just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

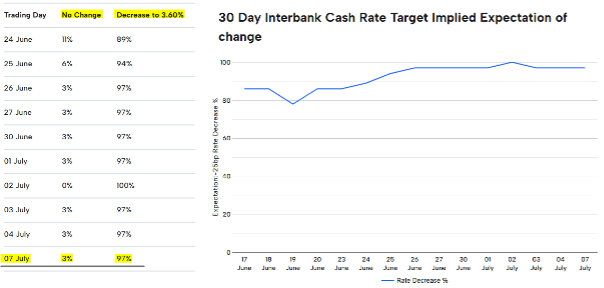

As the Reserve Bank of Australia (RBA) meets today at 2:30pm Sydney time, market participants and landlords are watching with heightened anticipation.

While no decision has yet been made, the probability of another 25 basis point cut is being priced in with conviction, but a high probability is already awaited.

If confirmed, this would mark the third cut in 2025, potentially reducing the official cash rate to 3.60%, its lowest level since the pandemic era.

More importantly, it would represent the first instance of back-to-back rate cuts by the RBA in over a decade a decisive signal that Australia's monetary policy cycle has turned a corner.

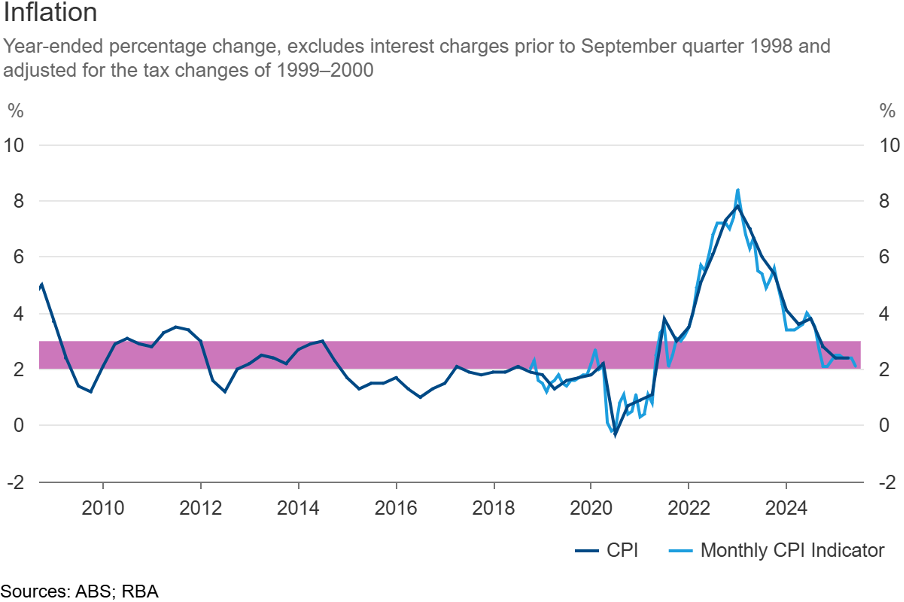

The RBA’s policy shift reflects a broader recalibration of expectations in response to slowing economic momentum.

Inflation, while still above target, has shown signs of easing in recent quarters.

Consumer confidence remains soft, wage growth is tepid, and GDP growth is struggling to keep pace with population increases. In short: monetary conditions are too restrictive for a slowing economy.

Recent RBA communication has subtly hinted at this transition. While not explicitly dovish, the tone has softened indicating that policymakers are increasingly concerned about the downside risks of overtightening.

With the unemployment rate ticking higher and retail spending plateauing, the argument for pre-emptive easing becomes compelling.

If the cut is delivered today, it will not be a reactive decision it will be a forward-looking move designed to support demand, ease mortgage stress, and prevent an unnecessary contraction in credit-sensitive sectors like housing and construction.

For households, especially those with variable-rate home loans, this rate cut could offer tangible monthly relief.

According to estimates, a 25 bps cut on a $600,000 mortgage equates to a monthly saving of roughly $90 to $100, depending on the lender.

If this is the third cut in a row, total savings this year could exceed $250 per month for average-sized loans.

But beyond the immediate cash-flow benefit, there’s a deeper implication: psychological relief. Many borrowers stretched their budgets during the ultra-low-interest rate era.

The aggressive tightening cycle from 2022 to 2024 shocked household finances. Easing that pressure restores not just liquidity but confidence.

It’s important to note that this relief depends on whether banks pass through the full cut. With funding costs still elevated in wholesale markets, not all lenders may be inclined to deliver the full benefit to borrowers.

The RBA will likely monitor this closely and pressure institutions to ensure monetary policy flows through effectively.

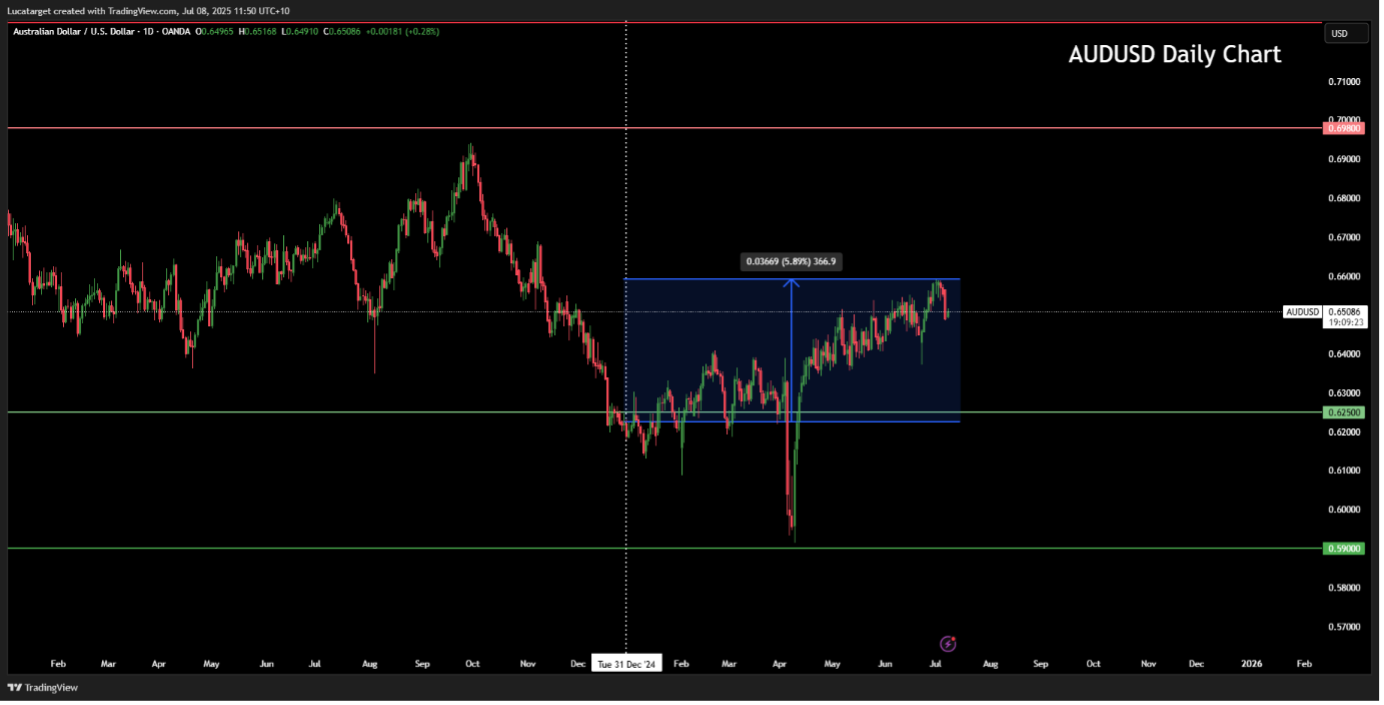

On the FX side, logic would suggest that lower rates weaken the Aussie dollar. After all, rate differentials matter, and as the RBA eases while the Fed and ECB hold firm, interest rate spreads narrow.

But the AUD has proven resilient. In 2025 alone, the AUD/USD pair has appreciated by over 6%, supported by:

So, would a third rate cut finally dent the AUD’s strength?

Not necessarily.

Here’s why:

Markets have likely priced it in: The expectation of today’s cut is already embedded in AUD futures and currency options markets.

Global rate convergence: If the Fed begins signalling cuts later in the year something bond markets are already speculating the AUD may maintain its relative appeal.

Real yields remain attractive: Despite nominal cuts, Australia still offers positive real yields, especially when compared to Japan or parts of Europe.

In short, unless the RBA surprises with a larger cut or explicitly dovish forward guidance, the downside for AUD may be limited.

In fact, a relief rally is possible if the central bank delivers a cut without accompanying pessimism.

Why is the RBA expected to cut rates again today?

The RBA is responding to signs of a slowing economy subdued wage growth, weakening consumer sentiment, and inflation that is gradually easing. With unemployment rising and retail spending flatlining, the central bank is likely seeking to support demand and avoid a credit contraction, particularly in housing.

What would be the significance of a third rate cut in 2025?

If confirmed, this would lower the official cash rate to 3.60% the lowest since the pandemic and mark the first back-to-back rate cuts in over a decade. It would signal a clear pivot in Australia’s monetary policy cycle toward stimulus and accommodation.

How will this rate cut affect mortgage holders?

A 25 basis point cut could save roughly $90 to $100 per month on a $600,000 mortgage. With three cuts in 2025, total annual savings could exceed $3,000 for variable-rate borrowers. However, the extent of relief depends on whether banks pass on the cut fully to customers.

Could this cut weaken the Australian dollar (AUD)?

Not necessarily. Although lower rates typically weaken a currency, the AUD has remained resilient, supported by commodity demand, strong trade balances, and global investors seeking relative value. Unless the RBA surprises markets with deeper cuts or dovish guidance, the AUD may remain stable or even rally slightly.

What should we watch for beyond the rate decision?

The RBA’s forward guidance is crucial. Markets will look for clues about whether this is the end of the easing cycle or the beginning of a broader shift. If the RBA remains cautious and balanced, rate expectations may stabilize. But if it leans dovish, more cuts could be priced in for late 2025.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

cBridge, by Spotware, has launched Markout Report, a risk intelligence module that lets brokers detect toxic flow, rank accounts by financial impact and act before losses accumulate, all within the bridge.

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.