just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The latest market developments have been largely dictated by geopolitical tensions and trade policy shifts, creating a backdrop of heightened uncertainty for major currency pairs. The US dollar has shown resilience, gaining around 0.5% from recent lows, as concerns over trade war escalation momentarily eased following a partial policy reversal by the US administration. President Trump’s decision to halt the doubling of tariffs on Canadian steel and aluminium provided temporary relief; however, the broader 25% tariffs on these goods remain in place. With key tariff implementations still looming, including additional measures set for April 2nd, the risk of further escalation remains high.

In response, the European Union has moved swiftly, imposing tariffs on $26 billion worth of US exports, with further measures scheduled for mid-April. These moves, coupled with increased tariffs covering 289 downstream products valued at $150 billion, signal a prolonged and intensified trade dispute. Notably, the automotive sector, particularly the supply chains for cars, trucks, and heavy machinery, stands to bear the brunt of these policies. Canada and Mexico remain among the most affected economies, with the broader uncertainty placing additional pressure on both currencies. Despite this, positioning in the Canadian dollar suggests that significant short interest among leveraged funds may be providing a temporary cushion against deeper depreciation.

Meanwhile, the euro’s performance remains closely tied to geopolitical factors, particularly developments in Ukraine. A potential ceasefire agreement, backed by US-led negotiations, could lead to a temporary de-escalation in the region. While the direct economic impact remains uncertain, a reduction in geopolitical risk could offer some support to the euro. Energy markets, however, remain relatively unmoved, with natural gas prices holding steady and crude oil showing only modest gains following revisions by the IEA, which lowered its forecast for excess crude supply.

In the UK, the focus has shifted to securing exemptions from US-imposed steel tariffs. The government is actively negotiating a carve-out, leveraging the argument that UK-US trade is largely balanced. However, success is far from guaranteed. While UK steel exports to the US have declined since the 2018 tariff measures, the sector remains a focal point for policymakers. Failure to secure an exemption could weigh on the British pound, particularly given current market expectations that some form of relief will be granted.

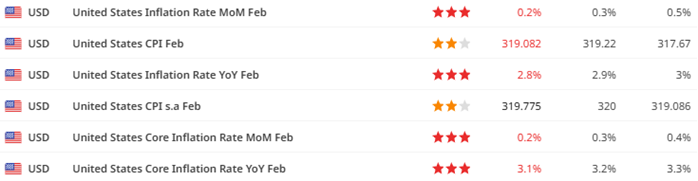

Looking ahead, the dollar’s trajectory will likely hinge on incoming economic data, particularly inflation metrics. The latest US CPI release came in lower than expected, with core inflation slowing to 3.2% year-over-year versus forecasts of 3.3%. This marks a continued downward trend in inflation, reinforcing the market’s expectations that the Federal Reserve could shift toward a more dovish stance. While the Fed has maintained a cautious approach, further evidence of easing price pressures could solidify bets on rate cuts later in the year. As a result, the USD has seen some softening, with investors recalibrating their expectations for future monetary policy adjustments. Meanwhile, the Bank of Canada is widely expected to implement a 25bp rate cut, reflecting growing concerns over economic momentum. With market sentiment heavily driven by shifting policy expectations and geopolitical risks, volatility is likely to remain elevated in the near term.

Overall, while the USD remains supported by relative economic resilience, the broader uncertainty tied to trade tensions and global policy shifts suggests that caution remains warranted. Market participants should remain vigilant as April’s tariff deadlines approach, with potential retaliatory actions set to further influence currency markets.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.