just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The US dollar has entered the week struggling to recover from last week’s sharp decline, with the DXY index falling below the 104.00 level. This move erases all gains the dollar had accumulated since Donald Trump’s election victory. The sell-off coincided with a shift in market sentiment following softer US economic data and renewed uncertainty around the administration’s economic policies. Over the weekend, President Trump acknowledged that the economy is in a “period of transition,” downplaying concerns over tariffs while insisting that any adjustments would be minor. However, the broader market remains sceptical about the impact of potential trade policies on growth and inflation.

Equity markets have followed a similar trajectory. The S&P 500 has erased its post-election gains, retreating to its 200-day moving average near 5,730. Investors are speculating whether the weakness in both economic indicators and risk assets could pressure Trump into scaling back his tariff plans. So far, the administration has shown limited concern, with only minor rollbacks on Canadian and Mexican tariffs implemented last week.

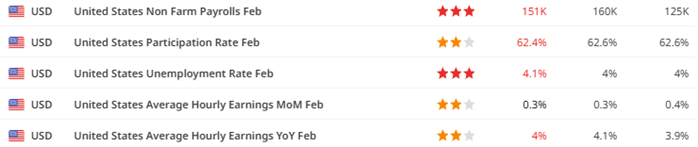

The latest nonfarm payrolls report revealed a 151,000 job increase in February, an improvement from January’s downwardly revised 125,000 figures. However, after factoring in revisions, net job growth fell short of expectations by 11,000. While employment trends remain solid—averaging 191,000 jobs per month over the last six months—recent data suggests a loss of momentum compared to the post-election hiring surge. Notably, the federal government shed 10,000 jobs in February, marking the sharpest decline since mid-2022, potentially reflecting the administration’s push to reduce public sector employment.

Federal Reserve Chair Jerome Powell remains cautious but not overly alarmed by the latest economic developments. He reaffirmed that while uncertainties persist, the economy remains "in a good place," emphasizing that the Fed is not in a rush to adjust policy. Despite this stance, markets have priced in a more dovish outlook, with expectations now leaning toward a June rate cut and a total of 75 basis points in easing by year-end. This divergence between market pricing and Fed rhetoric has contributed to the dollar’s recent slide.

Another major driver of recent USD weakness has been the sharp rise in yields outside the US. The 10-year Japanese Government Bond (JGB) yield climbed to a new year-to-date high of 1.58%, reflecting growing expectations that the Bank of Japan (BoJ) will tighten policy further. January’s labour cash earnings report showed a 3.0% rise in base salaries, reinforcing speculation that the BoJ could raise rates as early as June or July, with some pricing in a smaller hike even in May. If this trajectory continues, Japanese rates could climb toward 1.00% by year-end, further narrowing the yield differential with the US and pressuring USD/JPY lower.

Meanwhile, German bond yields also saw a significant jump last week, with 10-year Bund yields rising 40 basis points to 2.84%, approaching their October 2023 highs. Markets reacted strongly to expectations that Friedrich Merz, the incoming German Chancellor, will pursue expansionary fiscal policies. Plans for increased defence and infrastructure spending have pushed up government borrowing costs while simultaneously providing a tailwind for European assets, strengthening the euro in the process.

Markets will closely watch upcoming macroeconomic releases, including the Sentix Investor Confidence Index in the Eurozone and US Consumer Inflation Expectations. Additionally, remarks from key policymakers such as Bundesbank President Joachim Nagel could influence rate expectations in Europe. In Japan, GDP data and household spending figures could further shape market views on the BoJ’s policy trajectory.

With the USD facing headwinds from softening economic data, shifting Fed expectations, and rising global yields, the next few weeks will be critical in determining whether the dollar finds stability or extends its decline.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.

Want to master the markets? A winning trading mindset beats a perfect strategy. Learn how emotional discipline helps you conquer fear and avoid heavy losses.