just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

USD: Fed signals higher rates for longer & softer landing for US economy.

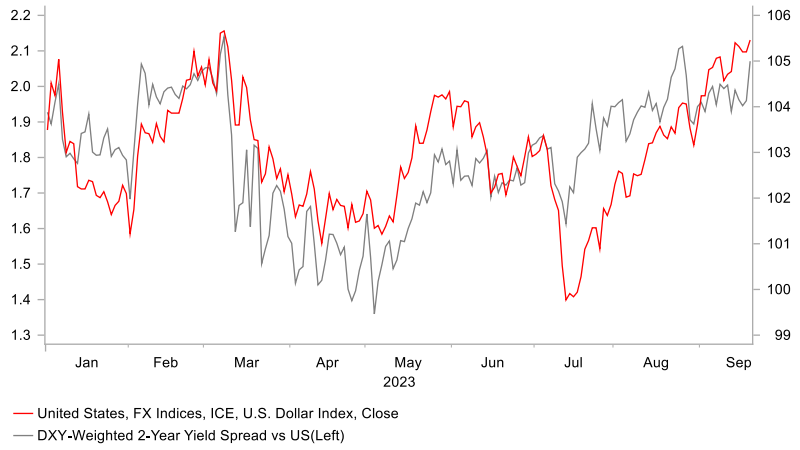

During the Asian trading session, the US dollar has maintained its strength following the recent FOMC meeting. This resulted in the dollar index reaching an intraday high of 105.69. The surge in the US dollar's value has been driven by the upward adjustment in US yields overnight. Specifically, the 2-year US Treasury yield saw a notable increase of approximately 12 basis points since just before the FOMC meeting, reaching an overnight intraday high of 5.18%. This represents a new cyclical high, surpassing the previous high of 5.12% from July.

The rise in short-term yields also had a mild effect on longer-term yields. The 10-year US Treasury yield increased by around 10 basis points, reaching a new cyclical high of 4.45%. This shift in yields was primarily triggered by the Federal Reserve's decision to adopt a more hawkish stance yesterday morning at 4am on Sydney time. While the Fed opted to keep the policy rate unchanged, the updated guidance provided a clear indication that the Fed intends to maintain higher interest rates for an extended period (hawkish stance). Consequently, the US rate market has scaled back its expectations for rate cuts by the Fed in the upcoming year, with approximately 58 basis points of cuts now being priced in by the end of the next year. This month alone, nearly 50 basis points of cuts have been removed from the US yield curve, lending further support to the US dollar.

The Fed's "higher for longer" message was articulated through revisions to economic and policy rate projections. The updated dot plot revealed that a majority of FOMC participants still plan to implement one final rate hike later this year. Out of the 19 participants, 12 favour increasing the policy rate to 5.625% by year-end, mirroring projections from June. The most significant alteration to the forecasts is that FOMC participants now anticipate fewer rate cuts in the coming years. The median projection for the Fed's policy rate by the end of the next year and the end of 2025 has both been raised by 0.50 point to 5.1% and 3.9%, respectively. Additionally, the Fed released projections for 2026 for the first time, showing a policy rate closer to their neutral estimate of 2.5%, with a projection of 2.9% by the end of 2026.

The primary reason behind the Fed's indication of a prolonged period of higher rates is its increased confidence in a softer landing for the US economy. There were notable upward revisions to GDP forecasts for this year and the next, now standing at 2.1% and 1.5%, respectively. This suggests a more modest slowdown in growth in the coming year. Consequently, the Fed no longer anticipates a significant rise in the unemployment rate from its current level of 3.8%, which is slightly above the cyclical low of 3.4% set in January. The unemployment rate forecasts for this year and the next were both revised downward by 0.4 percentage points to 4.1%. With less expected slack in the US labor market, the Fed does not foresee continued undershooting of their inflation projections in the years ahead. While the core PCE forecast for this year was lowered by 0.2 percentage points to 3.7%, core inflation forecasts for the next year and 2025 remained largely unchanged at 2.6% and 2.3%, respectively, with a slight increase of 0.1 point.

Overall, the Fed's updated guidance is expected to reinforce the upward momentum of the US dollar in the short term. There is a higher risk of one final rate hike in November or December, although weaker economic activity and core inflation data in Q4 could dissuade the Fed from following through with these plans. Similarly, we anticipate a more significant negative impact on the US economy in the coming year due to the delayed effects of previous aggressive tightening, which may encourage the Fed to implement more than the planned 50 basis points in rate cuts by the end of 2024.

USD VS. SHORT-TERM YIELD SPREADS

Source: Bloomberg, Macrobond & MUFG Research

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

cBridge, by Spotware, has launched Markout Report, a risk intelligence module that lets brokers detect toxic flow, rank accounts by financial impact and act before losses accumulate, all within the bridge.

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.