just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

Every week, I try to make sense of the noise in the market, and this one is no different. After a strong July for the US dollar, I’m closely monitoring whether that strength has legs, or if we’re starting to see cracks form beneath the surface.

The dollar (DXY) surged over 3% in July, its biggest monthly gain since April 2022. That strength came on the back of trade optimism, new tariff deals, and a resilient U.S. economy. But here’s the thing: markets may be overly optimistic about the economic impact of these tariffs.

As of the end of July, the average effective U.S. tariff rate reached 18.4%, a level we haven’t seen since the 1930s.

The real question now is how long that strength can last, especially as we begin to assess the economic fallout. That’s what I’ll be watching this week.

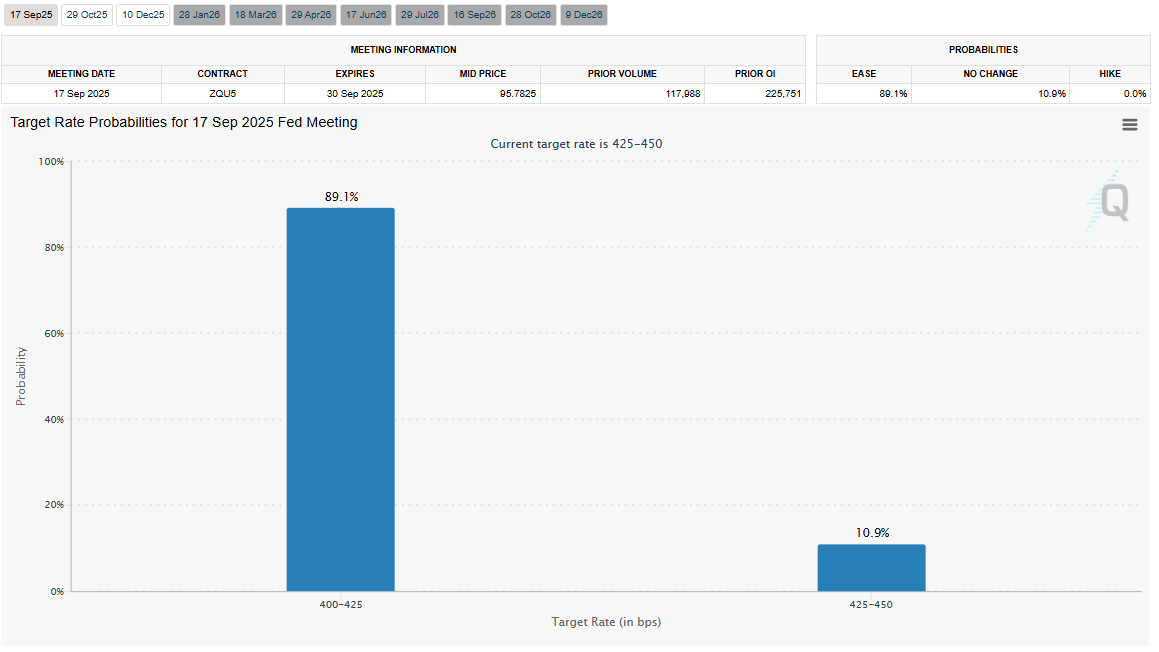

There’s no FOMC meeting this month, but don’t think the Fed is out of the picture. All eyes are on the Jackson Hole Symposium (22–24 August), where Powell is expected to give an updated view on policy.

With last week’s non-farm payrolls coming in far weaker than expected, the probability of a September rate cut has increased.

If we get more softness in labor data and signs of tariff-induced inflation, that could be the turning point. Until then, expect the Fed to hold the line.

This week is heavy on G10 central bank decisions:

Bank of England (Aug 7) – A rate cut is almost fully priced in. Inflation is sticky, but growth is soft. Expect internal division at the MPC.

Reserve Bank of Australia (Aug 12 next Tuesday) – After a weak June CPI print, I’m leaning toward a 25bp cut. The RBA seems set to proceed gradually.

Norges Bank and RBNZ (Aug 14 & 20) – Both are likely to hold, though the RBNZ has around an 80% chance of cutting. I’ll be watching their tone closely.

The key theme across all these decisions? Caution. Central banks are moving, but no one wants to go too far too fast.

EUR/USD: After falling from 1.17 to 1.14 in July, I’m now watching for a base around the 1.14 handle. While the EU-US trade deal brought some EUR selling, I think the worst of the positioning flush is behind us. If US data weakens, this pair could push back toward 1.17 by month-end.

USD/JPY: The yen sold off sharply last month, breaking through 150. That weakness has been driven more by BoJ caution and Japanese political uncertainty than by US strength. If the BoJ continues dragging its feet on tightening, I wouldn’t be surprised to see 152 tested before we see any retracement.

AUD/USD: This pair remains sensitive to global growth sentiment. With the RBA likely to cut but stay cautious, and the US-China trade narrative stabilizing, I’m watching for a potential bounce above 0.65 if risk sentiment stays firm.

USD/CAD: The Canadian dollar has shown resilience, supported by strong jobs data. But weaker PMI numbers and higher inflation complicate the BoC’s path. I see limited upside for the loonie unless we get a meaningful risk-on wave.

China’s July Politburo meeting didn’t bring the stimulus fireworks many were hoping for. Still, with 5.3% GDP growth in H1 and new childcare subsidies and social programs on the table, I think Beijing is opting for targeted support over broad stimulus.

I’m still cautious on CNY and expect more depreciation pressure unless we see clearer policy shifts in October’s five-year plan announcement.

In LatAm, the Brazilian real is catching my attention again. With a spot rate of 5.53 and MUFG forecasting a gradual move toward 5.35, I think BRL still has room to recover, especially if commodities stabilize and political noise stays contained.

We’re in a market driven more by perception than fundamentals right now. The trade deals look good on paper, but the real impact, especially on inflation and global demand, has yet to be felt. If the data starts turning, so will the trades.

Until then, I’m staying nimble, focusing on data surprises, and watching rate differentials more than headlines. As always, it’s not just about what the central banks say, it’s about what the market hears.

Let’s see how the week plays out.

1. What is driving the US dollar strength in August 2025?

The US dollar has surged due to stronger-than-expected economic resilience, optimism over recent trade deals, and delayed expectations for Fed rate cuts. However, with weaker job data emerging, this trend may soon reverse if the Fed signals easing.

2. Why is EUR/USD under pressure despite a US-EU trade deal?

Although the deal reduced tariff risks, excessive long positioning and strong US economic data led to a correction in EUR/USD. The pair could recover if the Fed leans dovish and US data weakens further.

3. What central bank decisions should traders watch this week?

Key rate decisions from the Bank of England (Aug 7) and Reserve Bank of Australia (Aug 12) are in focus. Both are expected to cut, but forward guidance and economic projections will likely drive the currencies more than the cut itself.

4. Is the Australian dollar expected to strengthen or weaken?

AUD may gradually appreciate if risk sentiment remains stable and the RBA maintains a cautious tone. A potential US-China trade resolution would also support AUD in the medium term.

5. How does Jackson Hole impact forex trading?

The Jackson Hole Symposium (Aug 22–24) is closely watched for Fed Chair Powell’s policy guidance. Any shift toward dovish language or mention of labor market softness could significantly influence USD pairs.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.