just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The US dollar is finding some short-term pressure as global market sentiment worsen following a temporary policy shift from the Trump administration. However, beneath the surface, fresh inflation data and deepening US-China tensions are complicating the outlook for the greenback, keeping markets firmly on edge.

One of the biggest developments driving the market rebound this week has been President Trump’s decision to pause the implementation of elevated “reciprocal tariff” rates for 90 days a move aimed at de-escalating tensions with key US trade partners. This exemption applies to most countries but notably excludes China, which now faces a sharply increased tariff rate of 125% on targeted goods. For others, including Canada and Mexico, a reduced 10% tariff will apply down from the threatened 60%.

The weighted average US import tariff now stands around 25%, but that number drops closer to 13–14% if China is excluded. While this move has injected a degree of relief into markets especially for high beta FX like AUD and NZD it’s also underscored Washington’s increasingly hawkish posture toward Beijing.

Markets initially interpreted the announcement as a diplomatic olive branch, with equities staging an aggressive relief rally. The S&P 500 surged by 9.5%, and the Nasdaq jumped over 12%, reversing much of the damage caused by the announcement of tariffs earlier this month. Treasury yields dropped sharply in tandem 10-year and 30-year yields fell by 20–30bps as bond markets recovered from recent panic-driven selling linked to forced liquidations and volatility in basis trades.

According to US Treasury Secretary Scott Bessent, the White House now hopes to "approach China as a group" after negotiating terms with other allies a comment that reinforces the idea of a multilateral pushback against Chinese trade practices. But China isn’t backing down either. In retaliation, Beijing raised its own tariffs on US imports to 84%, showing that the tit-for-tat spiral remains very much alive.

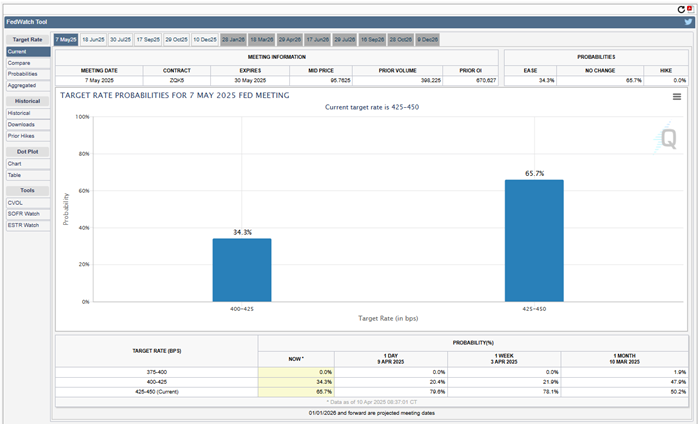

Against this backdrop, Federal Reserve policy expectations have adjusted sharply. Before the tariff pause, market pricing had tilted toward as much as 125bps of Fed rate cuts by year-end, driven by concerns about financial instability and stagflation. Since Trump’s reversal, however, that figure has compressed to around 75bps, reflecting some stabilization.

The Fed’s March FOMC minutes, released last night, offered limited insight given the rapid policy shifts since the meeting. The key takeaway remains that the Fed is not in a rush to restart aggressive rate cuts. That said, recent instability in bond markets and the political pressure from the administration could still tilt the balance toward more intervention if volatility re-emerges.

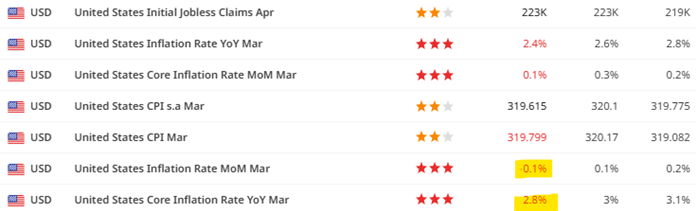

Adding another layer of complexity to the Fed’s calculus was yesterday’s US CPI print, which delivered a notable downside surprise. Headline CPI unexpectedly declined by 0.1% MoM in March, marking the first monthly drop since mid-2022. On a year-on-year basis, inflation slowed to 2.4%, well below the consensus estimate of 2.6% and down from 2.8% in February.

Core CPI which excludes food and energy also came in softer, rising just 0.1% MoM and 2.8% YoY, versus market expectations of 0.3% and 3.0%, respectively.

This significant miss has helped reinforce the argument for easier Fed policy later in the year, especially if growth momentum softens further in the second half. The US dollar index dropped over 1.2% following the release, with weakness seen against the euro and commodity currencies.

The decision to escalate tariffs against China and Beijing’s retaliation has reignited pressure on the renminbi, pushing USD/CNH to a recent high of 7.4290 before easing back toward 7.35. The onshore yuan (USD/CNY) also tested the upper limit of its daily 2% band.

In response, the People’s Bank of China (PBoC) has reportedly stepped in behind the scenes, instructing major state-owned banks to cut back on US dollar purchases for proprietary accounts to reduce FX pressure. While speculation about a broader renminbi devaluation is building, Beijing appears keen to avoid outright depreciation likely to maintain financial stability and avoid stoking capital outflows.

Reports from Bloomberg indicate that China’s top leadership is now preparing to roll out a new wave of stimulus aimed at softening the blow from deteriorating trade relations. Measures could include targeted support for the housing market, consumer demand, and strategic sectors like AI and semiconductors.

The fact that these discussions are happening at the highest levels of government and with urgency signals concern within Beijing about the economic fallout of a prolonged tariff war. More front-loaded stimulus, potentially alongside coordinated financial easing, appears increasingly likely.

Despite the recent bounce in high beta FX and the weakening dollar, MUFG warns that a sustained recovery remains unlikely in the short term. Tariff uncertainties, slowing global growth, and potential stagflation risks in the US still present major headwinds. The pause in US-China escalation may prove temporary, and the outcome of negotiations or lack thereof could once again reset the playing field.

The risk of further renminbi pressure also casts a shadow over Asia FX and commodity-sensitive currencies. For now, MUFG’s base case remains cautious, with expectations of softer economic data in the coming months, gradual weakening of the USD (particularly if inflation slows further), but ongoing volatility as geopolitics and trade dominate.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.