just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The European Central Bank may have just executed another rate cut but make no mistake this was not your typical dovish pivot. If anything, the tone from Christine Lagarde and the Governing Council was one of careful restraint, perhaps even quiet resistance. Yes, the deposit rate was trimmed by 25bp to 2.00%, but what followed sent a louder message: the ECB believes it’s nearing the end of its easing cycle, not beginning a new one.

This latest move brings the policy rate squarely to the mid-point of the ECB’s own “neutral” range (1.75%–2.25%) as published earlier this year. That’s no coincidence. The central bank has now positioned itself with enough policy ammunition to pause, assess, and importantly push back against overly dovish market expectations. And that’s exactly what Lagarde did.

Lagarde’s press conference was a balancing act. The ECB unveiled a set of downgraded inflation projections, with headline HICP expected to fall to 2.0% in 2025 (down from 2.3%) and to a low of 1.6% in 2026. These adjustments alone might have fuelled expectations of a longer easing cycle, but Lagarde made a point to attribute the fall in inflation to two main factors: lower energy prices and a stronger euro.

By calling these revisions “mechanical,” she was sending a message: this isn’t a sign that demand is collapsing or that core inflation is vanishing. In fact, core HICP was slightly revised up to 2.4% for 2025, suggesting underlying pressures are still present particularly in wage growth and services. That’s a key point. The disinflation process is real, but it’s not purely a monetary story.

On growth, the ECB’s tone was cautious but not gloomy. GDP expectations for 2025 hold at 0.9%, and 2026 was revised slightly down to 1.1%, mainly due to carryover effects from tariffs and fading momentum after a solid first half of the year. But even here, the ECB remains optimistic that increased government spending especially in defence and infrastructure could support resilience into 2027 and beyond.

Why Lagarde’s Messaging Matters

Lagarde is walking a tightrope between acknowledging progress on inflation and avoiding a market overreaction that might unwind the ECB’s work prematurely. The last thing the ECB wants is a surge in rate cut bets that pushes financial conditions too loose, undermining its fight against lingering core price pressures. Her insistence that the easing cycle is “well-positioned” and that decisions remain “data-dependent” reinforces the ECB’s desire to control the narrative.

Behind this language is also a deeper concern: global risks. The ECB’s scenario analysis explicitly warns that if EU-US trade tensions escalate something increasingly likely given the political calendar in both regions both growth and inflation could undershoot forecasts. Conversely, if trade negotiations manage to avoid drama, we could see modest upside.

It’s telling that Lagarde didn’t sound especially hopeful about a “benign” trade resolution. With the U.S. heading into elections and the EU facing its own internal political reshuffling, the odds of messy, drawn-out talks are rising. That geopolitical risk acts as a wildcard for future ECB moves and provides some justification for keeping optionality open, including the possibility of a surprise cut at the July meeting, if conditions deteriorate sharply.

But as of now, markets are aligned with the ECB’s implied message: don’t expect back-to-back cuts. A more likely path is a quarterly pace of reductions, skipping July and reconvening with fresh data and a better read on trade by the September 11 meeting. MUFG still sees a terminal rate of 1.50% by year-end, but even that feels more conditional than before. The bar for further easing has been raised.

FX Market Response: EUR Repricing

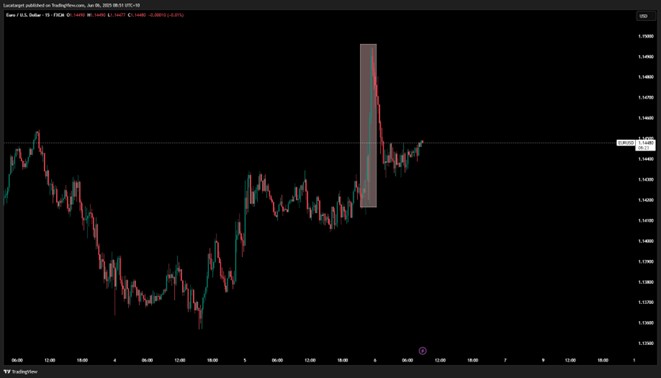

Markets wasted no time absorbing this shift. EUR/USD quickly pushed toward the 1.1500 handle, driven by the hawkish tone and upward revision in the short end of the eurozone yield curve. The 2-year yield rose by 5bps, reflecting a broad repricing of ECB easing expectations.

If the Fed ends up cutting sooner than anticipated particularly if this week’s NFP print comes in weak the euro could gain even more ground. The key resistance at 1.1573 (the April high) is now in play. Beyond that, we could see momentum build toward 1.20 if the ECB stands pat while the Fed pivots.

Also worth noting: Germany’s proposed €46 billion corporate tax relief package could reinforce the euro’s macro foundation. If passed, this fiscal boost would not only support growth but also reduce the pressure on the ECB to do more. That, combined with rising eurozone government investment, particularly in infrastructure and military capacity, suggests we’re entering a phase where fiscal and monetary policy start pulling in opposite directions.

Lagarde didn’t just deliver a rate cut she delivered a message of control. This was about shaping expectations and anchoring the ECB’s credibility in an increasingly volatile global backdrop. The central bank is threading the needle: easing just enough to acknowledge disinflation, but not so much as to unleash market exuberance or weaken the euro’s recent strength.

We are likely closer to the end of this easing cycle than many anticipated. Unless inflation stalls again or geopolitical risks flare up in an ugly way, Lagarde may have succeeded in buying the ECB enough space to watch and wait.

For EUR bulls, the macro setup remains constructive. And for FX traders, the focus now shifts firmly to the U.S. with every Fed comment and piece of incoming data holding the potential to tip EUR/USD through critical resistance.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.