just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

Technical Outlook: Foreign Markets Rise as Investors Hedge Against U.S. Economic Risks

Currency Overview

USD – Tariff Tension Meets Exhaustion

JPY – No Relief in Sight

AUD – Bullish Reversal Gaining Ground

NZD – Cautious but Capped

EUR – Stuck in Stagnation

GBP – Lacking Fuel for Breakout

CAD – Quiet Strength Beneath the Surface

CHF – Flatlined

As doubts grow around the strength of the U.S. economy, global investors are turning their attention—and capital—toward emerging markets. With trade policy uncertainties mounting and the U.S. dollar losing steam, capital is flowing into riskier but potentially more rewarding regions.

What’s Fueling the Shift:

Economic momentum in the U.S. is showing signs of fatigue, especially as the threat of a 25% tariff on select imports looms on April 2. This is raising fears of inflationary pressure and supply chain slowdowns, creating a risk-off tone around U.S. assets.

As the greenback pulls back from recent highs, emerging-market currencies are finding room to rally. Investors are betting the dollar will weaken further if U.S. trade restrictions escalate or if economic data underwhelms.

Asset managers are reducing U.S. exposure and rotating funds into emerging economies like Brazil, India, and South Africa—regions offering higher yields, more attractive valuations, and less sensitivity to U.S. policy moves.

For many, emerging markets are serving a dual purpose: a hedge against U.S.-led volatility and a way to re-engage with global growth outside of the dollar-centric narrative.

Gold vs Dollar: Offloading on the Greenback

With risks still looming in the US amidst impending tariffs on April 2, large institutions are now off-loading some of their positions on Dollar and increases their bets on Gold.

The U.S. is set to introduce a series of new tariffs on April 2, 2025, targeting key sectors like automobiles, energy, and trade reciprocity. The move is part of the administration's broader push to bolster domestic industries and rebalance perceived trade inequities—but it’s also stirring concerns about inflation, trade retaliation, and the strength of the U.S. Dollar.

Key Tariffs Taking Effect April 2:

1. 25% Tariff on Imported Cars & Auto Parts

2. Secondary Sanctions on Countries Buying Venezuelan Oil

3. Reciprocal Tariffs on Select Trade Partners

While tariffs are aimed at protecting U.S. industries, the currency market is reacting with caution. Here’s how the dollar is being influenced:

Result: While the dollar saw a temporary boost on haven demand, sentiment is now turning bearish, especially if tariffs go into full effect and start dragging on the real economy.

Looking Ahead:

April 2 could prove to be a key inflection point—not just for trade policy, but for markets broadly. If fully enforced, these tariffs may tilt the U.S. economy toward slower growth, with ripple effects across inflation, equities, and the currency.

For dollar-watchers and macro traders, this isn’t just a trade issue—it’s a potential monetary and market narrative shift.

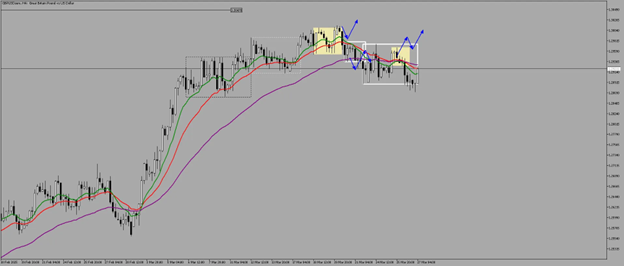

4-Hour

Dollar is still on a bullish sequence with highs and lows still intact.

But recent upside moves suggest that despite its rebound on the upside, Dollar struggles to sustain the moves with frequent sell-offs (shaded in red) after the run-ups (shaded in green).

1-Hour

A break of the 103.944 level could trigger more signs of weakness on the Dollar.

This could also potentially send the Dollar to 103.759 level that could be a catalyst for the Dollar’s further downside potential.

4-Hour

Yen continues to weaken amidst a dovish BoJ. A break of the 747.1 level could trigger further weakness on Yen and sending currencies paired with it to the upside.

USDJPY

4-Hour

USDJPY still does not exhibit any signs of weakness as the USD is more hawkish vs JPY.

The 50 MA can be a bounce level for USDJPY for upside potential with a draw on 151 level.

A break of the 151 could trigger price to draw to 151.30 level.

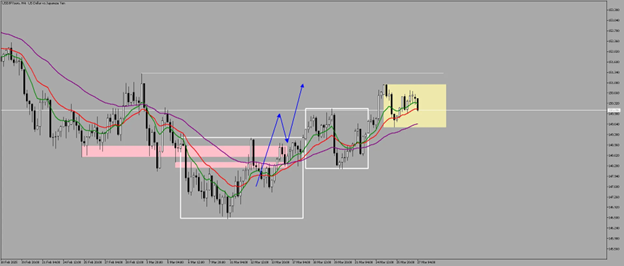

4-Hour

We have now shifted from bearish to bullish after the Aussie Dollar took out the 0.631 level.

A stronger bullish bias can be anticipated if we breakout of the range at 0.633 level. We can look for breakout trades with confluences of price trading above the moving averages.

1-Hour

As long as we remain above the equilibrium level, we could see the Aussie to maintain its bullish stance and potentially, hitting the breakout level.

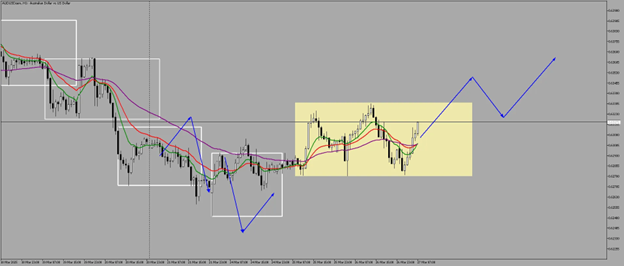

4-Hour

Compared to AUD, NZD lacks momentum for an upside move as we are ranging with high volatility inside the crossfire zone.

For confirmed strength, its best to approach NZD with caution, awaiting a potential breakout.

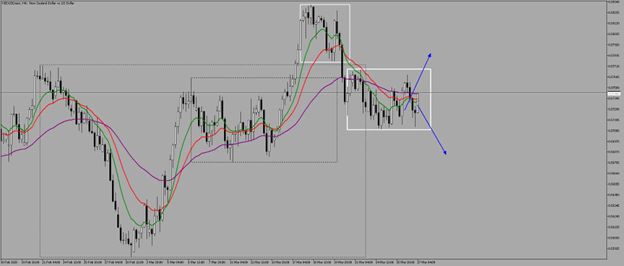

4-Hour

Looking at AUDNZD, we can see that AUD is gaining traction over NZD. If we are going to look for a better trade, AUDUSD is the better trade for longs.

4-Hour

Despite Dollar’s weakness, the Eurozone is not getting much traction as we are still trading below moving averages and Euro is currently on a bearish sequence with no signs of recovery for a potential upside.

1-Hour

Unless we breakout of the 1.07308 - 1.07954 level, further downside is still intact with Euro.

4-Hour

Dollar tried to weigh down the Pound as it failed to breakdown the range and only “wick-ed” the lows. GBP is still lacking momentum for an upside continuation.

A renewed strength can be anticipated if we break past the 1.298 level and potentially, hitting the 1.30 level for new highs.

The EUR and GBP have been stalling for some time, partly due to a slowdown in aid and strategic support from the EU and UK to Ukraine in the ongoing conflict with Russia. This perceived hesitation has weighed on investor sentiment, diminishing the appeal of European markets.

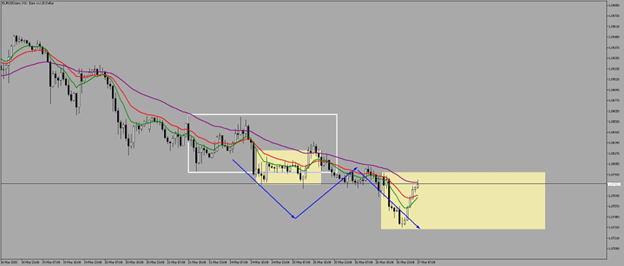

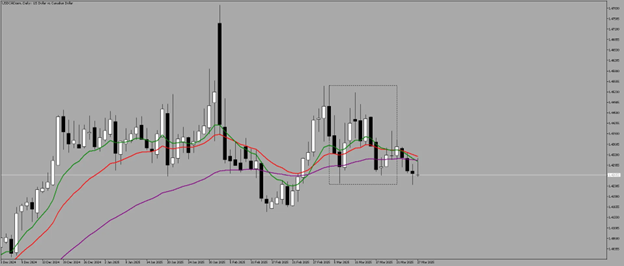

Daily

With Canada’s retaliatory stance on the United States, we could see who’s winning the tug on USDCAD.

4-Hour

Though overall, the USDCAD is still on a big range-bound environment, we could see signs of weakness over the US Dollar as USDCAD is threading below the equilibrium of the range.

A breakdown of the support level could trigger more downside for the USD and upside on CAD.

Daily

With the Swissie, there’s still no signs of momentum either on the upside or the downside.

With this lack of momentum, its best to look for alternative markets that exhibits an obvious momentum or direction.

Overall, FX markets are entering a compression phase, with pressure building across major pairs. The upcoming U.S. tariffs on April 2 could serve as the spark for a broader move—especially for USD-crosses.

“In times of uncertainty, the market doesn’t whisper—it waits. And when it moves, it moves fast.”

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.

Want to master the markets? A winning trading mindset beats a perfect strategy. Learn how emotional discipline helps you conquer fear and avoid heavy losses.

Read our latest Gold price action forecast to see how a double top pattern triggered a massive XAU/USD selloff.

Wondering how the API weekly report impacts oil prices? Learn how U.S. crude stockpiles and voluntary surveys predict the official EIA report.

cTrader Mobile 5.9 introduces a dedicated charts tab, single-tap chart access, a draggable floating action panel and a new focus mode for positions and orders, following the platform's Best Mobile Trading App win at UF Awards Global 2026. Sergey Borisov of Spotware comments on the update.

BitPay B.V., the European arm of BitPay, has been authorised as a crypto-asset service provider under MiCA by the Dutch AFM, allowing it to offer regulated crypto and stablecoin payment services, cross-border payments, and consumer spending tools across the EU.

Spotex has appointed Joe Tuccio, previously Head of Digital Partnerships at Seabury Capital, as Head of Digital Assets. Tuccio brings 20 years of financial markets experience and will lead partnerships with liquidity providers and custodians as Spotex expands its institutional FX venue into digital assets.