a somewhat turbulent week, leaning towards a negative performance. Several factors contributed to this trend, including positive developments in Asia, particularly China's economic stimulus efforts, and the anticipation of the Bank of Japan (BOJ) maintaining its ultra-easy monetary policy during its decision on Friday.

There was a moment when the Yen strengthened in response to a hawkish event by the Federal Reserve, which triggered a risk-off sentiment and drove traders towards safe-haven assets. However, this rally was short-lived, and the sentiment shifted during the U.S. session on Thursday, possibly due to better-than-expected U.S. jobless claims data, which supported the idea of a "soft landing."

When the BOJ finally announced its decision on Friday, they adhered to expectations by keeping ultra-low interest rates unchanged at -0.10%, cementing the Yen's bearish trajectory for the remainder of the week.

Bullish Headline Arguments

Bearish Headline Arguments

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Last week we identified five bearish catalysts converging into a single week and argued that the bears had a window but not the narrative. The data came in largely as expected. CPI fell to 3.8%. PPI confirmed the same backward-looking story. Retail sales badly missed, growing 0.2% against a 1.0% forecast. Chair Warsh was guarded in his congressional testimony. Markets had a difficult session before stabilizing after hours on the CPI print.

STARTRADER has launched 42 new 24/5 US stock CFDs and confirmed 43 new 24/7 US stock CFDs from 27 July 2026, giving clients access to 85 widely traded names including NVIDIA, Apple, Tesla, and Boeing, with round-the-clock trading addressing traditional exchange schedule constraints.

Luramic, a regulated provider of institutional liquidity and trade execution services, has announced the launch of its liquidity platform for brokers, hedge funds, and proprietary trading firms.

The Vault has partnered with blockchain security firm Halborn to launch a joint advisory programme helping banks, treasuries and financial institutions design and validate digital asset custody infrastructure, combining architecture design with independent security review through a four to six week engagement.

Marex has partnered with Coinbase to allow clients to use USDC, Circle's dollar-denominated stablecoin, as initial margin collateral for CFTC-regulated derivatives, following a CFTC no-action letter. The service completed its first transaction with Prime Trading, LLC, supported by Coinbase's custody and reporting infrastructure.

cBridge, by Spotware, has launched Markout Report, a risk intelligence module that lets brokers detect toxic flow, rank accounts by financial impact and act before losses accumulate, all within the bridge.

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.