just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

As we head into the third week of May, market participants are weighing a mix of bullish price action against stubborn economic risks. Next week’s US economic calendar is headlined by two pivotal updates: fresh housing data amid ongoing affordability concerns, and April’s inflation report—a release known for surprising markets.

While stocks, particularly the S&P 500, have powered through resistance levels in recent weeks, there’s a growing disconnect between market optimism and underlying fundamentals. This week’s data could be a wake-up call.

Let’s break it all down…

The upcoming housing report will provide the latest snapshot of a sector still struggling under the weight of high financing costs. With the 30-year mortgage rate lingering just below 7%, the average new mortgage taken out for home purchases—about $450,000—equates to monthly payments nearing $3,000. That’s simply unaffordable for most Americans.

This affordability squeeze explains why mortgage applications remain historically low, despite a modest bump in new purchase applications. More importantly, sentiment among builders is collapsing. The National Association of Home Builders (NAHB) index fell sharply in May, underscoring a gloomy outlook among those closest to the action. Builders are reacting not only to pricing pressure but also to buyer hesitation triggered by recent volatility across financial markets.

With the housing market showing little sign of revival, even marginally weaker data could reinforce a broader economic slowdown narrative.

April inflation data—especially on the services side—has historically been a market-mover. That’s because April often sees annual increases in service-sector costs like healthcare, travel, insurance, and other stickier inflation categories.

In both 2023 and 2024, April’s CPI report came in hotter than expected, causing notable reactions in rates and equities. This time, there’s cautious optimism that services inflation could come in cooler—below the Bank of England’s 5% forecast.

If that’s the case, it won’t necessarily trigger a rate cut at the Fed’s June meeting, but it would help solidify expectations for policy easing later in the summer, potentially in August. For rate-sensitive sectors like housing, a more dovish tilt could offer some badly needed relief.

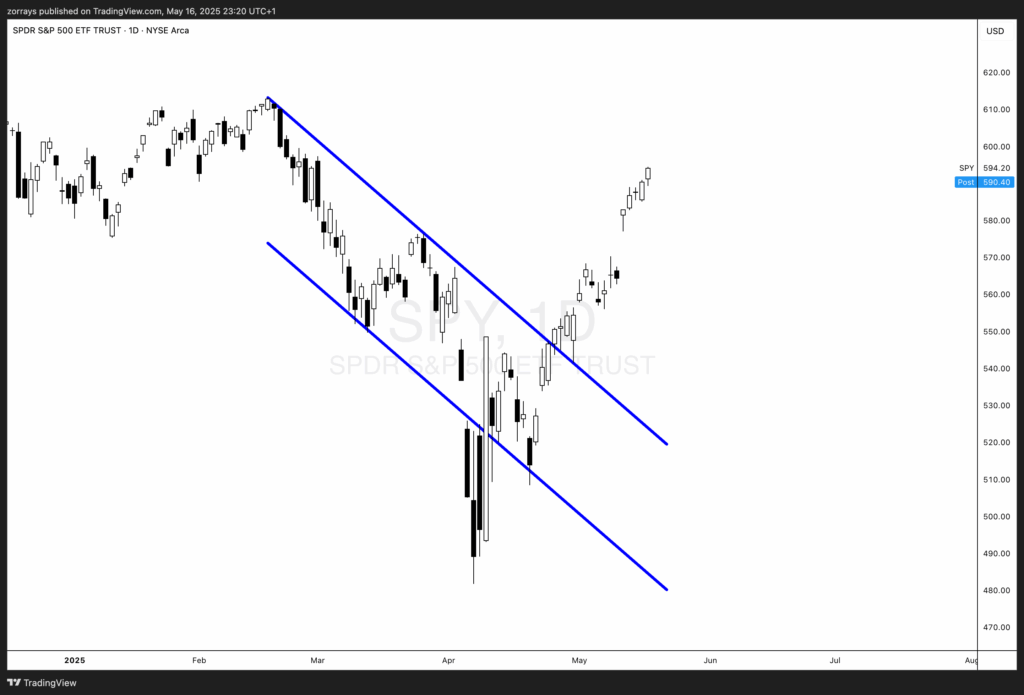

From a technical standpoint, the S&P 500’s recent performance has been stunning. After bottoming out in April, the index has broken out of a descending channel in dramatic fashion—posting one of its fastest rallies ever over such a short period.

Momentum remains strong, and short-term breadth indicators suggest little resistance up to all-time highs. But is this momentum sustainable?

Not everyone thinks so. And a look beneath the surface reveals that some market participants may be mispricing risk.

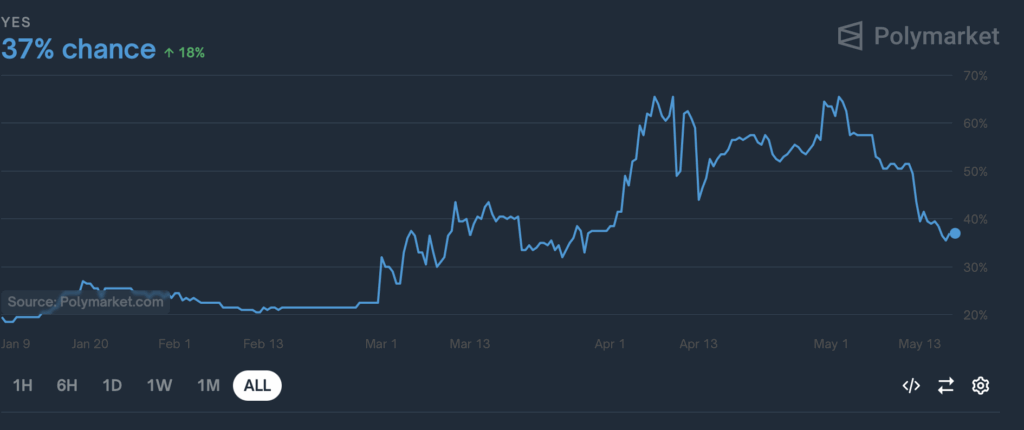

Source: Polymarket.com

While equity markets seem euphoric, prediction markets are still pricing in a 37% chance of a US recession before year-end. That number has dropped significantly since the recent 90-day pause on new tariffs, which initially spooked investors earlier this year.

However, it’s crucial to note that this pause is just that—a temporary deferral, not a resolution. The structural trade issues between the US and China remain unresolved, and any flare-up could reintroduce significant downside risks for growth.

In short, while the immediate threat has eased, the underlying fragility of the macro backdrop hasn’t gone away. The divergence between rising stock prices and sustained recession probabilities suggests either optimism is warranted—or investors are being lulled into a false sense of security.

Next week’s data on housing and inflation will offer timely insights into the real economy—beyond the headlines of new stock market highs. The S&P 500’s record-breaking rally may seem unstoppable, but with affordability collapsing in the housing sector and recession risks still elevated, caution is warranted.

For traders, investors, and policymakers alike, this week presents a reality check: the economy and the market may not be singing the same tune. Stay vigilant, stay informed.

Alchemy Markets is a multi-asset brokerage providing retail traders with the same elite trading conditions, tools, and transparency typically reserved for institutions.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.