just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

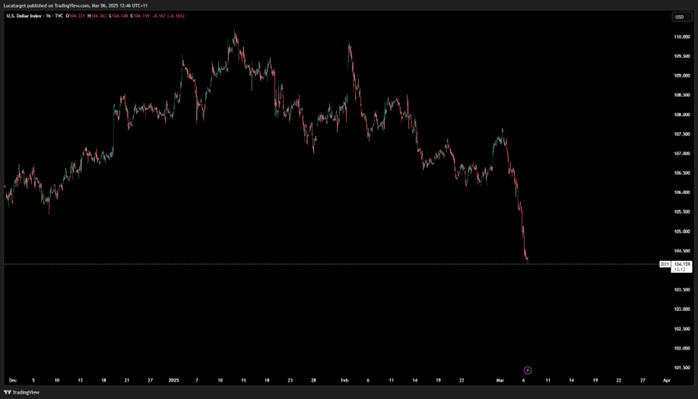

The recent depreciation of the US dollar has raised questions about whether the currency is at a turning point. While I have stepped away from predicting EUR/USD dropping below parity, the broader outlook still leans toward renewed dollar strength. The key driver remains the sharp move in US-Eurozone yield spreads, which has provided short-term resistance for the dollar. The recent 50-basis-point drop in the US-EZ 10-year spread—the most significant since the initial COVID-19 shock in 2020—has bolstered the euro’s rally. However, this momentum may not be sustainable.

The euro has been the best-performing G10 currency recently, supported by a surge in yield spreads and political developments in Germany. A recent deal between Friedrich Merz’s CDU-CSU and the SPD aims to create off-balance-sheet funds to boost defence and infrastructure spending, potentially unlocking further economic momentum. However, the Greens' stance remains a crucial factor in whether this initiative will pass before the current parliamentary session expires on March 25.

Despite this, the euro’s upside remains limited by trade tensions. Former US President Donald Trump, in a recent address, explicitly targeted the EU for additional tariffs, alongside China, Brazil, India, Mexico, and Canada. Given Trump’s history of erratic trade policies, uncertainty remains high. Reports suggest a potential tariff rollback for Canada and Mexico, but Europe remains firmly in the crosshairs, which could weigh on EUR/USD.

The Japanese yen, which had been benefiting from falling US yields and risk-off sentiment, faced a setback as front-end US rates rebounded. Despite this, Washington’s growing discomfort with currency misalignment adds another layer of complexity. Trump has openly accused Japan and China of devaluing their currencies and has suggested tariffs as a countermeasure. If this rhetoric intensifies, it could discourage speculative yen selling and even encourage yen buying.

Japanese authorities are also voicing concerns over excessive yen weakness. Vice Finance Minister Atsushi Mimura warned that a weak yen could hinder real wage growth, reinforcing the view that the government prefers a stronger currency. With Japan’s previous interventions totalling JPY 24.55 trillion (USD 160 billion) in 2022 and 2024, any further weakness may trigger official action.

Looking ahead, the yen’s trajectory will largely depend on US front-end rate movements. If US yields continue to retreat and Trump’s stance on currency intervention gains traction, USD/JPY could shift downward. However, in the short term, the pair's recent rebound suggests a period of consolidation before any decisive move lower.

Traders should monitor several key economic releases and events that could drive FX volatility:

The FX landscape remains highly fluid, with shifting yield spreads, political uncertainty, and trade tensions driving market moves. While the euro has capitalized on recent USD weakness, trade risks and political hurdles could limit further gains. The yen’s outlook remains tied to Washington’s stance on currency policy and front-end US rates. In the coming weeks, expect heightened volatility as traders react to evolving macroeconomic and geopolitical developments.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

cBridge, by Spotware, has launched Markout Report, a risk intelligence module that lets brokers detect toxic flow, rank accounts by financial impact and act before losses accumulate, all within the bridge.

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.