just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

More Hawkish Standpoint in Anticipation of 2024: Contrasting Market Sentiments

As we approach the end of the year, The Street is buzzing with the release of annual outlooks. I will release a comprehensive analysis but still a lot of work to be done so it will be published around early January, the time is ripe to juxtapose my 2024 Federal Reserve (Fed) outlook with the prevailing consensus and the market's implied policy trajectory. In essence, my stance is notably more hawkish than both, although I project 2-3 rate cuts commencing in the middle of the year, as I’ve mentioned on my webinar and my YouTube videos.

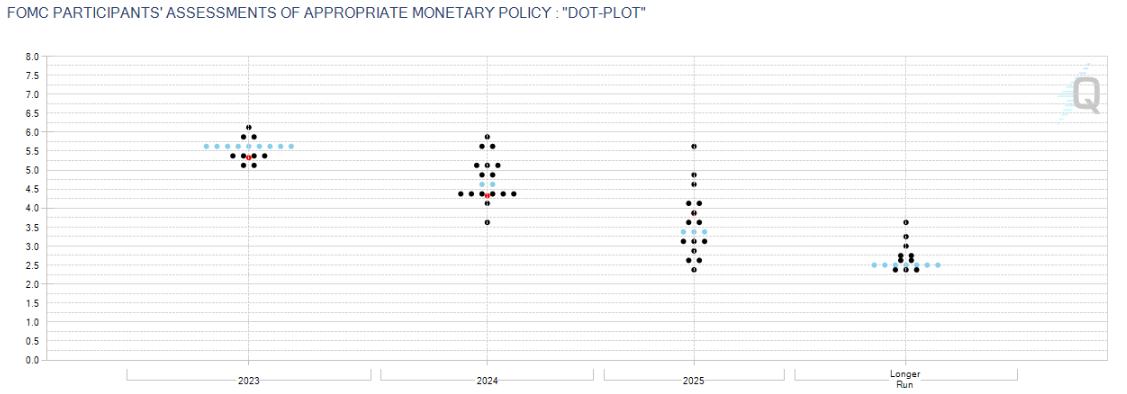

A detailed examination of the chart below unveils the market's anticipated federal-funds rate from now until December 2024. While the consensus aligns with my expectation of no further rate hikes, my forecast deviates as I foresee rate cuts initiating in May. The fed-funds futures curve I present suggests a trajectory with cuts almost every meeting, culminating in an implied funds rate of approximately 4.5% by year-end.

Dot Plot Chart

Source: CME

In contrast, economists surveyed by Bloomberg, not depicted in the chart, project an even lower policy rate of 4.45%. This implies nearly 100 basis points of cuts in the coming year, considering the current effective funds rate is at 5.33%. Additionally, the median dot for end-2024 from the Federal Open Market Committee's (FOMC) September Summary of Economic Projections stands at 5.1%. My viewpoint, anticipating the first rate cut in June or July with at most two additional cuts by year-end, positions the target federal-funds rate between 4.75% to 5%. This trajectory aligns somewhat with the September dots, depicting a less-dovish outlook.

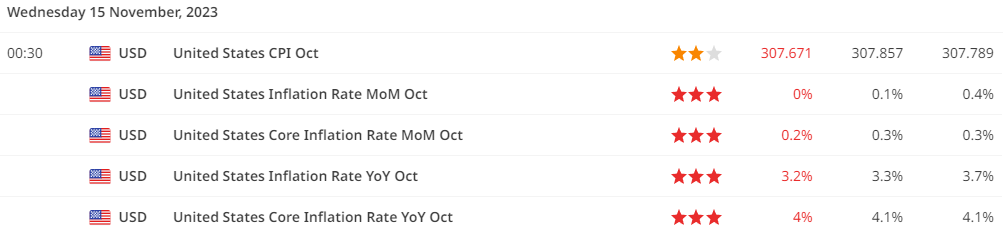

My rationale hinges on the belief that inflation will take most of the next year to approximate the Fed's 2% goal. My 2024 rate forecast assumes a slowdown in the U.S. economy, likely commencing as early as Q4 2023, as we could see already yesterday on the release of the CPI data.

US CPI

Source: Finlogix

This aligns with the Fed's perspective that tightening credit conditions and higher rates will impede economic growth. I anticipate inflation to be around 3% by midyear, and the subsequent cooling, combined with subpar growth, will prompt the Fed to moderate the current restrictive policy setting, albeit without excessive easing.

More dovish forecasts, in contrast, presuppose a more significant economic slowdown than I anticipate. Consensus forecasts project U.S. GDP growth below 1% for the first half of the year, concluding 2024 at 1.7%. The consensus also envisions U.S. core personal consumption expenditures (PCE) inflation below 3% by Q2 2024, settling at 2.5% by year-end. These figures, while not divergent from the Fed's September dots, suggest a more cautious stance.

The crux of the divergence lies in the interpretation of the Fed's reaction function. While consensus and market expectations posit a swift response to slowing growth and decelerating inflation, I maintain a contrary view. I perceive the dots as indicative of a Fed comfortable with a cooling growth scenario, even with a moderate decline in inflation, yet sustaining a relatively tight policy stance.

Shifting Focus to Federal Home Loan Bank (FHLB) Reforms: Implications and Criticisms

Proposed reforms to the Federal Home Loan Bank (FHLB) system are on the horizon, potentially restricting member banks' capacity to provide liquidity during banking system stress. Currently, FHLBs issue advances to commercial banks as a source of liquidity and funding. The suggested alterations favour tapping the discount window for short-term liquidity over relying on FHLB advances.

Examining the historical trends in FHLB advances and discount window usage since 2000 reveals interesting patterns. During periods of stress, FHLB liquidity provision overshadows discount window borrowing. Instances such as the Global Financial Crisis (GFC), the COVID lockdowns, and more recent regional banking stresses in March-April 2023 underscore the significance of FHLB liquidity. This preference may stem from the perceived stigma associated with discount window borrowing, as FHLB advances are less conspicuous and reported less frequently.

Furthermore, the years leading up to the pandemic witnessed a steady increase in FHLB usage, reaching over $500 billion by the end of 2018. Conversely, 2021 and 2022 saw diminished FHLB advances, attributed to the Federal Reserve's ample liquidity provision post-March 2020 lockdowns and the persistent zero-rate environment, facilitating readily available cheap bank funding.

While the proposed reforms remain pending with no definitive timeline, they face considerable criticism. One primary concern questions the readiness of banks to seek discount window financing in the absence of FHLB advances during a liquidity event. If banks are reluctant to turn to the window, the question arises: where will they source liquidity in times of stress?

This contemplation leads to the notion that, in periods of calm, banks might hoard liquidity as a precautionary measure, potentially raising the lowest comfortable level of reserves in the banking system and causing stress on both banks and the overall financial system.

Shifting Gears to Real Money Demand for US Treasuries: An Intricate Market Dynamics Exploration

Extensive discussions about real money demand for U.S. Treasuries have been a recurring theme, particularly emphasizing the positive demand from institutional investors for both bills and coupons. In the realm of bills, institutional investors exhibit a willingness to deplete their cash and short-term securities holdings in favour of higher returns in the bill market. This behaviour mirrors that of money market mutual funds, which, since the postponement of the debt ceiling in early June, have been redirecting their investments from the Federal Reserve's overnight reverse repo facility to T-bills.

Despite this positive trend, a noteworthy player in the domestic market, U.S. commercial banks, has been reducing its holdings of U.S. Treasuries and agency mortgage-backed securities (MBS) since last year. Official Fed statistics indicate a reduction of approximately $500 billion in these positions since February 2022. While total holdings have increased since the pandemic's onset, the ongoing reduction in UST and MBS holdings raises concerns.

The reduction in bank holdings is attributed to the surge in interest rates and mark-to-market losses on securities portfolios, exacerbated by leverage constraints such as the supplementary leverage ratio (SLR). Given my apprehensions about continued robust supply from the U.S. Treasury into 2024, the declining participation of price-inelastic buyers, such as commercial banks, raises concerns about whether price-sensitive buyers will be sufficient to smoothly absorb the forthcoming Treasury issuances.

In conclusion, the intricate interplay of economic forecasts, proposed financial reforms, and market dynamics creates a tapestry of uncertainties. As we navigate the complex landscape of monetary policy, liquidity provision, and Treasury markets, staying attuned to evolving trends and potential risks becomes imperative for informed decision-making in the ever-evolving financial landscape.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feedjust now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.