just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

It’s not often that one report can shake the whooe market narrative, but that’s exactly what happened after Friday’s U.S. non-farm payrolls data.

I’ve been watching these developments closely, and the shift in sentiment is something traders shouldn’t underestimate.

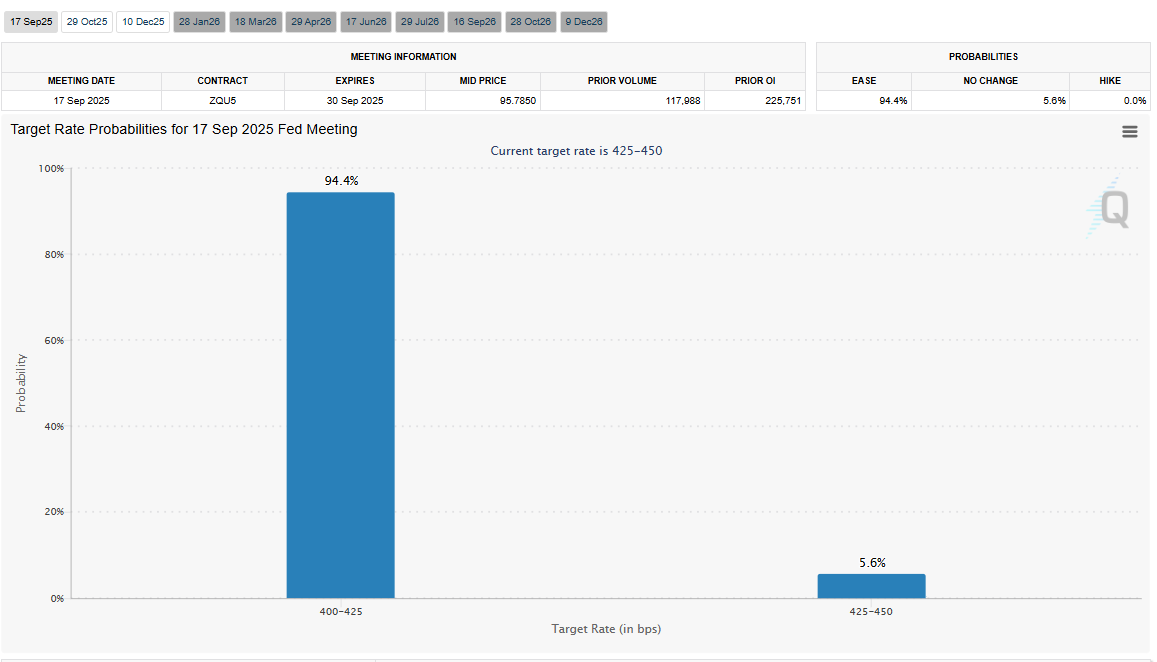

Just days ago, the market was still debating whether the Fed might hold rates into year-end. Fast-forward to now, and we’re staring down the barrel of an 90% probability of a rate cut in September.

The US02-year yield collapsed by almost 30 basis points, and the dollar reacted exactly as you’d expect in this kind of repricing: it tanked.

But there’s more to the story than just rates.

We’re not just talking about a soft report here. The revisions to previous data were brutal. Over the last three months, non-cyclical sectors (excluding health and education) lost 49,000 jobs.

This isn’t your typical post-COVID adjustment, that kind of decline is historically associated with full-blown crises.

Add to that a significant drop in the ISM manufacturing employment index, which plunged to levels we haven’t seen since the GFC, and it becomes clear: this wasn’t a blip. It’s systemic.

We’ve now gone from “data-dependent Fed” to “what will stop them from cutting?” The market is no longer waiting for a green light the assumption is that the easing cycle is now the base case, not the tail risk.

What makes this moment stand out is that the USD is already weak, it’s fallen over 10% in the first half of the year.

And while that may suggest limited room for further downside, the underlying drivers here are far more concerning than usual.

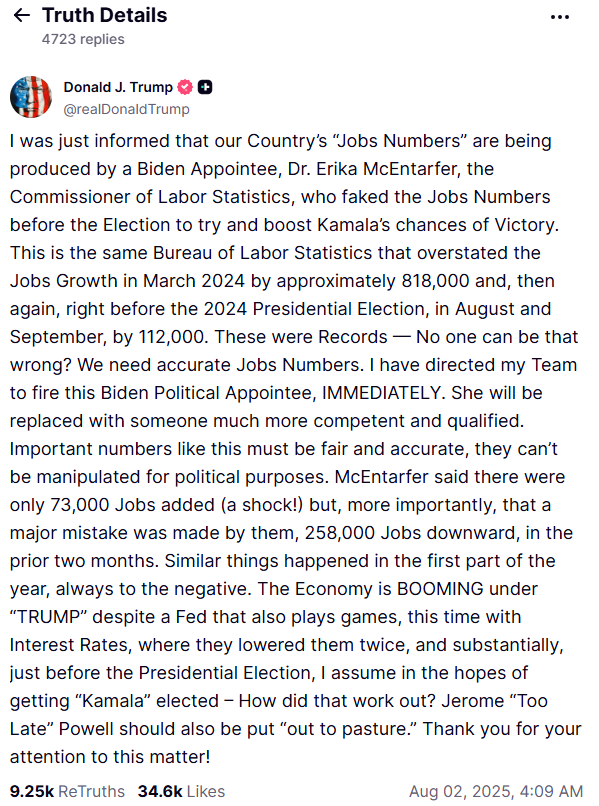

There’s also a growing sense that politics is spilling over into monetary policy. Trump’s comments about Powell and the firing of the BLS head after weak jobs data raise valid concerns around institutional independence something markets are hypersensitive to.

If that confidence erodes further, we could see another leg down in the dollar.

Right now, the market is digesting all of this and starting to rethink the entire U.S. macro narrative. The Fed's messaging remains cautious, but if inflation doesn’t surprise to the upside, a cut in September looks almost baked in.

Some key things on my radar this week:

Durable goods and factory orders today (both expected to slow sharply)

The next CPI print, which could either fuel or halt this dovish pivot

The Fed’s Loan Officer Survey, giving us insight into credit conditions, which are likely tightening further

With yields plummeting and risk appetite slowly returning (at least for now), here are two setups I find compelling:

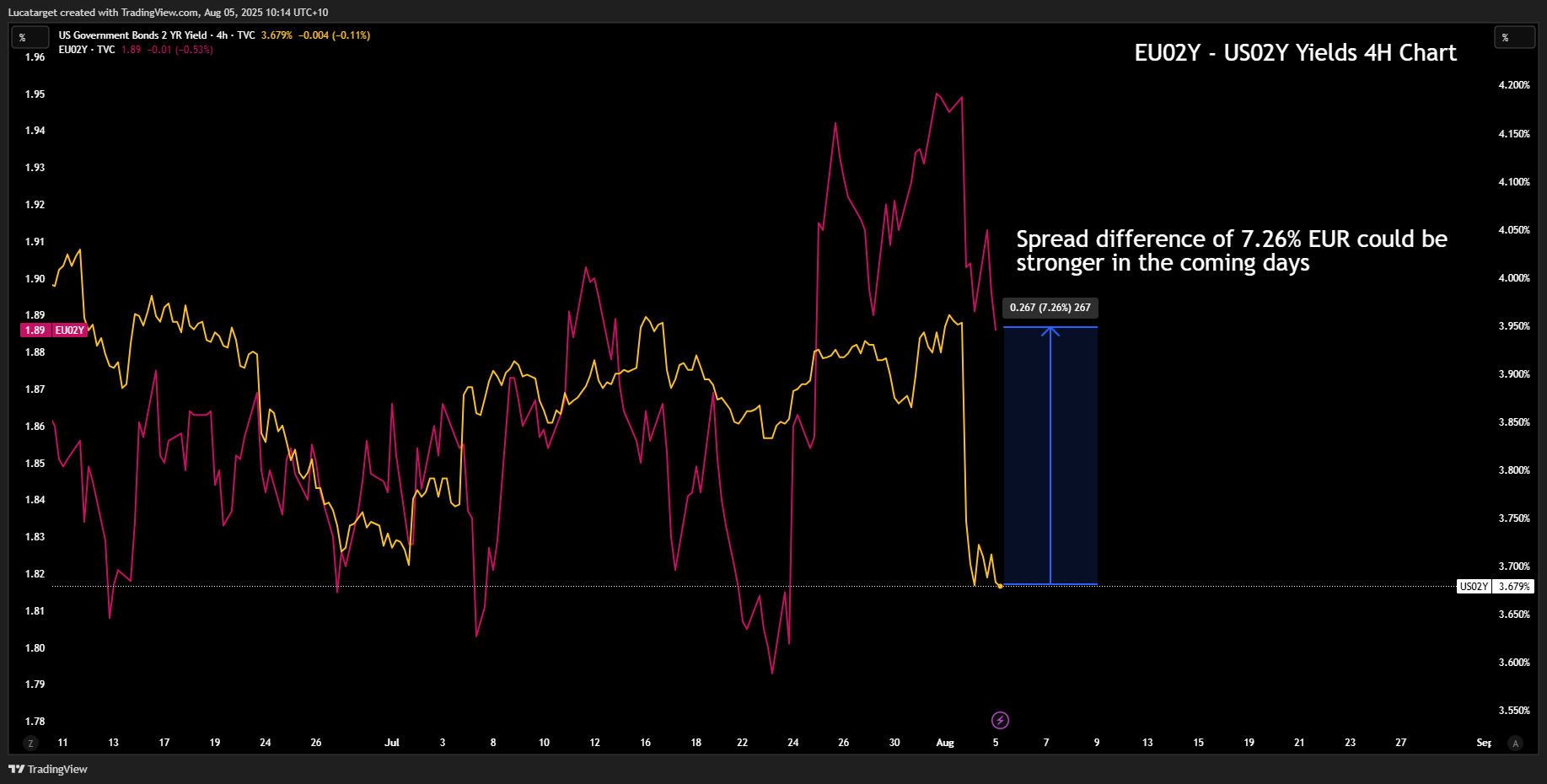

With the Fed pivoting dovish and the ECB in “hold” mode, the yield spread is starting to favor the euro again. (Yellow US Pink EU)

We’ve cleared key resistance levels and are now looking at 1.1600 as the next area of interest and possible reisstnce. I'm looking to targets near 1.1800 and 1.20 as last target, 1.1550 could be attractive for long entries.

Catalyst: Further confirmation of weak U.S. data or even neutral Eurozone numbers could be enough to drive this higher.

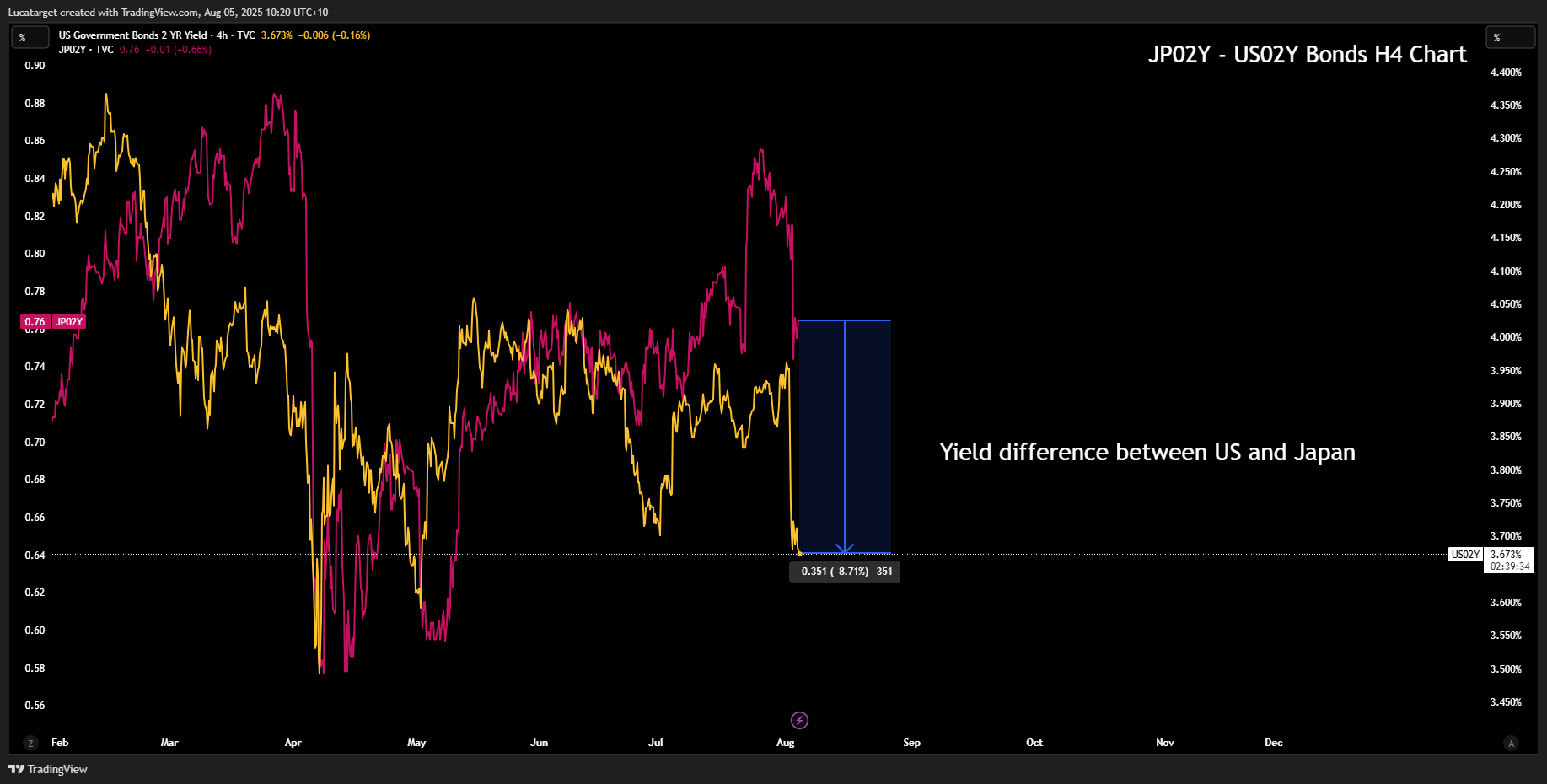

While Japanese yields remain subdued, the sharp drop in U.S. yields has made the rate differential far less compelling.

Add to that growing concerns around Fed credibility, and there’s a case to be made for downside.

Targeting a return to 144.00, with stops above 148.00. Not a swing-for-the-fences type of trade, but the risk/reward is starting to stack up, specially looking for the final target at 140.000

I’ll be keeping a close eye on incoming data, especially with Trump signaling another Fed appointment is imminent.

If the next pick is perceived as politically motivated, we could see more pressure on the dollar.

Markets are clearly in a transition phase, from inflation fears to growth fears, and when that happens, the FX market becomes reactive, not predictive. That’s where opportunity lives.

Let’s see what the rest of the week brings. Stay sharp, stay flexible and as always, trade what’s in front of you, not what you hope for.

1. Why did the U.S. dollar drop after the latest NFP release?

The dollar fell sharply because the non-farm payrolls data showed significant weakness, especially after major downward revisions. This has increased the market’s expectation of a Fed rate cut in September, reducing demand for USD-denominated assets.

2. What’s the probability of a Fed rate cut in September 2025?

Market pricing currently reflects an 90% chance of a rate cut at the September FOMC meeting, driven by weaker jobs data, deteriorating economic indicators, and political pressure on the Fed.

3. How do weaker U.S. job numbers impact forex trading?

Weaker employment data usually signals slower economic growth, prompting expectations of monetary easing. This tends to lower bond yields and push the U.S. dollar down, especially against currencies where rate expectations remain stable or hawkish.

4. What are the best forex pairs to trade during a dovish Fed pivot?

When the Fed signals a pivot, EUR/USD and USD/JPY often present opportunities. EUR/USD tends to rise as the yield spread narrows in favor of the euro, while USD/JPY can fall due to shrinking rate differentials with Japan.

5. Could political interference in the Fed impact forex markets?

Yes. Any perceived erosion of the Fed's independence, such as politically motivated personnel changes, can trigger a loss of investor confidence, adding downward pressure on the U.S. dollar and increasing volatility across major pairs.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.