just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

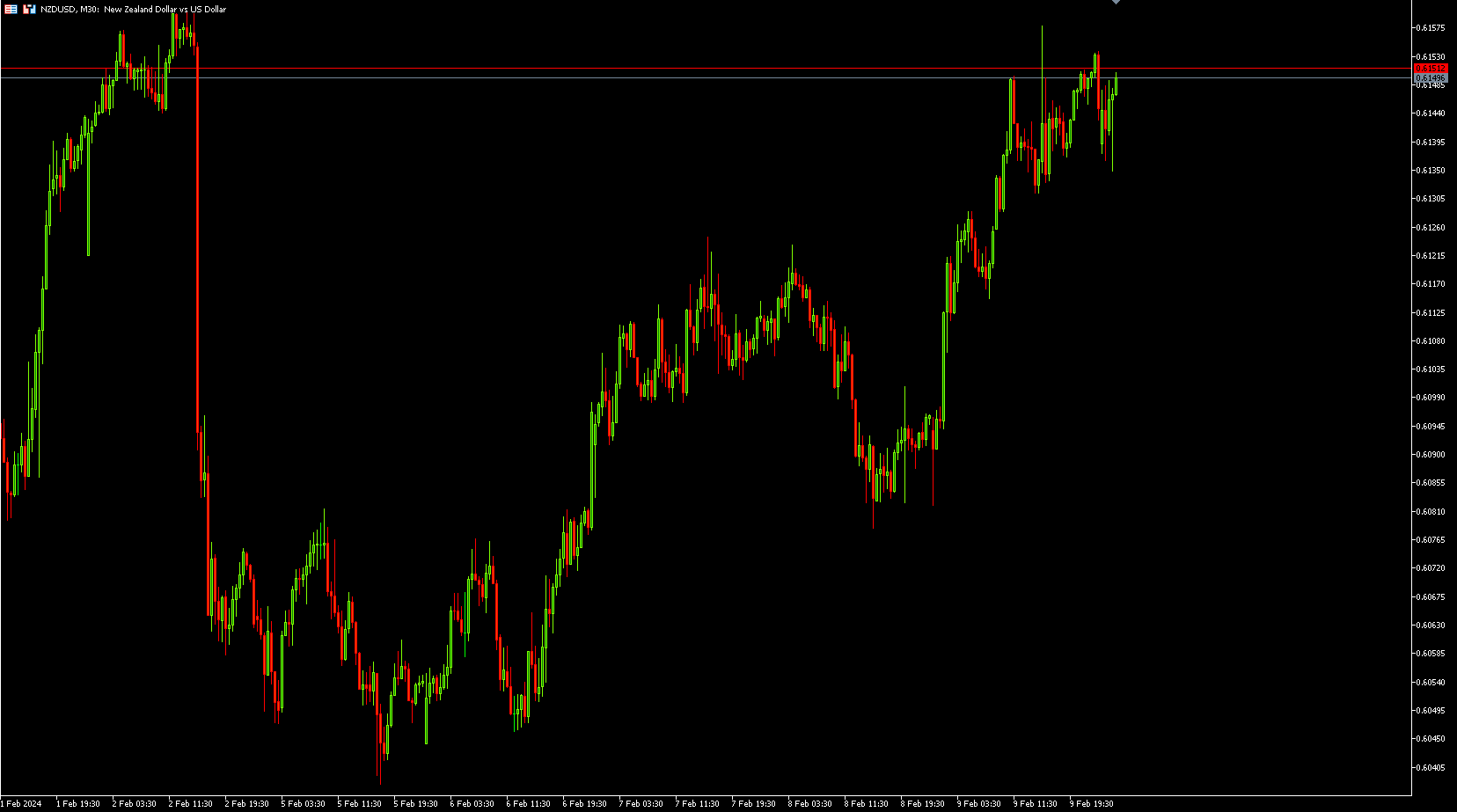

The New Zealand dollar emerges as a standout performer, marking a notable gain of approximately +0.6% against the US dollar in recent overnight trading. A week-long ascent from the low of 0.6038 on February 5th to an overnight high of 0.6135 paints a picture of Kiwi strength. Particularly striking is its dominance against the Aussie, pushing the AUD/NZD rate to its lowest since May of the previous year, lingering just below the 1.0600-level.

Fuelling this surge is the unexpected hawkish turn in the Reserve Bank of New Zealand's (RBNZ) rate hike expectations this month. The implied yield on the December 2024 New Zealand three-month interest rate futures contract has surged by approximately 60 basis points since the beginning of February. The market now anticipates a higher probability of the RBNZ executing one final rate hike before potentially reversing course and implementing rate cuts later in the year. As of now, around 22 basis points of hikes are priced in by the May RBNZ policy meeting, with the expected number of cuts by year-end scaled back to only about 36 basis points.

Noteworthy Friday’s reports from ANZ bank, revising their RBNZ call, add further momentum to market expectations. ANZ now forecasts two additional 25 basis points hikes in February and April, influenced by robust labour market and Consumer Price Index (CPI) reports from New Zealand in Q4.

NZDUSD 30min

Source: MetaQuotes ACY Securities

Shifting focus to last week's market wrap-up, global markets experienced consolidation amid a lack of fresh data triggers. Federal Reserve Bank of Richmond President Barkin echoed caution about the timing of rate cuts, contributing to a patient market sentiment. ECB Chief Economist Lane highlighted near-term disinflation occurring faster than anticipated, emphasizing the need for further progress toward the 2% goal. ECB Governing Council member Wunsch expressed concerns about wage growth not aligning with the 2% inflation target, advocating for a wait-and-see approach before considering rate cuts. The S&P 500, while marginally lower at the time of writing, flirted with record highs, and the Euro Stoxx 50 closed 0.7%, while the FTSE 100 fell 0.4%. Meanwhile, the US 10-year note saw a 2 basis points lift to 4.14%, and oil prices trended higher with WTI reaching USD76.1/bbl, a 3.0% increase. Gold, however, experienced a slight dip of 0.1%, closing at USD2,033/oz.

Insights Inspired by MUFG & ANZ: Credit to Their Analysis for Shaping Some Aspects of This Text

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

cBridge, by Spotware, has launched Markout Report, a risk intelligence module that lets brokers detect toxic flow, rank accounts by financial impact and act before losses accumulate, all within the bridge.

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.