just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

Markets have entered a period of heightened fragility, with risk sentiment caught in the crossfire between geopolitical tensions in the Middle East and an increasingly uncertain monetary policy backdrop in the U.S. and Europe. While the headlines remain dominated by the Israel-Iran conflict and its broader ramifications, market participants are also recalibrating expectations around central bank actions especially the Federal Reserve following persistent signs of sticky inflation.

Let’s start with the geopolitical front. The recent flare-up involving Iran’s retaliatory strike on Israel was initially met with market fear, but asset prices quickly rebalanced once it became clear that both sides were keen to avoid an all-out war. Despite the temporary shock, financial markets interpreted the action as largely symbolic. Oil prices spiked momentarily but failed to sustain momentum, reflecting both ample supply buffers and a perception that the conflict, for now, lacks the kind of escalation risk that would severely threaten energy flows.

However, we shouldn't be complacent. While diplomacy may be containing immediate fallout, the situation remains fluid. Any miscalculation could reignite volatility, particularly in oil markets. It's worth noting that Brent crude still trades with a geopolitical risk premium embedded, and any sudden deterioration could renew upward pressure on prices something central banks will be closely watching.

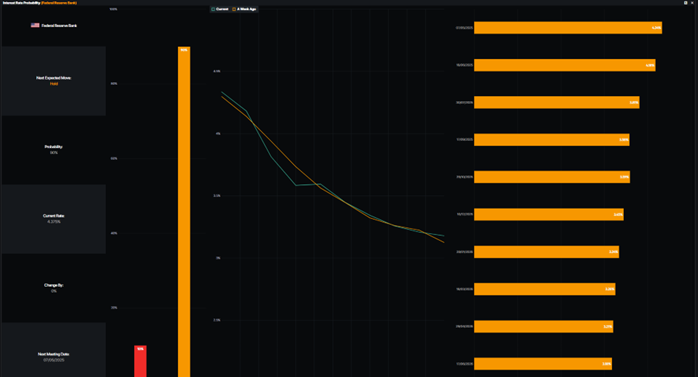

On the monetary policy side, the Fed’s path forward is becoming increasingly murky. After a string of hotter-than-expected CPI prints, the disinflation narrative is under pressure. March inflation, for instance, showed renewed momentum in core services, reinforcing the notion that inflation is proving more persistent than policymakers anticipated. As a result, market pricing for rate cuts has shifted significantly from as many as six cuts expected at the start of the year to perhaps just one or two now being priced in.

Fed Chair Powell has maintained a cautious stance, emphasizing the need for more evidence before committing to any easing cycle. This aligns with recent speeches from other FOMC members, who have flagged concerns about reacceleration risks and urged patience. Simply put, the bar for rate cuts has risen.

Global markets are now repricing accordingly. U.S. yields have climbed, the dollar has regained some strength, and equities while still supported by strong earnings are showing signs of stress at the margin, especially in rate-sensitive sectors. The message is clear: monetary easing is not a given.

Across the Atlantic, the European Central Bank is still hinting at a June rate cut, but that too depends on upcoming data. Wage dynamics in Europe remain a concern, and like the Fed, the ECB doesn't want to move prematurely and risk a resurgence of inflation pressures.

Layered atop these macro variables is the ever-present role of energy markets. While the initial Middle East escalation didn’t produce a sustained oil rally, the structural tightness in crude markets remains relevant. Inventories are below average, OPEC+ production discipline persists, and demand forecasts are being revised upward, especially as China stabilizes and global air travel rebounds.

Adding to the mix is the shift in investor sentiment toward gold. In the face of geopolitical uncertainty and doubts about the timing of rate cuts, gold has surged to record highs, supported by strong central bank demand and growing retail interest. It’s a sign that investors are seeking hedges not just against inflation, but against broader systemic risks.

We’re navigating a market regime where binary outcomes are increasingly possible. Either inflation cools convincingly, unlocking rate cuts and supporting risk assets, or it persists forcing central banks into a prolonged holding pattern. Meanwhile, any flare-up in geopolitical tensions could upset even the most well-laid forecasts.

In this kind of environment, flexibility is paramount. Portfolio strategies need to balance duration risk with inflation hedges, maintain exposure to real assets like commodities and gold, and remain nimble in FX particularly as the dollar's path becomes more data dependent.

The weeks ahead will be pivotal. U.S. CPI, PCE inflation, and any fresh signals from the Fed could reshape the outlook again. Simultaneously, the Middle East remains a wild card, and oil traders will be watching every headline.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

cBridge, by Spotware, has launched Markout Report, a risk intelligence module that lets brokers detect toxic flow, rank accounts by financial impact and act before losses accumulate, all within the bridge.

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.