just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

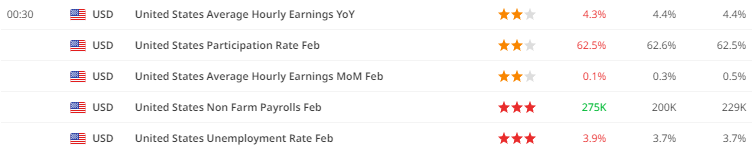

In the latest release on US February payrolls last Friday, the numbers paint a mixed picture of the labour market. Nonfarm payrolls surpassed expectations, surging by an impressive 275,000, well above the estimated 100,000 required to accommodate population growth. However, the sheen of this robust performance was dimmed by a substantial downward revision of 167,000 to the prior two months' payrolls.

USA NFP

Job gains in February were primarily attributed to sectors like private education & health (+85,000), leisure & hospitality (+58,000), and government (+52,000). Notably, private education & health and government roles, which tend to be less cyclical, collectively contributed to around half of the total payroll growth. Conversely, the manufacturing and wholesale trade sectors, sensitive to economic cycles and interest rates, experienced job losses during the month.

While payroll growth maintained its solidity, other indicators in the employment report suggest a potential softening of the labour market. The unemployment rate saw a 0.2 percentage point increase to 3.9%, marking its highest level in over two years. Despite the strong payroll growth, the unchanged participation rate at 62.5% and a 184,000 decline in the household survey measure of employment added a layer of complexity. The household measure, considering self-employed individuals, farm workers, and business dynamics, introduces uncertainty about the true health of the labour market.

Average hourly earnings (AHE) rose by a modest 0.1% month-on-month in February, falling below expectations. AHE growth in the previous month (January) was also revised slightly downward to 0.5% from 0.6%. The Federal Reserve's preference for AHE to be within the 3-3.5% range was challenged, as year-on-year AHE growth eased to 4.3% in February.

For the Federal Reserve, the February employment report presents a mixed bag. While the welcomed correction in AHE was anticipated, the central bank closely monitors the Employment Cost Index and Atlanta Fed Wage Growth Tracker, both indicating a continued easing trend. The strong payroll growth may provide room for cautious optimism, influencing the Fed's stance on rate cuts.

In the bigger picture, the February employment report might not drastically alter the Fed's perspective, but there is a nuanced dovish undertone. Importantly, private surveys are signalling a softening in hiring intentions and an uptick in layoffs, factors that likely contributed to Fed Chair Powell's recent comments about being "not far" from considering rate cuts. The central bank, he noted, requires "a little bit more" data to gain confidence in inflation moving sustainably down to the 2% target.

Chart 1 illustrates the substantial rise of 275,000 in nonfarm payrolls for February, with revisions showing a solid three-month average payroll gain at 265,000 and a six-month average at 231,000, signalling resilience amid underlying uncertainties.

Insights Inspired by UniCredit: Credit to Their Analysis for Shaping Some Aspects of This TextTop of Form

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.

Want to master the markets? A winning trading mindset beats a perfect strategy. Learn how emotional discipline helps you conquer fear and avoid heavy losses.

Read our latest Gold price action forecast to see how a double top pattern triggered a massive XAU/USD selloff.

Wondering how the API weekly report impacts oil prices? Learn how U.S. crude stockpiles and voluntary surveys predict the official EIA report.

cTrader Mobile 5.9 introduces a dedicated charts tab, single-tap chart access, a draggable floating action panel and a new focus mode for positions and orders, following the platform's Best Mobile Trading App win at UF Awards Global 2026. Sergey Borisov of Spotware comments on the update.

BitPay B.V., the European arm of BitPay, has been authorised as a crypto-asset service provider under MiCA by the Dutch AFM, allowing it to offer regulated crypto and stablecoin payment services, cross-border payments, and consumer spending tools across the EU.

Spotex has appointed Joe Tuccio, previously Head of Digital Partnerships at Seabury Capital, as Head of Digital Assets. Tuccio brings 20 years of financial markets experience and will lead partnerships with liquidity providers and custodians as Spotex expands its institutional FX venue into digital assets.