Search Companies, News, Members & more

Terms of ServicePrivacy PolicySecurity PolicyLegal InformationCommunity GuidelinesSitemapsCookie Settings

2026 Copyright © Liquidity Finder Ltd. All rights reserved.

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Fusion Capital and the DEX Liquidity Revolution

Published on Mar 11, 2026

Updated on Jun 20, 2026

The crypto liquidity space has grown rapidly over the past few years, and brokers searching for a provider now have more options than ever. That makes it harder to tell who is doing what differently. So when I caught up with Jasper Cooney from Fusion Capital last week, I wanted to get beyond the usual pitch and understand how the business actually works behind the scenes. And to learn more about the significance of their recent connection to the Hyperliquid.

Jasper is Fusion's Head of Product, based in London, and is the kind of person who talks about liquidity aggregation with genuine enthusiasm, a clear opinion, and no interest in pretending it is more complicated than it needs to be. He also happens to be a crypto native, not a tradfi convert, which gives him a perspective that is refreshingly different from the usual institutional FX veterans I spend my time speaking to.

A Crypto-Focused Hedging Venue

So what is Fusion Capital? The short answer is that it is a specialist crypto-focused hedging venue for CFD brokers. The firm works with brokers who need to offload risk on their crypto volume, whether that means direct STP execution for their end clients or manual hedging by their dealing desk.

"Effectively, we're a crypto-focused hedging venue is sort of how we like to brand ourselves. We work with brokers who need to offload risk on their crypto volume. Be that trading directly onto us as an STP for their clients or manually hedging."

Jasper Cooney

Head of Product, Fusion Capital

What makes Fusion more interesting than a standard liquidity feed is the level of customisation. The team creates bespoke pricing configurations for each client. Some brokers want large top-of-book depth on major coins for manual hedging, so they know exactly what price they will get when they click. Others want tight spread pricing across hundreds of altcoins to pass through to their retail clients. Fusion builds both, and everything in between.

"Some of the brokers want to know what they're hitting on large size. So we'll create a feed which is an all-in spread price, guaranteeing one Bitcoin always at top of book."

Jasper Cooney

Head of Product, Fusion Capital

Fusion currently offers over 350 crypto CFD pairs and expiring futures, with pricing aggregated from around four major crypto exchanges, several of the large non-exchange market makers, and, most recently, a growing roster of decentralised exchanges. The pricing is routed through Gold-i, one of the most established trading technology providers in the industry. Fusion's development team in Poland has built an in-house layer that sits between Gold-i and the exchanges, handling rebalancing-execution and risk management on Fusion's behalf.

Pure A-Book, but Smarter Than That Sounds

One of the most interesting things about Fusion is its business model. The firm is pure A-book. Every trade is hedged. But the way it monetises that hedged flow goes well beyond simply marking up a spread.

"We're pure A-book and basically we utilise the volume to do arbitrage in the back, be it convergence spread arbitrage or funding rate arbitrage. That's basically how we monetise."

Jasper Cooney

Head of Product, Fusion Capital

I asked Jasper to explain this in plain English.. In the crypto world, different exchanges charge funding rates (the crypto equivalent of swap or overnight financing rates) at different intervals, some hourly, some every eight hours. These rates vary dramatically between venues. At any given moment, one exchange might be paying longs while another is paying shorts.

"Some of the exchanges might be paying longs and some of them might be paying shorts. So it's about how we can move our positions around in the background to ensure we can get paid or at least get the best rate."

Jasper Cooney

Head of Product, Fusion Capital

For the client, none of this complexity is visible. They get a clean, tight price and agency execution. Behind the scenes, Fusion is running a sophisticated operation that allows it to offer very competitive pricing while still generating revenue from the volume. It is a neat model and explains why the business is focused on winning high-volume clients rather than charging fat spreads.

The funding rate landscape in crypto is, incidentally, pretty fascinating. Much more complex than FX. Jasper pointed me to Coinglass, which tracks funding rates across all major exchanges in real time. In quiet markets, Bitcoin funding rates might sit at around 3% annualised. During extreme volatility, they can spike to 20% or more. On smaller altcoins, Jasper has seen rates hit 3,000% annualised, which is obviously extraordinary for anyone short and collecting. There is a growing industry of arbitrage desks in London doing nothing but buying spot and shorting the perpetual to harvest funding rates, a strategy that barely exists in the FX world. (Who knew?)

The Inverse Price Problem

One technical detail that came up in our conversation, and which I think is worth explaining for readers less familiar with crypto aggregation, is the issue of inverse pricing. When you aggregate liquidity from multiple exchanges and market makers, it is entirely possible for the buy price from one source to be lower than the sell price from another, resulting in a crossed or inverse spread. In the FX world, this would be a gift to any arbitrageur. In the crypto world, it happens routinely.

Fusion sets a minimum spread of zero on all external feeds so that clients never see an inverse price (MetaQuotes, among others, simply cannot handle one). But internally, those price dislocations are exactly where Fusion's "Raptors" go to work.

"It's kind of about what we do in the background with trading that price convergence and divergence with our own tech, which is how we actually monetise it ourselves. Even when we're showing the clients a really tight price, it's about what we do with the volume in the back, which is our speciality on our trading desk."

Jasper Cooney

Head of Product, Fusion Capital

Execution That Can Handle Size

For a relatively young business, Fusion has demonstrated it can handle serious size. Jasper described a recent instance where a single market order for 20 Bitcoin was executed with zero slippage, split across a couple of exchanges. The firm's feeds are built to show one Bitcoin at the top of book, with depth extending to eight or ten Bitcoin within a couple of dollars.

"We've had I think 20 Bitcoin in a clip before which actually executed with very good slippage, which was cool because we hadn't really seen that ticket size of one single transaction. I think it was actually zero slippage."

Jasper Cooney

Head of Product, Fusion Capital

Fusion holds VIP-tier accounts at all its exchange partners and is co-located on their servers for optimal execution speed. The team is also in regular dialogue with some of the larger exchanges about how they manage risk, sharing knowledge from the traditional FX world in exchange for a deeper understanding of how the crypto venues operate internally.

One area Fusion is watching closely is CME's crypto futures, particularly as the exchange moves towards extended trading hours. While Fusion already offers dated futures from crypto native exchanges, the CME product is more likely to become an internal hedging tool for the desk than a product offered directly to clients.

Toxic Flow: A Problem That Doesn't Seem to Exist

Coming from the FX world, where the phrase "toxic flow" can send a bank's risk desk into a cold sweat, I was curious whether Fusion ever encounters similar problems. In FX, latency arbitrage, aggressive news traders, and clients who sweep the book across multiple venues are all considered problematic. Banks routinely ask their intermediaries to turn off specific clients or restrict access.

In crypto, the picture is completely different. I asked Jasper directly whether any of his exchange partners had ever complained about the nature of the flow they were receiving. His answer was surprising to me.

"We're always hearing about it but to be honest we've never seen it. The exchanges aren't going to complain about any sort of flow. I mean there's people arbitraging them all day. Volume's volume and we're back to back. The client's getting filled at the same price we're getting filled at. We never take the trade before we've placed it, so it's never warehoused."

Jasper Cooney

Head of Product, Fusion Capital

This is a striking contrast with the FX market, where the sensitivity around flow quality has become almost pathological. In crypto, the sheer number of venues, the prevalence of bot trading, and the decentralised nature of price discovery mean that arbitrage is not just tolerated but is seen as a natural and healthy part of the ecosystem. It actually helps harmonise prices across exchanges. For brokers coming from the FX world, where they may have internalised the anxiety around flow toxicity, this is worth understanding: in crypto, aggressive flow is not a problem. It is the market.

A Crypto Native, Not a Tradfi Convert

Jasper's route into the industry is worth a mention because it says something about the culture of the business. He came straight out of Oxford Brookes University into Bitcashier, the crypto payments platform focused on high-ticket USDT liquidation for the luxury goods market (yachting, mainly). Bitcashier's CTO, Marc Dominic, had started working on the Fusion concept at around the same time, and Jasper was there from the very beginning.

"Fusion came out of Bitcashier just as an idea because it was where the volume was. It was always in the derivatives in crypto. So it was sort of how do we capture that? And then fell into this liquidity provision thing because we didn't want to go after retail, that's a whole hassle."

Jasper Cooney

Head of Product, Fusion Capital

The team worked its way through the institutional crypto landscape, attending every expo, having hundreds of conversations with prospective clients about what they actually needed, and iterating the product accordingly. There is no legacy FX thinking embedded in the business. That has its advantages: the team is not weighed down by assumptions about how things are "supposed to work" in institutional markets, and it moves fast. Jasper became Head of Product on the strength of having built much of what Fusion now offers.

We were discussing what I see as the tension between the tradfi and crypto worlds (both competing for each other's business) , and he noted that while the crypto exchanges could learn from the tradfi world on risk management, the platforms themselves, Hyperliquid in particular, are in many ways much more advanced than anything the FX industry has produced.

"The crypto platforms are awesome. Hyperliquid, the features on those platforms are really cool. It all comes from a new industry with its own idea of how a trading platform should look, which is quite interesting."

Jasper Cooney

Head of Product, Fusion Capital

Hyperliquid: The DEX That Changed the Game

The most exciting part of our conversation centred on Hyperliquid, the decentralised perpetual futures exchange that is growing at an extraordinary pace. Built on its own Layer 1 blockchain, Hyperliquid has processed over $200 billion in monthly trading volume and has become the only DEX to rank among the top 10 derivatives exchanges globally. It offers up to 40x leverage on crypto, zero gas fees, and a fully on-chain order book that delivers execution speeds comparable to centralised exchanges.

(For readers more familiar with the traditional FX world, a quick primer. A DEX, or decentralised exchange, is a trading venue that operates without a central operator or intermediary. There is no company holding your funds, no central order matching engine in the traditional sense, and in most cases no KYC requirement. Anyone, anywhere in the world, can connect their crypto wallet and start trading. Trades are executed and settled directly on a blockchain through smart contracts. Think of it as the difference between trading through a broker and trading directly on a public ledger where the rules are enforced by code rather than by a compliance department. DEXs have grown from a niche corner of crypto into serious venues. Hyperliquid, the largest of them, now processes more derivatives volume than most centralised exchanges and ranks among the top 10 globally.)

Fusion recently integrated with Hyperliquid through Gold-i, and the results have been immediate. The addition of DEX liquidity has tightened Fusion's pricing to its best levels ever and opened up a new universe of arbitrage opportunities between centralised and decentralised venues.

"It's a whole new world to the other exchanges. It creates opportunities for arbitrage and different order books. Pricing and inversions. Our price is as tight as it's ever been now for clients."

Jasper Cooney

Head of Product, Fusion Capital

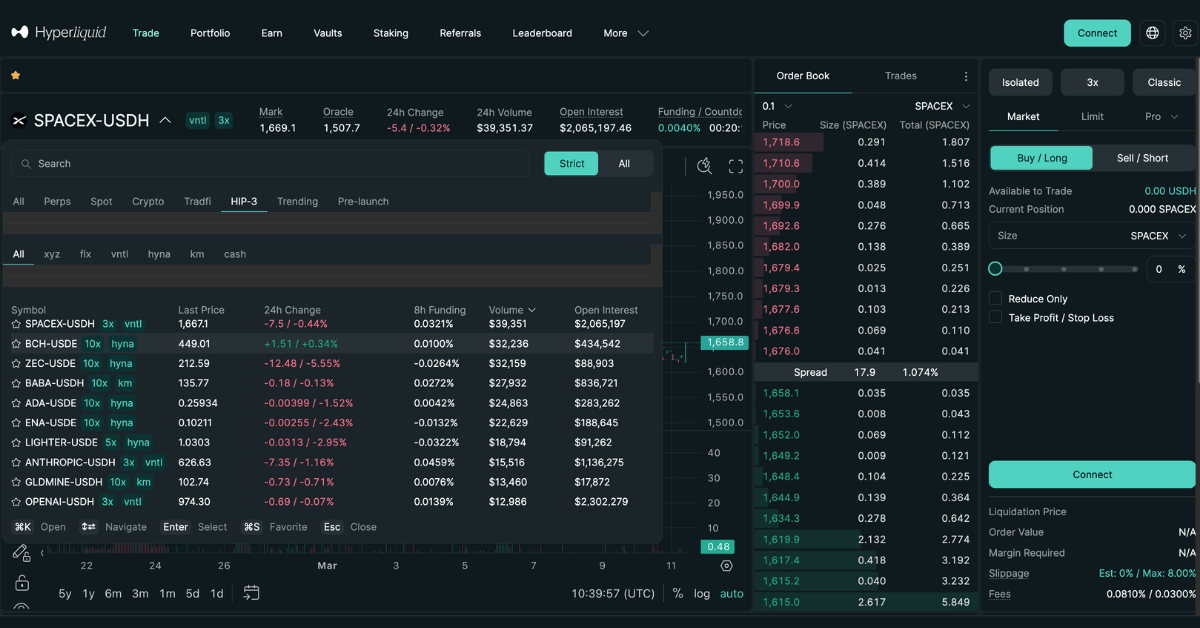

What makes Hyperliquid exciting is its HIP-3 protocol, which allows anyone to list a new perpetual contract by posting collateral. This has led to the creation of perpetual futures on traditional assets including silver, Brent crude, natural gas, and, most intriguingly, pre-IPO companies. The volume on HIP-3 products is growing at around 50% per month.

Image: Hyperliquid's dealing screen

Because Fusion is now connected to Hyperliquid, these products are in principle available to its broker clients. The implications are significant. A retail broker using Fusion's pricing could offer its end clients the ability to take a position on SpaceX before it lists, or trade commodities perpetuals over a weekend when traditional markets are closed. These are products that simply did not exist in the retail brokerage ecosystem a year ago.

Perhaps the most striking detail about the Hyperliquid integration is how it happened. Fusion did not have a single conversation with a human being at Hyperliquid. There was no sales call, no onboarding team, no account manager. They found the API documentation, connected it through Gold-i, and went live.

"We haven't spoken to anyone. We actually found the API and we've connected it. Literally there is no one to speak to."

Jasper Cooney

Head of Product, Fusion Capital

That is, in a nutshell, how the decentralised world works. And it is both impressive and slightly unsettling in equal measure. Fusion is also adding other DEXs including Lighter and Aster, whose order books offer further depth and opportunities.

A Trading Desk, Not a Sales Machine

One thing that became clear during our conversation is that Fusion sees itself as a trading desk first and a sales operation second. The firm does not currently have a head of sales. Instead, it is moving towards a distribution partnership model, working with larger intermediaries who can channel volume through Fusion's infrastructure without the firm having to attend every expo with a badge and a pitch.

"Our strength is our execution and basically our tech and what we can do on the back of volume. Our strength is almost as a trading desk as opposed to a sales company."

Jasper Cooney

Head of Product, Fusion Capital

The ideal Fusion client is a CFD broker with a significant B2B operation, because B2B flow tends to come in larger ticket sizes and higher volumes, which is exactly what the Raptors need to do their work in the background. The firm is not interested in prop firms that B-book everything; that generates no hedgeable volume. It is all about flow.

Swap Rates: Stability in a Volatile Market

Funding rates in crypto can be bewildering for anyone coming from the FX world, where overnight swaps are charged once at 10pm and rarely move dramatically. In crypto, rates can swing from 3% annualised to 20% or more on Bitcoin, and Jasper mentioned seeing 3,000% on some altcoins during extreme volatility. They change by the hour on some exchanges.

Fusion simplifies this for its broker clients by charging swaps once a day, in line with FX convention, and dictating its own rates rather than passing through the underlying exchange rates in real time. The rates are updated only when there is a material shift. For brokers, that means predictability and a cost structure they can plan around. If a broker wants to offer perpetual futures as a product and charge more granularly, Gold-i has tools that can replicate the exchange-level funding rate structure.

Why Fusion Capital Is Worth a Closer Look

The crypto CFD liquidity space is competitive and noisy. It is easy for a broker evaluating providers to end up with a shortlist where everyone looks the same: tight spreads, deep liquidity, fast execution. Jasper was honest enough to acknowledge this problem head-on.

"I've shown people pricing before and they go, well, that's just normal. The pricing's really deep and it's really tight and it updates really quickly. So then it's got to be something else."

Jasper Cooney

Head of Product, Fusion Capital

"That something else", in Fusion's case, translates into tangible advantages for the broker. The in-house trading layer means Fusion can offer tighter pricing without sacrificing its own margins, because the revenue comes from how it manages the flow, not from how much it charges for it.

The willingness to build bespoke feeds means a broker gets pricing configured for their specific business model, not a generic one-size-fits-all product.

Access to Hyperliquid and other DEXs means a broker can offer their clients products that most competing providers cannot yet deliver, from weekend crypto perpetuals to pre-IPO names like SpaceX. And because the team is technically driven rather than sales-led, problems tend to get solved by the people who built the system, not passed up a chain.

The Hyperliquid integration alone is a compelling reason to have a conversation with Fusion. The ability to offer retail broker clients access to pre-IPO perpetuals on names like SpaceX, crypto perpetuals with deep DEX liquidity, and traditional asset perpetuals that trade over weekends is a product set that most competing providers cannot yet match.

Fusion is not the biggest name in the space. It does not have a vast sales team or a presence at every conference. What it does have is a small, sharp, technically excellent operation that builds its own tools, hedges everything, and is constantly looking for the next venue or product that gives its clients an edge. In a market where everyone's pricing looks the same, that matters more than most people realise.

If you are a broker looking to upgrade your crypto offering, Jasper Cooney is the person to speak to. He will not give you a sales pitch. He will give you a straight answer. Which, in this industry, is worth quite a lot.

Found this interesting? Become a member of LiquidityFinder and get daily industry news direct to your inbox. Join here.

Author

| Sam Low is the Founder of LiquidityFinder. With over 18 years in working with FX trading technology, Sam has deep experience in the FX (forex) trading industry, working with brokers, liquidity providers and end traders themselves. | You can message Sam directly here. |

What is Fusion Capital? +Fusion Capital is a crypto liquidity and hedging venue for brokers. It provides pricing, execution, and market access for firms that want to hedge crypto CFD exposure efficiently rather than warehouse that risk internally.

What does Fusion Capital actually provide to brokers? +Fusion provides crypto pricing, liquidity access, execution infrastructure, and hedging support. That includes bespoke liquidity feeds, support for manual and automated hedging workflows, and access to a broad set of crypto CFD pairs and expiring futures.

How is Fusion Capital different from a standard liquidity provider? +Fusion is differentiated by its tailored pricing model. Instead of delivering one generic feed to every broker, it builds configurations around the broker’s real requirements, including top-of-book depth, tighter spreads, broader altcoin coverage, or pricing designed specifically for manual hedging and risk transfer.

What does “pure A-book” mean? +Pure A-book means trades are hedged externally rather than internalised. The provider is acting as an execution and risk-transfer venue, not warehousing the broker’s flow as principal risk in a B-book model.

Why does A-book matter in crypto? +It matters because crypto markets are volatile, fragmented, and fast-moving. Hedging flow externally reduces exposure to sharp directional moves and gives brokers a cleaner execution model when they want to pass risk out rather than keep it on their own book.

How can Fusion Capital offer tight pricing and still make money? +Because its economics do not depend only on spread mark-up. A venue like Fusion can monetise flow through execution optimisation, arbitrage opportunities, spread convergence, and funding-rate differentials across venues while still showing competitive prices to clients.

What is a DEX? +A DEX, or decentralised exchange, is a trading venue that operates on blockchain-based infrastructure rather than through a traditional central intermediary. Users generally connect via wallets and trade through systems that are executed or settled through on-chain or blockchain-linked mechanisms.

How is a DEX different from a centralised exchange? +A centralised exchange controls onboarding, custody, market access, and the trading environment directly. A DEX removes much of that central control, allowing users to interact more directly with the market infrastructure. That changes how access, custody, settlement, and listing models work.

Why do DEXs matter for brokers? +DEXs matter because they create new pools of liquidity, new order books, and faster product innovation. For brokers, that can mean better price formation, more differentiated products, and access to markets that may appear on decentralised venues before they reach traditional providers.

What is Hyperliquid? +Hyperliquid is a decentralised perpetual futures venue known for combining on-chain infrastructure with a fast, order-book-based trading experience. It has become one of the most important decentralised derivatives venues in crypto.

Why is Hyperliquid important? +Hyperliquid is important because it proves that a decentralised venue can offer serious derivatives liquidity, strong usability, and rapid product development. It is a meaningful venue in its own right, not just a niche DeFi experiment.

How can Hyperliquid improve pricing for a liquidity provider? +By adding another high-quality live order book into the aggregation mix. More credible venues usually means tighter pricing, better routing choices, more efficient hedging, and more opportunities to capture price differences across markets.

What kinds of opportunities does Hyperliquid create? +Hyperliquid creates opportunities in pricing, execution, arbitrage, and product access. It can improve liquidity quality while also opening up markets and instruments that are newer, less widely distributed, or unavailable through many traditional providers.

Can DEX liquidity make a broker’s product offering more competitive? +Yes. DEX liquidity can help brokers offer tighter prices, more diverse crypto exposure, and access to newer products that emerge first in decentralised markets. That can create a real competitive edge in a crowded brokerage landscape.

Why is bespoke pricing important for brokers? +Bespoke pricing matters because different brokers have different flow profiles. A broker hedging larger tickets manually needs something different from one streaming prices to smaller high-frequency flow. Tailored pricing improves execution quality and makes the feed more useful in live trading conditions.

Why is crypto liquidity harder to evaluate than it first appears? +Because headline claims such as tight spreads or deep liquidity do not tell the full story. What really matters is how stable the price is, how much real size is behind it, how quickly it updates, and how well the venue performs when volatility and ticket size increase.

Who is Fusion Capital best suited to? +Fusion is best suited to brokers with meaningful crypto flow that needs proper hedging. That includes brokers with active crypto books, larger ticket sizes, or a need for more tailored liquidity and execution support than a generic mass-market feed can deliver.

Share this article

Comments

Most Recent

Find The Right Partners for

Your Trading Business

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Risk and dealing analytics provider BrokerPilot helps multi-asset brokers spot toxic flow before it eats into their P&L. Chief Revenue Officer Sergey Berezhnoy talks to Sam Low about catching toxic patterns across MT4, MT5 and cTrader, why new brokers get targeted from day one, and where AI fits into the dealing room without replacing the human dealer.

The Lowdown - newsletter. Something significant is happening in financial markets right now. Prediction markets are the new shiny object, and they are definitely now an institutional asset class. In the same way that brokers scrambled to add crypto to their offering a few years ago, the smartest operators in our space are already asking how they access prediction markets.

n in-depth review of TMGM (TradeMax Global Markets), the ASIC-regulated ECN broker offering raw spreads from 0.0 pips, MT4 and MT5, copy trading via HUBx and ZuluTrade, and 24/7 multilingual support across four regulated jurisdictions. Find out if TMGM belongs on your shortlist.

LiquidityFinder's Sam Low sits down with Nathan Sage, founder and CEO of Sage Capital Management, to trace his journey from FX fund manager to running a Bitcoin fund doing $1BN a day in 2016 — and how that experience of pain built one of the most connected prime brokerages in the digital assets market today.

Gold at record highs, oil as a meme stock, and crypto exchanges eyeing your clients. Watch our expert panel - Gold-i, Your Bourse, Tapaas and Devexperts - discuss broker risk management, , AI trading and the MetaTrader debate.

Over a long tapas lunch in Shoreditch, London, Sam Low sits down with Peter Brooks and Jess Reed from ADMISI eFX, the dedicated electronic FX desk operating inside one of the world's largest agricultural commodities companies. What emerges is a compelling case for why this largely unknown operation deserves serious attention from brokers, payments firms, corporate treasuries, and digital asset companies alike.

Explore live spread and quote benchmarks powered by the Tradefora Composite Index (TCI), an independent dataset aggregated from multiple FX and CFD brokers. View average, minimum and maximum spreads by instrument and timeframe, plus composite bid/ask quote data updated continuously at millisecond precision.

In Part 6 of his A-Book STP series, Youssef Bouz from GCC Brokers looks at how the rise of algorithmic and AI-assisted trading is forcing brokers to rethink risk models, revenue strategy, and long-term sustainability, and why trader longevity, not short-term extraction, is the real measure of a resilient execution business.

Create Your FREE Account

Get access to latest news, updates, real-time data, brokerage and trading firm insights and customized information feeds.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities Secures Full CMA Category 5 Licence in the UAE - Opens Regulated Office in Dubai

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.

Feed