just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

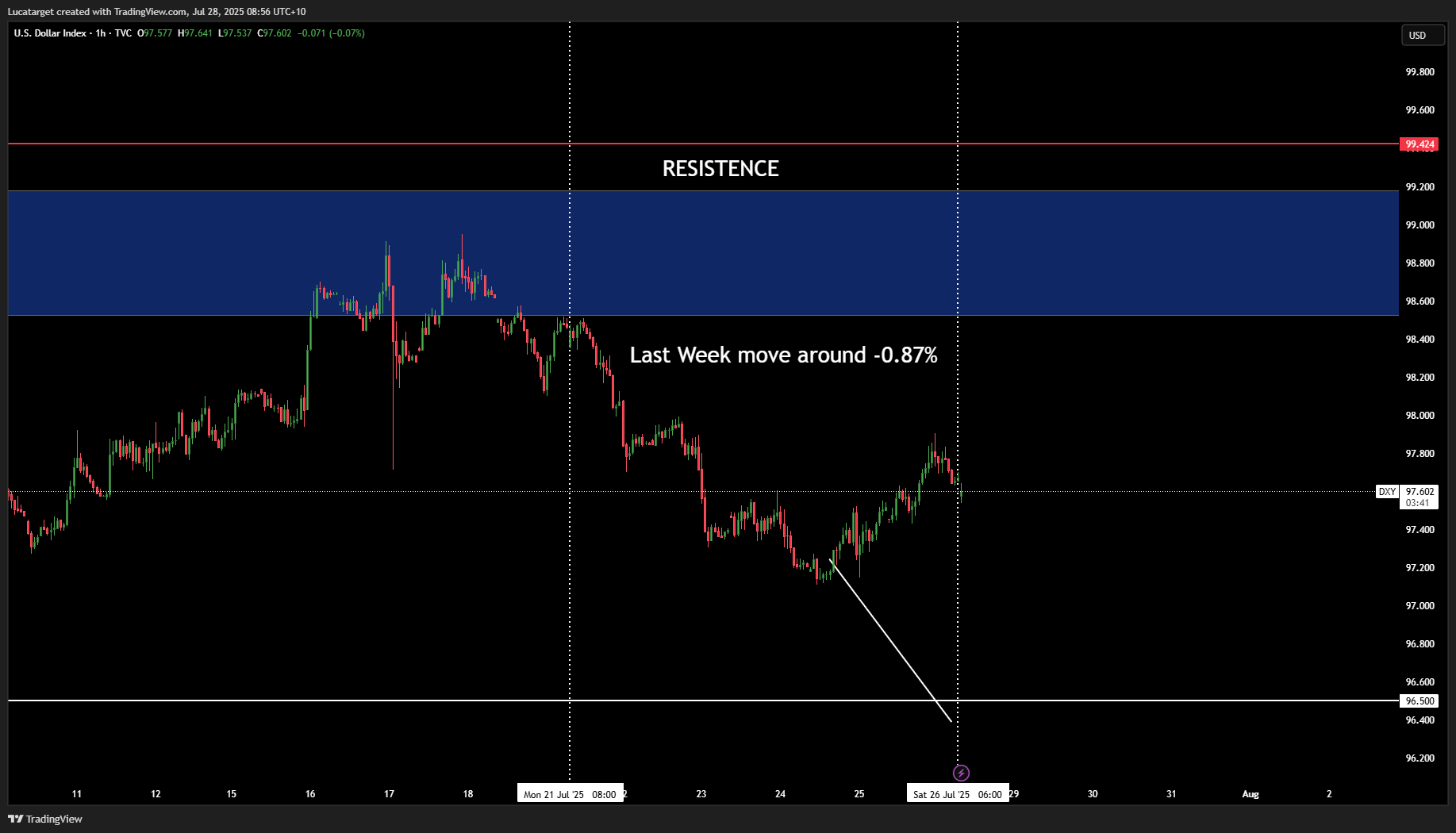

Last week ended on a firmer footing for the US dollar, but not before reminding us of just how sensitive markets still are to the interplay between monetary policy expectations and geopolitical risk.

The past few weeks have been marked by steadily declining FX volatility. With the dust settling after the US-Japan trade deal and President Trump easing his tone especially toward China the markets have breathed a cautious sigh of relief.

We’ve seen a resurgence in carry trades, with emerging market currencies like the BRL, HUF, MXN, and ZAR staging strong performances when funded by short JPY positions.(USDJPY up)

But let’s not be lulled into complacency.

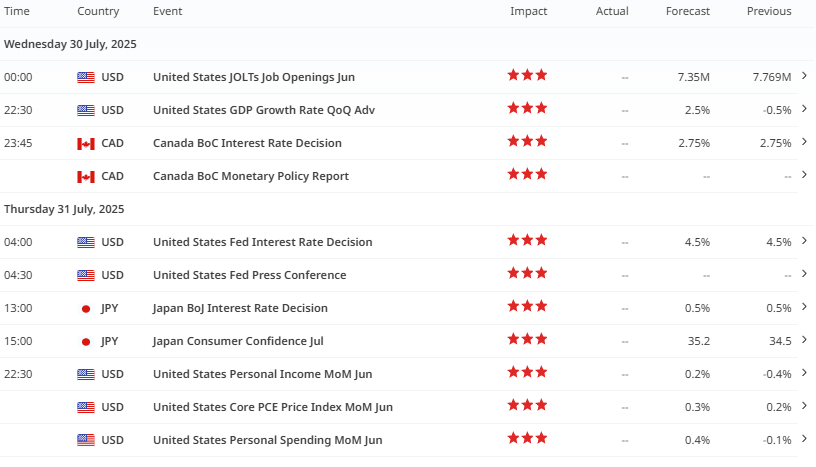

We’re heading into a packed week where three central banks, such as; the Fed, BoJ, and BoC will take centre stage, all with policy decisions due that could reshape FX flows and volatility expectations.

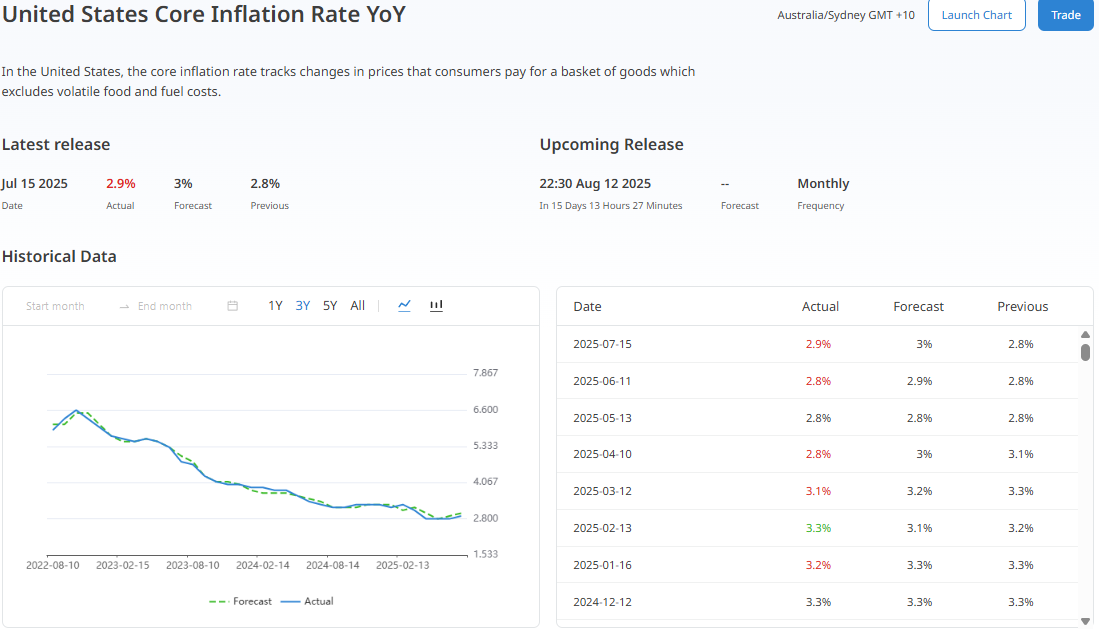

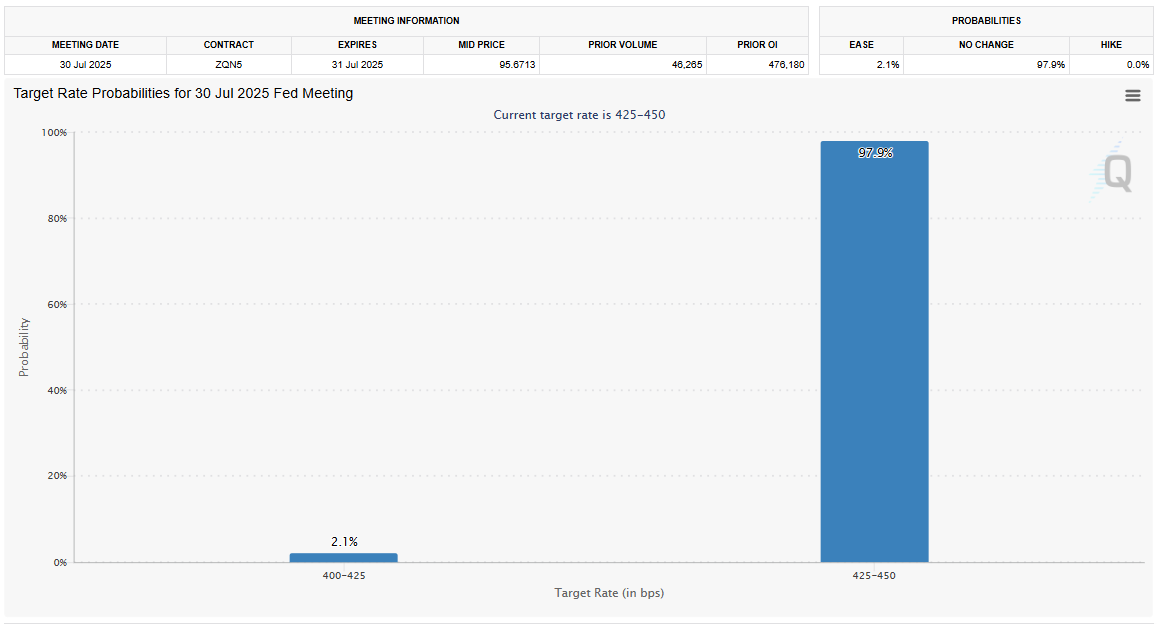

For the Federal Reserve, the tone has been remarkably steady. Recent US economic data including jobless claims and core inflation have given the Fed room to delay any immediate rate cuts.

Markets are expecting Powell to stay in “wait-and-see” mode, particularly ahead of the July Nonfarm Payrolls (due Friday), but any unexpected hawkishness could jolt risk sentiment.

If Powell surprises with language suggesting rate hikes are not off the table especially amid the recent inflationary pressure from tariff-related costs we may see the USD strengthen broadly, especially against lower-yielding currencies like the JPY and CHF.

Still, I lean toward the view that the Fed will opt for neutrality, reinforcing low volatility and, in turn, supporting carry trade appetite through the week.

The BoJ enters this week with a slightly more complicated backdrop. Deputy Governor Uchida’s recent speech struck a hawkish tone, hinting that inflation expectations are beginning to justify a return to rate hikes possibly by year-end.

However, politics might get in the way. Japan’s ruling coalition lost its majority in the upper house, and the pressure on PM Ishiba to resign is mounting.

This creates a unique tension: a central bank that wants to tighten policy versus a political system in limbo. In my view, Governor Ueda is unlikely to rattle the cage this week.

With expectations already pricing in a hike later this year, the bar is high for a further hawkish surprise.

If we’re right, and the BoJ stays balanced, USD/JPY could resume its grind higher especially as low volatility continues to incentivize JPY-funded carry positions.

Over in Canada, the BoC is widely expected to stay on hold, but what matters here is guidance. President Trump’s threats to slap 35% tariffs on Canadian goods loom large, though they may end up being softer in application or even delayed.

A dovish BoC, coupled with trade uncertainty, could put CAD under pressure particularly against the USD and possibly the EUR.

Here’s what I’ll be watching most closely this week:

Tuesday: US Goods Trade Balance & JOLTS, AU CPI

Wednesday: US GDP (expected +2.5% annualized), Canada Rate Decision, FOMC

Thursday: Japan Retail Sales & Industrial Production, BoJ Meeting, US Core PCE

Friday: Eurozone CPI, UK & Eurozone Manufacturing PMIs, US Nonfarm Payrolls (consensus: +118k)

The combination of GDP and jobs data will be critical in shaping the market’s Fed outlook through August and beyond.

In light of the current backdrop, I remain constructive on USD/JPY for the week ahead. The pair has shown resilience even amid hawkish BoJ commentary, and I believe the dovish policy divergence will continue to drive interest.

The 150–153 zone could be tested again if Powell maintains a cautious stance and Japanese politics remain murky.

I also continue to favour long EUR/GBP, especially with the ECB holding firm on rates while the UK continues to face a tricky macro-fiscal environment.

The divergence between monetary policy paths and upcoming tax considerations in the UK Autumn Budget make sterling vulnerable.

What really strikes me heading into this week is the underlying fragility of global macro calm. Markets are behaving as if policy is predictable and geopolitical tension is fading but that assumption may not hold.

China and the US are still in delicate negotiations, and while Trump has toned down the rhetoric (possibly with the election cycle in mind), we know how quickly that can change. Over the weekend, there were no new flare-ups, but investors should stay nimble.

We’re in a moment where carry rules, but I’ll be watching for the spark that could bring volatility back in force.

Q1: Why is volatility so low right now, and how does that impact FX trading?

A: Volatility has declined due to easing trade tensions especially after recent deals involving the U.S., Japan, and Southeast Asian nations and central banks taking a more measured policy approach. This low-volatility backdrop favors carry trades, where investors borrow in low-yielding currencies like the JPY to invest in higher-yielding ones, sustaining risk-on momentum in FX markets.

Q2: What should traders expect from the Federal Reserve this week?

A: The Fed is expected to keep rates on hold. Although inflation has picked up slightly, recent data doesn't justify immediate rate cuts. Powell is likely to remain cautious, signaling a “data-dependent” stance. Markets will look for clues on whether the Fed still intends to cut rates later this year any deviation could move the USD sharply.

Q3: Is the Bank of Japan turning more hawkish?

A: There are signs of a shift. Deputy Governor Uchida delivered a speech with a more hawkish tone, hinting at potential rate hikes later in the year. However, due to political uncertainty following Japan’s upper house election and PM Ishiba’s weakened position, the BoJ is unlikely to act in the short term. Markets are pricing in future tightening, but Governor Ueda is expected to be cautious this week.

Q4: How are political risks in Japan affecting the yen?

A: The LDP's loss of a majority has introduced political instability, making it difficult for investors to confidently back the yen. Despite expectations for higher BoJ rates, these gains have quickly faded. The market now sees continued weakness in JPY as more likely especially with favorable global conditions for carry trades.

Q5: What are the top FX trade setups to consider this week?

A: Two trades stand out:

Long USD/JPY: With low volatility, dovish Fed tone, and no immediate BoJ action, the dollar-yen pair could grind higher toward the 150–153 zone.

Long EUR/GBP: As the ECB holds firm and the UK faces a softer economic outlook and fiscal tightening risks, the euro may continue to gain ground against the pound.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.