just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

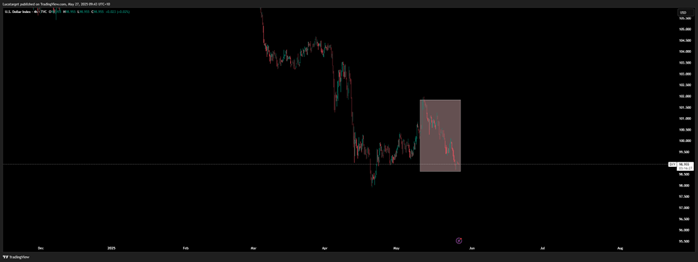

Despite fleeting moments of strength, the Japanese yen continues to struggle against the US dollar, weighed down by a confluence of bond market volatility, unclear policy direction from Tokyo, and renewed speculation surrounding US-Japan trade dynamics. This past week, the USD/JPY pair found itself trapped within a volatile range testing lows near 143 before rebounding modestly amid an absence of any decisive policy action or verbal intervention from either government.

The much-anticipated finance ministers’ meeting between the US and Japan, held on the sidelines of the G7 gathering, offered little in terms of currency-specific developments. Both sides reaffirmed that there was “no discussion of exchange rate levels,” a phrase repeated from earlier communiqués. Yet markets remain unconvinced that currency diplomacy is entirely off the table. Parallel reports that the US did broach FX policy in talks with South Korea have kept traders alert to the possibility that Japan may be under subtle pressure to engineer a stronger yen through domestic policy tweaks.

The yen’s recent rebound toward the 143 handle was short-lived. It occurred after a weak 20-year Japanese government bond (JGB) auction sparked a jump in long-end yields, drawing in some speculative yen buying. However, the relief faded quickly as investor nerves returned. A similar dynamic unfolded in the US, where the Treasury's own 20-year auction was also poorly received, underscoring broader market unease with duration risk on both sides of the Pacific.

One might expect rising JGB yields to signal yen weakness, mirroring the dynamic often observed with US Treasuries. Yet this time, the relationship is decoupling. The rise in Japanese yields appears driven less by inflation expectations or hawkish Bank of Japan (BOJ) signalling and more by sheer market indigestion. The recent JGB auction posted the longest tail since 1987 an unmistakable sign that investors are demanding a higher premium to hold long-duration Japanese debt.

The BOJ, for its part, is facing calls from market participants to tread carefully as it considers its next move in tapering its bond purchases. A recent survey released by the BOJ’s Financial Markets Department revealed a split in opinion: some urge caution given the jump in superlong yields, while others advocate for accelerating tapering efforts. For now, the most likely path appears to be a continuation of the current reduction pace enough to maintain credibility, but not enough to spark a bond market revolt or yen surge.

Japan’s latest inflation print added an unexpected twist to the narrative. Core CPI (excluding food and energy) rose to 3.5% year-over-year in April the fastest pace in about a year raising eyebrows among policymakers and investors alike. This will add weight to the upcoming BOJ-hosted conference on May 27–28, where Governor Kazuo Ueda and his deputies are expected to provide updated guidance.

The central bank is still operating in a delicate balancing act: expressing openness to future rate hikes while avoiding signalling a policy shift that could destabilize fragile domestic markets. With Fed officials, including Christopher Waller and John Williams, also attending, any hints of policy coordination or divergence will be closely parsed for signals on future USD/JPY direction.

The dollar’s recent broad-based softness, with the DXY once again slipping below 100, has offered some mechanical relief to the yen, as well as to other G10 currencies. Yet the extent of USD/JPY correction remains capped by persistent uncertainty over the BOJ's policy normalization and broader macro divergence.

Investors are still digesting stronger-than-expected US economic data, including firm retail sales and labour market resilience. These figures continue to support a “higher-for-longer” narrative for Fed rates, keeping upward pressure on UST yields and the greenback. Until we see clearer signs of Fed dovishness or a BOJ shift with teeth the yen will remain at the mercy of global crosswinds.

In the near term, the USD/JPY looks set to remain stuck in the 141–145 range. However, the risks are increasingly asymmetric. If the BOJ’s messaging this week /next week leans toward policy normalization particularly considering the inflation surprise and if US-Japan trade talks yield any more hints of FX coordination, we could see the yen catch a second wind.

But the path forward is muddied by geopolitical overhangs, uncertain Fed timing, and the unresolved question of how much appetite Tokyo really has for a stronger currency. The weak-yen narrative is not dead but it is increasingly contested, and markets are starting to prepare for a shift in tone.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.

Want to master the markets? A winning trading mindset beats a perfect strategy. Learn how emotional discipline helps you conquer fear and avoid heavy losses.

Read our latest Gold price action forecast to see how a double top pattern triggered a massive XAU/USD selloff.

Wondering how the API weekly report impacts oil prices? Learn how U.S. crude stockpiles and voluntary surveys predict the official EIA report.

cTrader Mobile 5.9 introduces a dedicated charts tab, single-tap chart access, a draggable floating action panel and a new focus mode for positions and orders, following the platform's Best Mobile Trading App win at UF Awards Global 2026. Sergey Borisov of Spotware comments on the update.