just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

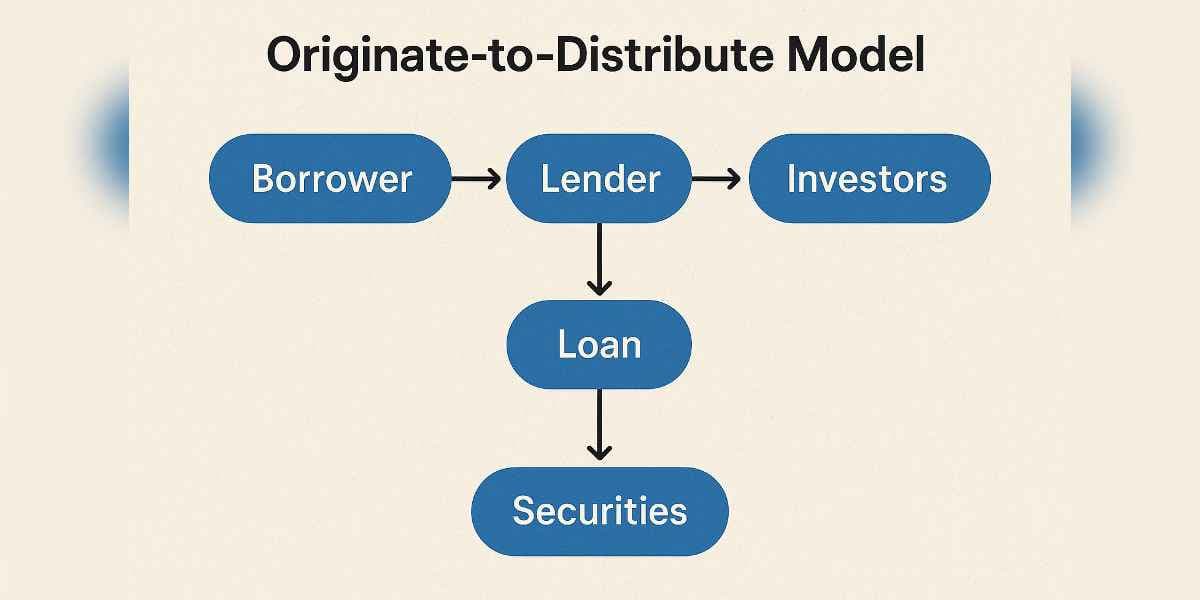

The OTD model is a modern banking approach where banks originate loans but quickly sell them to investors or package them into securities (like ABS or CDOs), rather than holding them until maturity. This model has expanded from mortgages to credit cards, auto loans, student loans, and corporate lending.

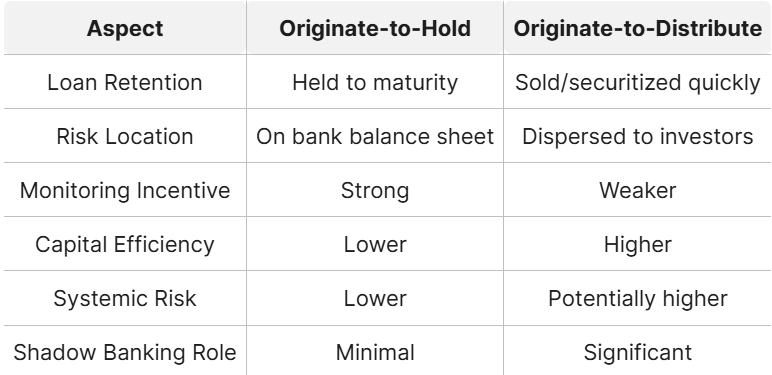

Banks benefit from diversified funding by accessing a broader pool of investors beyond traditional depositors. This expansion allows them to tap into various capital markets and investor types, enhancing their financial flexibility and resilience.

The dispersion of credit risk across many market participants reduces the concentration of risk within any single institution. By distributing loans to a wide range of investors, banks help mitigate systemic vulnerabilities that could arise from localized credit exposures.

Selling loans also improves capital efficiency for banks. By offloading loans from their balance sheets, banks free up regulatory capital, which can then be redeployed to originate additional loans, supporting greater lending activity and economic growth.

Additionally, banks generate fee income through multiple channels in this model. They earn fees from originating loans, selling them to investors, and providing ongoing servicing such as collecting payments and managing the underlying assets, creating diversified revenue streams.

As banks increasingly adopt the originate-to-distribute (OTD) model, one significant consequence has been the weakening of lending standards. Since banks no longer retain the majority of the risk associated with the loans they originate, their incentive to thoroughly screen and monitor borrowers diminishes. This shift can lead to a greater prevalence of lower-quality loans entering the financial system, as originators may prioritize loan volume over credit quality, knowing that much of the risk will be transferred to third-party investors.

The growth of shadow banking is another critical development linked to the OTD model. Nonbank entities such as collateralized loan obligations (CLOs) and investment managers now hold substantial portions of credit risk that was once concentrated within regulated banks. These nonbank financial intermediaries often operate with less regulatory oversight, which can obscure the true location and magnitude of risk within the broader financial system. This shift has contributed to the expansion of the so-called "shadow banking" sector, raising concerns about financial stability and transparency.

Liquidity risks have also become more pronounced under the OTD model. Banks that rely heavily on securitization markets for funding are vulnerable to sudden drops in investor demand for structured products. This vulnerability was starkly demonstrated during the 2007–2008 financial crisis, when the market for asset-backed securities seized up, leaving banks unable to sell or refinance their loans. The resulting liquidity squeeze forced some banks to seek emergency funding or absorb unexpected losses, highlighting the fragility of this funding model during periods of market stress.

Finally, the potential for credit crunches is an inherent risk in the OTD framework. If the secondary market for loans and structured products freezes, banks may be compelled to retain loans they had intended to distribute. This scenario can strain bank balance sheets, reduce their lending capacity, and ultimately restrict the flow of credit to the real economy. Such disruptions can amplify economic downturns, as seen in past crises, underscoring the importance of robust risk management and regulatory oversight in an environment increasingly shaped by the originate-to-distribute model.

In recent years, banks have significantly reduced the proportion of term loans they retain on their balance sheets. Instead of holding these loans until maturity, banks now sell or securitize the majority of them, transferring much of the associated credit risk to nonbank investors such as collateralized loan obligations (CLOs), investment funds, and other institutional players. This shift has fundamentally altered the risk landscape of the financial system, as nonbank entities now play a much larger role in absorbing and managing credit risk.

The distribution of loans by banks is increasingly purpose-driven. Banks are more likely to offload loans that are considered riskier, such as those issued for mergers and acquisitions (M&A), into the secondary market. These loans typically carry higher risk profiles and are more attractive for securitization and sale. In contrast, banks tend to retain a greater share of loans used for capital expenditures, which are generally viewed as less risky and more stable. This selective approach reflects both regulatory considerations and the banks’ own risk management strategies, as well as investor appetite for higher-yielding, riskier assets.

Despite the lessons from past financial crises, the originate-to-distribute (OTD) model remains a central feature of large-scale lending, especially in the United States and Europe. The model’s efficiency in freeing up bank capital and supporting high volumes of lending has ensured its continued use. However, the growing reliance on nonbank investors and the evolving complexity of structured finance products continue to pose challenges for financial stability, making robust risk management and regulatory oversight more important than ever.

Samantha Lee, Chief Credit Strategist at GlobalBank:

“The OTD model has proven resilient, but recent market volatility highlights the need for banks to maintain strong underwriting standards even when they don’t hold the loans long-term.”

Dr. Rajiv Menon, Financial Stability Advisor, ECB:

“Supervisors are increasingly focused on transparency and stress-testing in the securitization market. The lessons of 2008 are clear: risk must be understood and managed, not just transferred.”

Elena Garcia, CEO of FinTech Analytics:“

Advanced analytics and AI are helping banks better assess borrower risk, even in an OTD framework. However, technology is no substitute for prudent risk culture.”

Michael O’Connor, Senior Partner, Capital Markets Advisory:

“Shadow banking continues to grow, and while it adds flexibility to the system, it also creates blind spots for regulators. The OTD model is at the heart of this evolution.”

Lisa Tan, Head of Fixed Income Research, EuroInvest:

“Periods of market stress still expose the fragility of structured products. Investors are demanding more transparency and simpler structures, which is a healthy development.”

The OTD model remains a pillar of modern banking, enabling greater lending and risk sharing. However, recent events and expert commentary underscore the ongoing need for robust risk management, transparency, and regulatory vigilance—especially as new technologies and market participants reshape the financial landscape.

We're the largest marketplace to connect with brokers, Fintech companies & digital asset firms. Want to partner? Let's get in touch.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.