just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

I’m framing this week around three levers that actually move currencies: how the Fed communicates optionality into Jackson Hole, whether global activity data stabilise (PMIs, U.S. growth prints), and how far the BoJ’s tightening “option” can travel now that Japan’s growth looks sturdier.

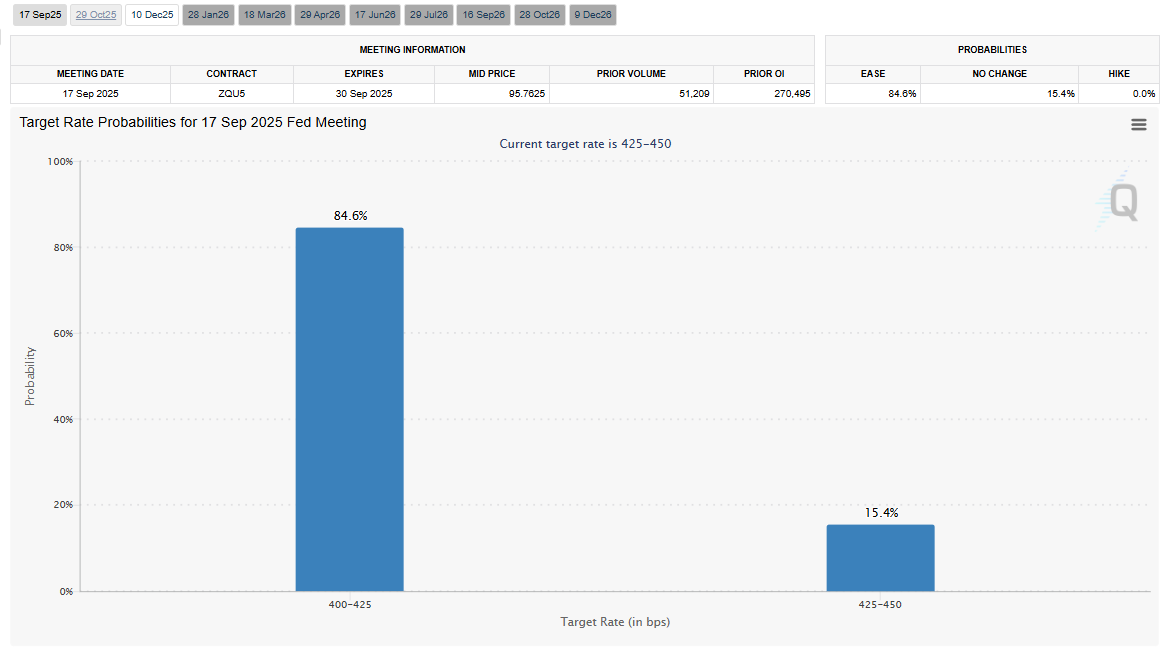

My bias remains that last week’s PPI wobble reset positioning, not the broader path toward gradual Fed easing; the front end firmed, but it didn’t construct a case for hikes. That distinction matters for FX because it tempers conviction, not direction

The core U.S. story into the symposium is that stronger producer prices nudged the market to trim the most aggressive cut expectations, yet left a September step still largely priced.

That dynamic supports a choppy dollar rather than a durable bull trend; the PPI mix added unease about tariff pass-through, but forecasts for the Fed’s preferred inflation gauge were only marginally revised and remain consistent with disinflation that’s slow, not broken.

I’ll respect two-way risk early in the week and re-engage on USD rallies if communication avoids an overt pushback on easing.

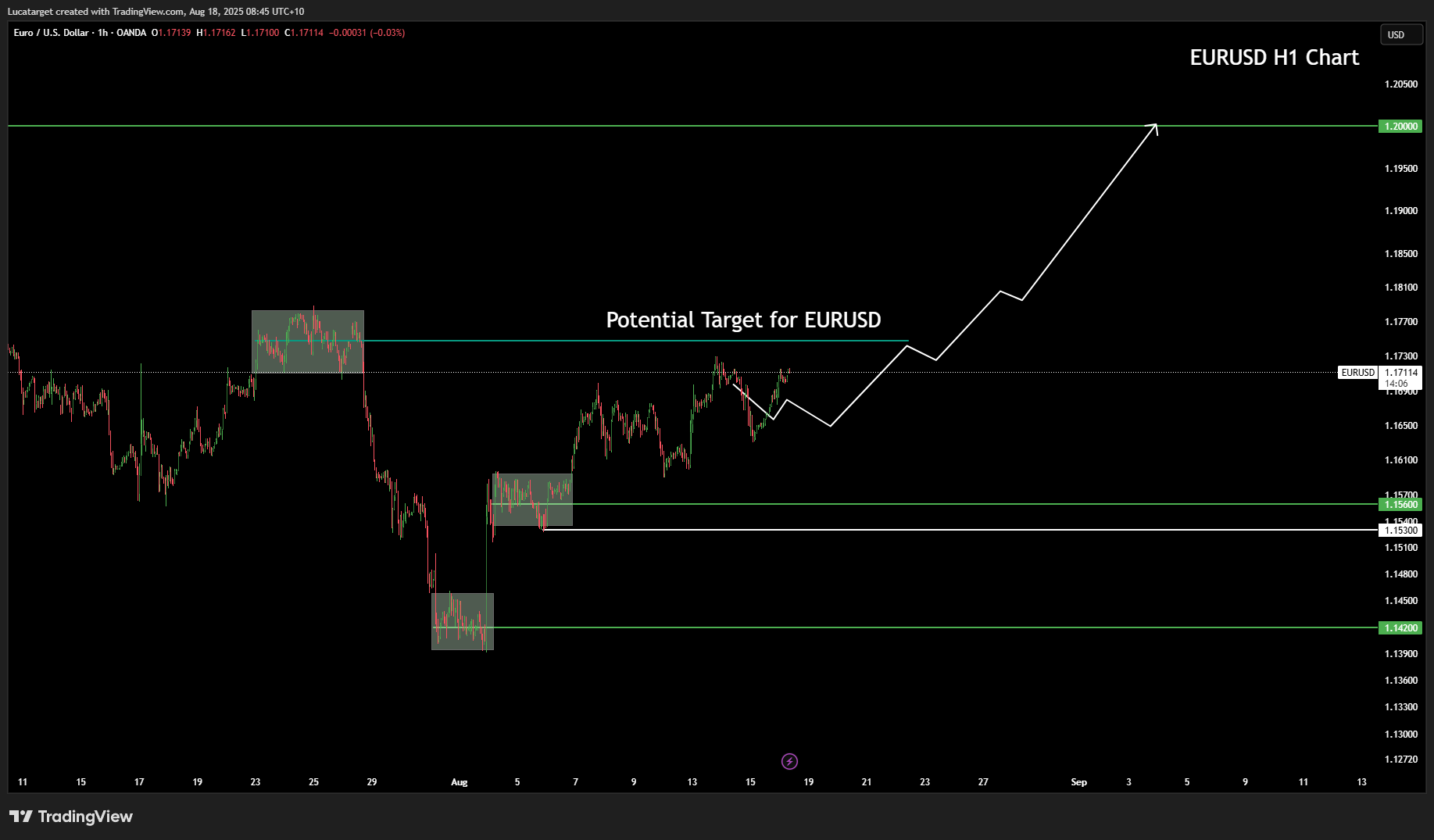

Europe is a patience trade. Desk colour late last week highlighted real-money demand on euro dips and flagged that the next euro-specific catalyst is PMIs later this week; in August liquidity, I prefer to buy pullbacks rather than chase strength.

Sterling stays tactically two-way: resilient on crosses when services inflation anxiety lingers, but sensitive to any hawkish read-through in Fed communication via the USD leg. I’m not paying up for momentum here; instead I’m managing ranges and letting the data do the talking.

Japan is the quiet swing factor. The GDP revision cycle shifted the narrative from “fragile” to “resilient,” with Q2 growth firmer and Q1’s contraction revised away.

That improvement lifts the probability that the BoJ resumes hikes before year-end; if the Fed is easing on a glide path while Tokyo normalises, rate-differential gravity starts working for the yen. My plan is simple: fade USD/JPY strength into resistance and re-add JPY on pops rather than chase breaks in thin markets.

I’m entering the week with a mild, diversified USD-short bias but I’m not running maximum size into the podium. I want the Fed to validate “optional easing” rather than force a hawkish re-price; if they avoid leaning against cuts, the path of least resistance is a softer USD in a low-trend August tape. That’s when I’ll layer into euro on dips (given the PMIs calendar and real-money interest) and re-add yen on strength as BoJ optionality outlives U.S. policy noise

On GBP, I’ll keep it tactical, trade the range and let services-inflation nerves and Fed tone dictate the USD leg rather than pre-commit to a trend week. For beta FX, I’ll keep sizing modest until the front end calms; if it does, I prefer AUD/NZD over CAD for clean anti-USD expression in this window.

This is a week to be patient, not passive. I’m respecting the two-way chop into Jackson Hole, buying EUR weakness, fading USD/JPY strength on the improving Japan-BoJ narrative, and keeping beta FX sized for volatility until the Fed clarifies the cadence of cuts. If the communication simply preserves optionality, the dollar’s path should remain lower by a grind rather than a break, exactly the backdrop where disciplined entry levels and staggered adds pay.

1. What is the main risk for the US dollar this week?

The biggest risk is how the Fed communicates at Jackson Hole. If Chair Powell avoids pushing back on rate-cut expectations, the dollar is likely to weaken gradually. A more hawkish tone, however, could fuel a short-term USD rebound.

2. Why is Japan’s growth data important for FX markets?

Japan’s stronger GDP revisions increase the likelihood of BoJ tightening later this year. If the Fed is easing while the BoJ hikes, the policy divergence favors yen strength, making USD/JPY rallies vulnerable.

3. How should traders approach the euro in August liquidity?

With thin volumes, the euro is better bought on dips rather than chased at highs. Real-money demand has supported EUR/USD on weakness, and this week’s PMI prints will be the next catalyst for direction.

4. What makes sterling more of a range trade right now?

Services-led inflation pressures in the UK complicate the BoE’s easing timeline, which keeps GBP supported at times. However, cable and EUR/GBP are still sensitive to broader USD moves and Fed communication, making it more of a tactical, range-driven play.

5. Which commodity currencies offer the cleanest anti-USD trades?

AUD and NZD are more attractive than CAD in this window. While CAD remains highly sensitive to US growth and oil headlines, AUD/NZD offer better risk/reward if US data softens and the Fed sticks to gradualism.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.