just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The past week brought a fresh wave of volatility to global markets as the U.S. reignited trade tensions with new tariffs, prompting swift retaliation from China and the European Union. However, in a dramatic turn of events, President Trump reversed course on April 9, announcing a 90-day suspension of most of the newly announced tariffs—excluding those on China, which were instead increased to 125%.

This unexpected policy pivot triggered a powerful relief rally in global equities, with Chinese and U.S. stocks rebounding sharply after days of heavy selling. While the market cheered the pause, the tariff hike on Chinese goods signals the trade conflict is far from resolved.

China wasted no time responding to the initial U.S. tariff barrage, imposing retaliatory duties on approximately $80 billion worth of American goods—a broad set of products designed to apply maximum pressure.

But following Trump’s partial retreat on tariffs, sentiment across Chinese equity markets flipped. The Shanghai Composite and Hang Seng Index both surged on April 9, joining the global rebound. Investors took the tariff pause as a potential signal that negotiation channels could reopen, even though China remains the primary target of increased U.S. duties.

The European Union reactivated previously suspended tariffs in early April, escalating the transatlantic trade dispute. As of April 9, retaliation affects around $25 billion worth of U.S. goods.

The EU’s move signals a clear break from its wait-and-see posture, especially following the U.S. decision to resume tariffs initially paused under previous agreements.

Retaliation Totals (As of April 9, 2025)

| Bloc/Country | Value of Tariffs | Key U.S. Exports Targeted | Tariff Range |

|---|---|---|---|

| China | $80 Billion | Agri, Autos, Tech, Industrial Goods | 15%–30% |

| European Union | $25 Billion | Metals, Food & Drink, Tech Goods | 10%–50% |

| Total | $105 Billion | — | — |

Andy Sieg, Citi Head of Wealth: “Don’t buy the dip! Don’t invest in risk assets—yet.”

In a firm caution to investors, Andy Sieg, Head of Wealth at Citi, urged restraint amid a landscape still shaped by global volatility, geopolitical headwinds, and unresolved trade tensions.

Fed Watch: How Trade Wars Could Shift the Rate Path

The March 18–19, 2025 FOMC meeting revealed a Federal Reserve still walking a tightrope between containing inflation and maintaining financial stability. While the Fed held rates steady at 4.25%–4.50%, its subtle shift in policy tone—and especially the move to slow balance sheet reduction starting April—speaks volumes about its awareness of emerging downside risks.

Connecting the Dots: Fed Policy vs. Trade War Fallout

The Fed’s March moves—particularly slowing balance sheet tightening—have helped cushion April’s market volatility from trade wars. But if tariff retaliation spreads or starts showing up in real economic data, the pressure will mount for rate cuts in the second half of 2025.

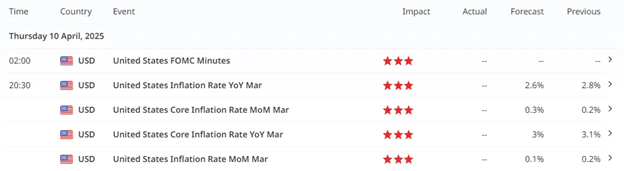

As markets head into Thursday’s U.S. session, focus is squarely on the March CPI release, due at 20:30 GMT, alongside the FOMC minutes earlier in the day.

Market Expectations:

If CPI matches or comes in below expectations, it gives the Fed breathing room. If it surprises to the upside—especially core—expect markets to reprice the rate path hawkishly.

4-Hour

As we await CPI for today, we are looking for the greenback to show its intent by:

Tactical Game Plan for Majors

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.