just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

In a dramatic pivot that has jolted currency markets, the United States and China have agreed to a sweeping rollback of mutual tariffs, marking what may be the most significant thaw in trade tensions since the Trump 1.0 era. For traders and economists alike, the deal announced in Geneva went far beyond expectations. Where many had braced for a moderate reduction to 60%, in line with earlier campaign signals, the reset to a 10% baseline stunned the market.

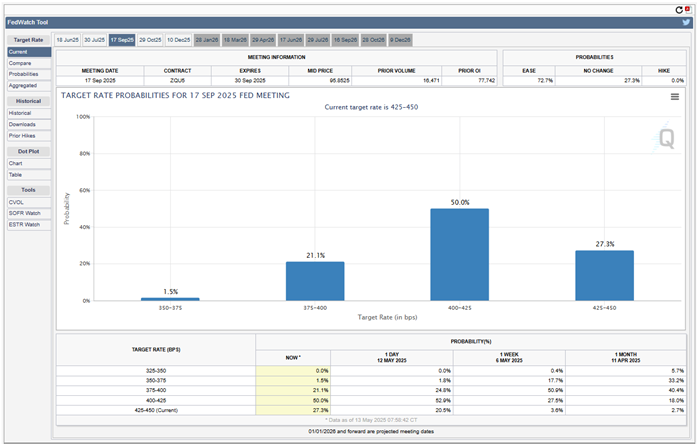

The dollar, which had been on the back foot since March as tariffs escalated, has clawed back around 3.5% on a DXY basis. Yet the bigger picture is less about relief and more about recalibration. The tariffs previously raised on Chinese goods had triggered a reciprocal retaliation and sent the dollar tumbling by roughly 9% from March to April. This rollback combined with the Fed’s current stance has pushed expectations of a July rate cut off the table. A week ago, the market was pricing in a 25bp cut with confidence. Now? Barely a 10bp move is anticipated.

Chair Powell’s previous hesitation to adjust policy amid trade uncertainty suddenly feels outdated. The Fed might now find itself forced to defend its current rate path longer than the market had hoped. The 90-day window before the next review of tariffs expires in August, just after the July FOMC, could still reopen volatility. But for now, US economic sentiment is buoyed. Boeing just got the green light to resume deliveries to Chinese airlines, and equity markets especially the tech-heavy Nasdaq are roaring in response.

Still, deeper questions remain. Trump has framed this as a “complete opening” of the Chinese economy, claiming it will narrow the US trade deficit and rebalance global trade. History, however, suggests caution. Both China and Germany have faced similar Western demands for decades with limited structural change. The risk is that Trump is overestimating what he has secured, and that tariffs could return with a vengeance, particularly with US elections drawing closer.

The British pound was among the top G10 performers this week a notable feat, considering it was up against a surging dollar. A fresh bilateral trade agreement with the US has helped reinforce the pound’s credibility in an increasingly fragile global trade framework.

More quietly but just as significantly, the Bank of England’s internal debate is growing more intense. Last week’s policy meeting nearly saw a rate cut, with Deputy Governor Clare Lombardelli and MPC member Megan Greene both leaning toward easing. Now, with the US-China détente in full view, their decisions appear finely balanced in retrospect. Greene has a known hawkish tilt, but Lombardelli’s position signals the Bank may be edging toward a more cautious outlook not rushing to cut further without clear signs of economic deterioration.

Today’s UK labour market data only sharpened that narrative. While headline wage growth slightly outpaced expectations, the PAYE job data continues to show weakness. April saw a 33,000 drop in payroll employment the fifth fall in six months underscoring a softening trend. Wage data excluding bonuses softened too, supporting the idea that the UK labour market is cooling, albeit unevenly. In short, while the BoE may move to ease further, it will likely do so with a measured hand. Inflationary pressures remain sticky, and wage growth is still too hot for comfort when viewed through the lens of a 2% inflation target.

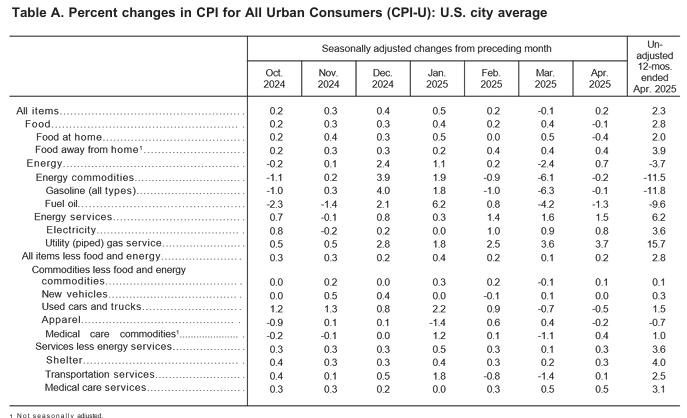

Just days after Washington and Beijing agreed to roll back nearly all trade war-era tariffs, U.S. inflation data added another twist to the macroeconomic landscape. April’s CPI print came in softer than feared, with headline inflation ticking up just 0.2% on a seasonally adjusted basis, following a dip of 0.1% in March. On an annual basis, inflation eased to 2.3% the lowest 12-month increase since early 2021. Markets initially priced this as a dovish signal, but with trade risks receding rapidly, the dollar is instead gaining altitude, buoyed by repricing in rates and risk sentiment.

Shelter costs were again the dominant driver of inflation, rising 0.3% month-on-month and contributing more than half of April’s increase. Energy prices also rebounded modestly, up 0.7% on the month, with electricity and natural gas making notable gains, even as gasoline prices eased. Food inflation offered mixed signals: the index for food at home declined by 0.4%, while dining out continued to show sticky inflation, up 0.4%. Egg prices plunged nearly 13%, reflecting continued volatility in animal product pricing.

Core inflation (CPI excluding food and energy) also rose 0.2% in April not exactly alarming, but just enough to cast doubt on the likelihood of a near-term Fed pivot. Before the CPI release, a July cut was already looking less certain in the wake of the tariff détente. Now it’s almost off the table.

The dollar is enjoying a short-term boost from the easing of trade tensions, but structural risks remain embedded in the global economy. The UK finds itself in a peculiar, sweet spot: benefiting from global shifts while facing mounting domestic challenges. Central banks on both sides of the Atlantic are not yet ready to pivot decisively, but they’re inching toward divergence. Expect volatility to return by August as the 90-day tariff review window closes and with US elections heating up, politics may once again overpower policy.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.

Want to master the markets? A winning trading mindset beats a perfect strategy. Learn how emotional discipline helps you conquer fear and avoid heavy losses.