just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

Markets continue to grapple with a world that's becoming increasingly difficult to read, and the dollar is a prime reflection of that confusion. The latest data out of the U.S. paints a picture that’s hard to ignore a clear loss of economic momentum just as inflation expectations begin to creep higher. First quarter GDP tracking has been cut sharply to -0.8% QoQ annualized, a significant miss compared to even the downgraded consensus. Labour market data isn’t offering much reassurance either, with job openings falling faster than expected and consumer confidence slipping to levels last seen in the depths of 2020. At the same time, short-term inflation expectations are edging up, raising the uncomfortable possibility that we’re now drifting into stagflation territory.

The Fed remains silent for now, but the market has started to speak. Dollar demand failed to show up at month-end, and the move to fade the greenback is gaining traction across desks. Positioning has shifted in favour of liquid alternatives the euro, yen and pound all look increasingly attractive, especially with their domestic outlooks looking relatively more stable.

On the corporate side, the tech-heavy optimism that once helped hold up equities is beginning to fray. Super Micro’s earnings miss didn’t help, and concerns are now building over how U.S. chip exports might be hit by escalating controls. With Microsoft, Meta, Amazon and Apple all reporting this week, there’s a real possibility that sentiment could swing quickly if results disappoint. And yet, equities haven’t cracked possibly because we’re now past the peak of macro uncertainty for Q1. Still, in FX, the dollar is no longer feeling like the haven it used to be. The repricing we’re seeing isn’t just about interest rate expectations anymore it’s about a broader loss of confidence in the U.S. growth story.

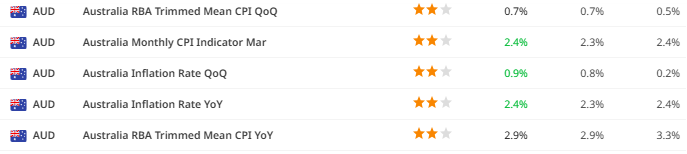

Looking across the Pacific, the Australian dollar had a moment of strength following this morning’s CPI release, which came in a touch firmer than expected. The rebound was largely driven by food and energy categories, in part due to the expiry of certain government subsidies. But despite the headline beat, the broader picture remains unchanged. Inflation is still within the RBA’s target band, and core measures continue to show signs of easing.

Some of the hawkish pricing in local rates has been unwound, but not completely and that might be a stretch. Goldman Sachs is sticking with their call that the RBA will resume cutting in May, with more easing to follow in the months ahead. The labour market is still tight, but it’s not overheating, and the inflation pulse simply isn’t strong enough to warrant a shift in tone. Given this, the Aussie’s recent strength feels more tactical than structural especially when risk sentiment is still fragile and global equities are mixed.

Meanwhile, China is back in focus after the latest round of PMI data showed a clear loss of momentum in the manufacturing sector. Both official and Caixin surveys dropped more than expected, with new export orders taking a particularly hard hit. That subcomponent tends to lead actual export volumes by a few months, which means China’s trade performance could deteriorate further into Q2.

Despite this, the Chinese yuan reversed initial losses, and it wasn’t just about technical flows. Beijing surprised markets by signalling it would exempt a list of U.S. goods from its 125% retaliatory tariffs. The so-called “whitelist” reportedly includes items like pharmaceuticals, aircraft engines, and semiconductors all of which are critical to China’s economy. This move suggests a more calculated approach from Beijing: standing firm on rhetoric while quietly carving out space for economic pragmatism.

There’s also a broader financial shift underway, with China’s sovereign wealth fund reportedly pulling back from U.S. private equity exposure. That’s more symbolic than systemic, but it fits into the broader trend of strategic decoupling. For now, soft CNY fixings continue, but the currency remains relatively stable even with the risks stacking up.

In short, we’re heading into May with markets that are re-evaluating old assumptions. The dollar is no longer a one-way bet, the Aussie looks overbought on shaky ground, and the yuan is being quietly supported by policy finesse. This is not a market for bold directional trades it’s one that rewards nuance, patience, and an eye on shifting fundamentals.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.