just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

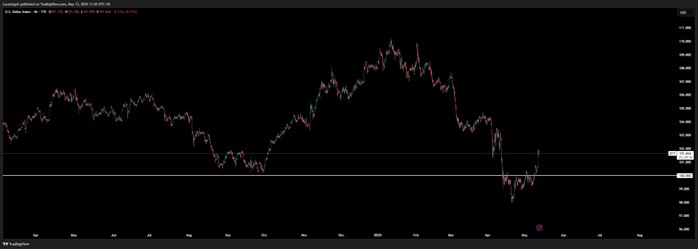

The U.S. dollar is trying to find its footing again, staging a modest recovery this month after a bruising decline in April. On the surface, things look better: DXY is back above 100, equities are climbing again, and markets seem momentarily relieved by Washington’s latest round of trade diplomacy. But none of this changes the deeper trajectory confidence in U.S. policy credibility remains damaged, and the rebound still feels more like a pause than a turning point.

The recovery was triggered in part by the Trump administration’s recent trade deal with the UK, a headline-grabbing move that reduced tariffs on specific sectors like autos and steel. But let’s be clear this was no reset. The broader 10% universal tariff remains untouched, and rhetoric from the White House suggests that future deals with other countries will be less generous, especially those with large trade surpluses. Also, with US China trade deal this weekend, rollback from 145% tariffs to around 30%.

What we’re watching is more tactical than strategic. These are short-term efforts to cushion market volatility and reclaim narrative control, not a signal that the U.S. is pivoting toward greater international cooperation. Trump has even hinted the lowest tariff rates offered to other countries after signing deals will be “much higher” than past norms. So, while some are calling this a relief rally, it’s better understood as a reaction to slightly lower chaos not improved fundamentals.

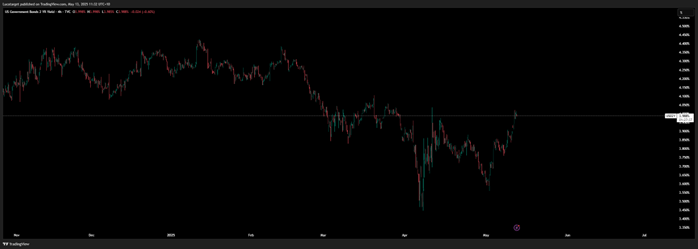

On the monetary side, the Federal Reserve has stuck to its “wait and see” messaging. Powell made it clear this week: the data doesn’t justify action yet, and the Fed isn’t about to pre-empt the next move without a clearer view. The labour market hasn’t cracked at least not visibly, and inflation hasn’t softened enough to justify a cut. As a result, the market has begun dialling back expectations of imminent easing, with rate cut pricing for June and July now fading.

This has helped lift U.S. yields slightly, and by extension, the dollar. But let’s not lose the forest for the trees. The correlation between short-term rate spreads and USD performance has weakened, and a notable disconnect has opened possibly reflecting the political risk premium building into U.S. assets. Markets are hedging not just interest rates but institutional credibility.

Outside the U.S., the FX landscape is beginning to stir more broadly. The most eye-catching move has come from Asia, where Taiwan’s dollar (TWD) surged nearly 9% in just a few days. There’s growing speculation that Taiwan may be quietly adjusting its FX policy, potentially reducing intervention to stay in Washington’s good graces ahead of trade talks. That strength has rippled across the region, with the KRW and THB catching some tailwinds. Meanwhile, China’s RMB remains relatively stable Beijing seems intent on anchoring regional currency stability through USD/CNY control.

Interestingly, G10 currencies haven’t fully mirrored the Asia FX story. The AUD, NZD, and JPY all strengthened earlier this week but quickly faded again. This suggests that the market’s shift is still local, not systemic at least for now.

Positioning data reinforces this: leveraged funds have been offloading dollar longs for over three months straight, with the latest data showing the biggest short USD positioning since last October. The most aggressive short interest is clustered around the yen, euro, and pound. Yet traders still hold long USD positions against the AUD and CAD, suggesting there’s caution about high-beta commodity FX while global growth wobbles under policy stress and tighter financial conditions.

Correlation dynamics are also changing. Over the past month, we saw a sharp rise in risk-off behaviour gold, yen, and Swiss franc all clustering as safe havens. But more recently, these clusters have faded. This tells me one thing: the loss of confidence in the dollar hasn’t fully vanished, but it’s becoming more nuanced. The market isn’t running to the exits anymore but it’s still pacing nervously near the door.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.