just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

Despite all the noise, the Bank of Japan played it safe. The policy rate stayed at 0.50%, and they merely tweaked their bond-buying program, saying they’ll slow down the pace starting April 2026. Nothing major, and the FX market shrugged USDJPY barely moved, still hovering just under 145. The real takeaway? The BoJ is walking a tightrope. Governor Ueda made it clear that uncertainty especially from global trade and geopolitical tensions is keeping the bank from tightening more aggressively. Unless we see a sudden surge in inflation or a major shift in global risk appetite, the yen's path will remain tied to external factors namely, long-end yield spreads and safe-haven flows.

Now, zoom out to the broader battlefield literally.

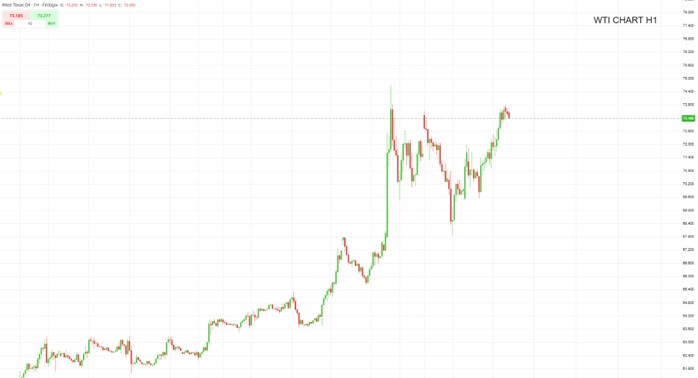

The Israel-Iran conflict remains the biggest wildcard on traders' radars. Over the weekend, markets took some relief in reports that Israel hadn’t struck Iran’s oil infrastructure at least, not yet. Oil prices briefly dropped back below $71 before bouncing toward $75 overnight, a sign that traders are playing this one hour by hour.

But this is no lull. Behind the scenes, Iran is reportedly reaching out via Arab intermediaries, signalling openness to resume nuclear talks if the U.S. stays out of the strikes. Meanwhile, Israel isn’t budging. Officials are planning at least two more weeks of military operations, clearly aiming to dismantle Iran’s missile and nuclear capabilities.

President Trump who left the G7 early to “attend many important matters” isn’t helping calm the waters. His social media tirade over Iran “wasting human life” and reiterating “IRAN CAN NOT HAVE A NUCLEAR WEAPON” is escalating the rhetoric, if not the conflict itself.

Bottom line: the market is still pricing in hope, not escalation. There’s a fragile belief that as long as oil keeps flowing, risk appetite can survive. That’s a dangerous assumption.

What does that mean for the dollar and risk assets?

The USD is weaker this week, with high-beta G10 currencies like AUD and NZD catching a bid as risk sentiment improves. But let’s be honest this isn’t confidence, it’s complacency. The lack of an oil shock has lulled markets into a sense of temporary calm, but if we get even one confirmed strike on energy infrastructure or pipelines, this all turns fast. A sustained rally in crude above $80 would likely reignite USD (DXY) demand on global growth fears and boost safe haven flows into the dollar and the yen.

Also keep in mind: US retail sales are coming in today. Any signal of consumer weakness especially after last month’s inflation surprise could reinforce bets that the Fed is done hiking and might even have to pivot sooner than expected. That would add fuel to the dollar sell-off.

My positioning mindset right now?

I'm already long USDJPY, looking for a resumption of yen weakness if bond spreads widen again. But I’m also watching for tactical opportunities to fade risk-on rallies in AUDUSD or NZDUSD especially if oil spikes again or geopolitical risk re-escalates.

If things flare up further in Tehran or if Trump hints at US intervention watch gold and oil rip higher. And watch USDCHF and USDJPY diverge: the franc may outperform as a geopolitical haven, while the yen’s safe-haven status remains muted unless Japan’s own data deteriorates.

Q1: Why didn’t the Bank of Japan’s decision move USDJPY significantly?

A1: Because markets expected no change. The BoJ held rates steady at 0.50% and only slightly adjusted its bond-buying program news that was already priced in. Without a surprise or shift in forward guidance, traders saw little reason to reprice the yen. The real driver of USDJPY remains U.S.-Japan yield differentials and global risk sentiment, not BoJ tweaks.

Q2: How does the Israel-Iran conflict affect currencies and commodities?

A2: It introduces event-driven volatility. Traders are watching for any escalation that could disrupt oil supply. A direct hit to Iran’s energy infrastructure could send crude prices soaring past $80, triggering safe-haven demand for the USD and CHF. In contrast, temporary de-escalation or diplomatic progress tends to lift risk assets like AUD, NZD, and EMFX.

Q3: Why is the U.S. dollar weakening despite geopolitical tensions?

A3: Because markets are currently betting on a soft-landing scenario. With no immediate oil shock and signs of slowing U.S. inflation, investors are reducing bets on further Fed hikes. This “relief rally” in risk assets is weakening the dollar but it’s fragile. A geopolitical flare-up or poor U.S. retail data could flip sentiment quickly.

Q4: What would cause oil to spike sharply from here?

A4: A confirmed strike on Iranian energy infrastructure, disruption to regional pipelines, or U.S. military involvement. Any of these would likely push crude back above $80 and potentially into triple digits depending on the scale of damage or intervention. This would amplify inflation fears and force a repricing of risk across FX and commodities.

Q5: What’s the biggest market mispricing right now?

A5: Complacency around energy risk. Markets are assuming oil flows will remain uninterrupted, despite escalating rhetoric and military activity. If this assumption is wrong, we could see a sharp reversal in risk assets and renewed demand for USD and hard commodities. Traders should be hedged for tail risk.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.