just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The FX market has entered a "wait and see" phase following President Trump's confirmation of new tariff hikes on steel and aluminium. Effective March 12, a 25% tariff will apply to all imports of these metals without exceptions—at least initially. The White House emphasized that this move aims to revive domestic manufacturing and protect American industry. However, President Trump has hinted at a possible exemption for Australia, citing the country’s substantial investment in the U.S. steel sector and its critical role in defence manufacturing. I’ve done a blog yesterday mentioning how it would work, you can find the blog HERE

The administration justifies these tariffs under Section 232 of the Trade Expansion Act, framing them as a national security measure (If you would like to read the full article CLICK HERE). Unlike the 2018 tariffs that mainly targeted raw materials, the new round extends to finished products, such as extrusions and slabs, which could have broader implications for U.S. consumers and manufacturers. The administration argues that past exemptions were exploited by exporters, prompting a more comprehensive approach this time.

Financial markets have so far taken a measured response. The U.S. dollar has held steady, supported by strong nonfarm payroll figures, which suggest continued economic resilience. Meanwhile, the Australian dollar—despite speculation over a potential exemption—remains one of the top-performing G10 currencies this year, buoyed by rising commodity prices.

A key question is how trading partners will respond. The European Union retaliated in 2018 by imposing tariffs on iconic American goods, including motorcycles and denim. Meanwhile, past U.S. tariff measures have proven costly; an analysis by the Peterson Institute for International Economics estimated that the 2018 steel and aluminium tariffs resulted in a per-job cost of approximately $650,000 due to higher consumer prices and reduced manufacturing competitiveness.

Emerging markets could face heightened risks. The Trump administration has announced "reciprocal tariffs," meaning countries imposing higher import duties on U.S. goods than vice versa could be targeted next. This disproportionately affects nations like India, Thailand, Argentina, South Africa, and Brazil, all of which maintain relatively high tariff structures. The recent appreciation of several emerging market currencies, such as the Brazilian real and Chilean peso, may be tested if trade tensions escalate.

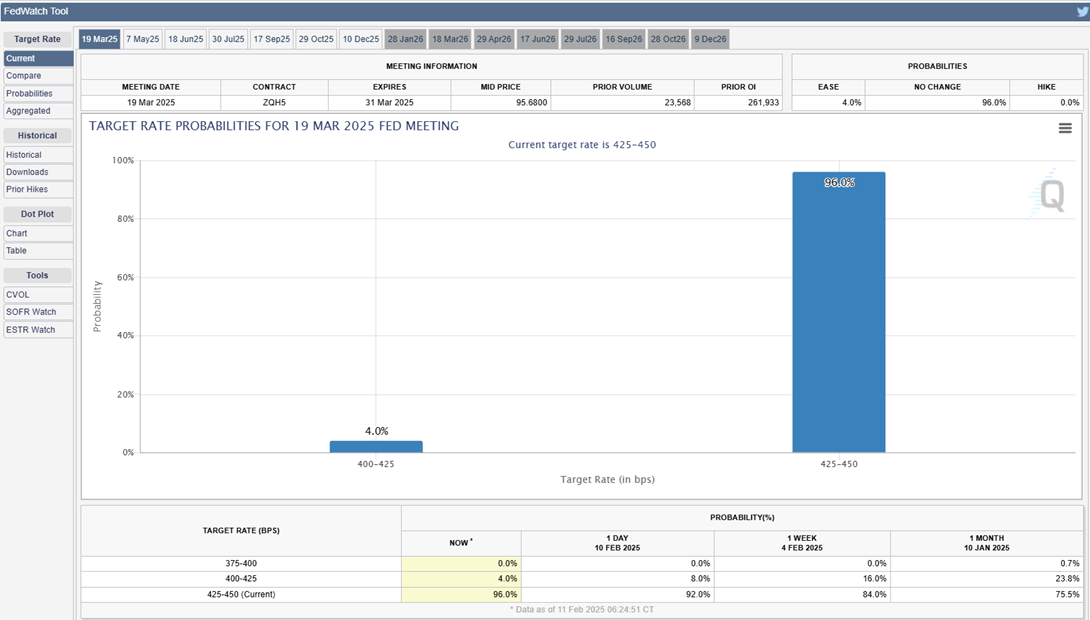

With the Federal Reserve maintaining a cautious stance on rate cuts amid strong labour data, the tariff debate injects another layer of uncertainty into the economic outlook. Historically, higher tariffs have led to increased inflationary pressures, which could complicate the Fed’s decision-making process.

Additionally, political factors cannot be ignored. The Australian government is pushing hard for an exemption ahead of its upcoming election, arguing that Australian steel is a critical input for U.S. manufacturing, particularly in defence-related sectors. Meanwhile, Trump’s aggressive trade policy plays into his broader election-year strategy, reinforcing his "America First" stance while setting the stage for potential negotiations.

The latest steel and aluminium tariffs mark a significant shift in U.S. trade policy, potentially straining relations with key allies and disrupting global supply chains. While markets remain calm for now, the real test will come in March when the tariffs take effect. How other nations respond—and whether exemptions are ultimately granted—will shape the trajectory of global trade in the months ahead. Traders and policymakers alike should brace for volatility as the situation unfolds. I do believe on a potential long on AUD if Trump decides to not go ahead with tariffs in Australia on March 12.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.