Search Companies, News, Members & more

Terms of ServicePrivacy PolicySecurity PolicyLegal InformationCommunity GuidelinesSitemapsCookie Settings

2026 Copyright © Liquidity Finder Ltd. All rights reserved.

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

JP Morgan's JPMD - A Tokenised Deposit Cum Stablecoin

Published on Jul 19, 2025

Updated on Mar 7, 2026

JP Morgan has announced that it will be issuing a stablecoin-like token, called JPMD, on a public blockchain.

Importantly, the token is permissioned. So, yes, it is on the pubic blockchain, but holders are “by invitation only”. Upfront, the guest or whitelist is limited to JPM Institutional Clients only.

To date my take on tokenised deposits has been: “Not useful outside the four walls of the place that issued them”. Specifically, my view has been that using JPM Coin or Kinexys is like have an extra discrete account in a specific currency which works on new technology or rails.

JPMD adds mew dimensions. To quote Keynes: “When the facts change, I change my mind …” In this case, the facts have changed. In this post I’ll explain my thinking.

As with all things bleeding edge in financial services, there is every risk that I haven’t understood properly, or just missed a few salient points, or just come to an implausible conclusion. If any of things are true, please call me out on them.

Why is this an important topic?

Let’s start at the beginning. With a good old TradFi account at JPM, or any Nostro, when you want to make a payment you send the instruction to JPM. Funds are then moved as book transfers if the recipient / payee also has a JPM account or IRL via a payment system, such as the FedWire, CHIPS, CHAPS or T2. But there are limitations on timing; business days end in late afternoon, early evening and the batch nature of the systems mean nothing happens at the weekend.

JPM broke out of this “legacy systems albatross” with JPM Coin and Onyx, which is now Kinexys. The “train” is the same; an account and a payment, but the “rails” are different. New technology enabling 24 * 7 * 365 processing.

The change meant that JPM clients could send and receive funds from any other client using Kinexys at any time. This is useful if a meaningfully large or all-encompassing group of clients all bank with JPM. An example where this is the case is India, with local banks using JPM to settle dollar trades.

At this point, you will understand my saying: “Not useful outside the four walls of the place that issued them”.

Kinexys is also a path for JPM to payments system renewal. Instead of trying to adapt, upgrade and fix the old rails, JPM have taken a really sensible path here. Trying to have a big bang, with the one stopping and the other starting, could be done, but requires huge planning. Allowing things to exist in parallel, whilst minimising investment in the old, legacy systems, reduces the operational risks involved. One of co-existence. There is a parallel from TradFi; bank branches with counter service vs. ATMs. Only some 50 years after the first ATMs were introduced did banks begin to push through widespread closure of their counter services.

What’s new or changing?

Quite often, people I interact with talk about public blockchains and private permissioned chains. Two discrete things. For reasons which are easy to imagine; KYC, transaction monitoring, sanctions screening, in other words all the regulatory must do stuff, which regulated financial institutions have to do. There is though a hybrid or in-between flavour: public permissioned.

This is an important concept. The token circulates on the public blockchain but only amongst approved users. A private members’ club. In the case of JPMD, the membership is limited to JPM’s institutional clients.

Using the public blockchain opens up interoperability, programmability and composability. The holy trinity of digital asset capabilities. Here’s my thinking of what this means in practical terms.

Today, an institutional client wanting to trade digital assets will often be required to pre-fund cash with whichever marketplace or broker it is using. In the TradFi world, if the client uses JPM and the marketplace uses Citi, then money has to move IRL and that can be slow. In technical terms, this type of set-up has credit risk and liquidity risk, as well as making liquidity management harder than it might be.

That works a bit better if both client and marketplace have a TradFi fiat Nostro with the same bank. Not really a scalable solution for the marketplace. And limited by all those TradFi opening hours and cut-off times.

Things work a bit better if you use Kinexys; the opening hour restrictions largely go away. But, there is the same limitation for the marketplace. And, as the client you still need to pre-fund the marketplace aka venue aka exchange.

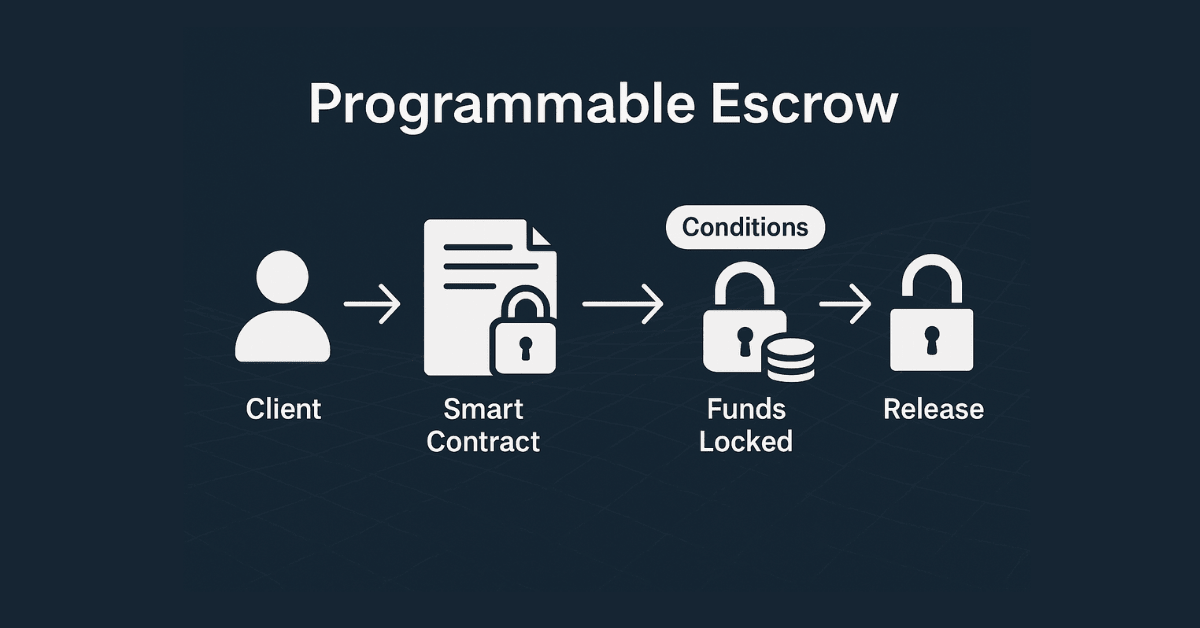

Once the client accounts are on a public-permissioned blockchain, all parties can take advantage of that holy trinity of digital assets. Back to that institutional client wanting to trade. Once it has some JPMD on a public chain, it could send a buy order to a marketplace, which in turn would use interoperability to earmark enough JPMD to cover the order and then try to execute. If the order is not filled, a quick kill instruction would lift the earmark, and the client can try its luck at another venue. Now exactly the same thing could be done with USDC or USDT; JPM is offering optionality. Programmability might be used for an escrow arrangement; when an order is placed, it enables funds to be earmarked, and then later transferred when pre-agreed conditions are met.

In technical terms, there is still credit risk, but vis a vis JPM rather than one or more marketplaces. There is no liquidity risk; one pool of liquidity serving the marketplaces and settlement needs which have accounts at JPM. There is still some liquidity management to be done, balancing fiat needs and tokenised deposit needs, but life is easier. In the long run, the fiat part will become smaller and smaller.

In terms of accounting and reporting, I don’t think there is any change here; today in fiat, or even Kinexys, JPM keeps track of client balances. With the advent of JPMD, JPM will still be accountable for things AML / CFT. That will force them to monitor the follows of their JPMD token between wallets. This is the same range of work as if they process a TradFi book-transfer between two JPM clients.

So clients have the ability to use the full range of new services on the public blockchain as long those they want to interact with also use JPM.

Now, somethings do not change. The issued JPMD is still a liability in JPM’s books and still has to be reflected in the liquidity calculations: LCR, NSFR.

In conclusion

JPM has done our industry a service with this step. Public permissioned is an important step.

I need to update my take on tokenised deposits:

Old: “Not useful outside the four walls of the place that issued them”.

New: “Useful inside the four walls of the issue or the private members’ only gardens controlled by the issuer”.

There is hope for even more useful developments. In times past, I have spent many hours in the world of securities settlement, dividends and withholding tax reclaims. These are elongated, paper-based processes. In my days at Goldman Sachs in Zurich, we had to collect all the confirmations of net dividends received and withholding tax deducted, then fill out forms, then submit these to HMRC in the UK for a stamp that entitled Goldman Sachs Intl to reclaim 20 of the withheld 35% under the double tax treaty, and then submit the stamped forms to the Swiss Federal tax folk. Potentially that could be much simpler: HMRC issues Goldman Sachs International a token on a public chain validating their right to that refund. The Swiss tax folk can see the position, the gross dividend paid, and the HMRC token all in the same wallet. A smart contract can execute the repayment of 35% of the withholding to token-holding wallets without any manual review or effort. Outside the upfront smart contract work, there is no on-going admin. Governments could reduce headcount. Could - but whether they will or not is an entirely different matter.

Things JPMD all work really well as long as all those who want to play are JPM clients. Rather like Google with search, and to some extent Apple with the App Store, JPM is building an ecosystem which could give it monopoly power in the long-run. I am an Operations guy who has spent his career settling trades and making payments. The main ingredient has been the use of financial market infrastructure (FMIs) to do that. The idea that we would all have to use JPM does not sit well.

My thanks to Mike Manning and Dani Heller for reviewing the draft and making some useful edits and observations.

Thanks for reading. Please do let me know what you think of these notes. Feedback via the comments would be great.

Author

|

Olaf Ransome is a liquidity and financial services expert. He is the founder of 3C Advisory You can message Olaf directly here. |

Share this article

Comments

Most Recent

Find The Right Partners for

Your Trading Business

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

SoFi's SoFiUSD is the first stablecoin issued by a US national bank. But do holders actually have the protection they think?

Brent Xu left Wall Street for blockchain in Ethereum's earliest days. Now his Franklin Templeton and Galaxy Digital backed platform Dora is bringing fractionalised bond trading to retail brokers. He speaks to Sam Low.

Discover whether KuCoin is still “The People’s Exchange” in 2026. This in-depth KuCoin review breaks down fees, KYC, security, Proof of Reserves, supported coins, deposits/withdrawals, futures, margin, Earn and the platform’s standout free trading bots — plus who it’s best for (and who should avoid it).

Gas fees can be the most confusing part of using Ethereum and other blockchains. This guide explains what gas fees are, why they exist, how costs are calculated (including EIP-1559’s base fee and priority tip), and the key factors that drive price spikes. You’ll also learn practical ways to reduce fees using gas trackers, smarter timing, batching, and Layer 2 networks like Arbitrum, Optimism, Polygon and zkSync.

Generating and sustaining liquidity requires a strategic approach across centralized exchanges, decentralized pools, and market-making relationships. This guide covers every stage of the process for crypto projects.

This guide covers how proof-of-stake works, the best assets to stake, liquid staking protocols, and the risks you need to understand before committing funds.

S&P Global Ratings gave Tether (USDT) the weakest Stablecoin Stability Assessment. Olaf Ransome breaks down what drives stablecoin risk—asset backing, custody/correspondent chains, transparency and reporting.

Decentralized exchanges (DEXs) allow peer-to-peer trading without intermediaries. This guide covers how AMMs work, how to connect a wallet, understand liquidity pools, manage slippage, and trade safely across Ethereum, BNB Chain, and Solana.

Create Your FREE Account

Get access to latest news, updates, real-time data, brokerage and trading firm insights and customized information feeds.

Spotex has appointed Joe Tuccio, previously Head of Digital Partnerships at Seabury Capital, as Head of Digital Assets. Tuccio brings 20 years of financial markets experience and will lead partnerships with liquidity providers and custodians as Spotex expands its institutional FX venue into digital assets.

RoboForex has integrated its MobileTrader platform into Telegram as a Mini App, giving traders account management, order execution, analytics and copy trading access within the messaging platform, with real-time synchronisation across Telegram, iOS, Android and web versions.

Learn how deliberate practice can improve your trading skills faster than spending more time on the charts. Discover practical tips to build discipline, consistency, and long-term trading success.

XS.com has appointed Anna Pastusenco as Group PSP and Banking Manager, tasking her with leading global payment partnerships across banks, EMIs and PSPs. She joins from IC Markets, bringing experience in payment infrastructure, banking relationships and commercial negotiations to the global broker's expanding payments ecosystem.

Looking at the latest Gold XAU/USD price action? See why a bearish trend continuation point to a massive drop.

Want to learn how to trade ECB events? Discover the top strategies for ECB announcement days, including volatility trading and breakout tactics.

Darwinex has integrated with TradingView, letting traders on the charting platform build a verified, publicly auditable track record from every trade. The move links Darwinex's regulated broker and Darwinex Zero development platform to investor capital allocation, based purely on trading performance.

Pepperstone has appointed Mohammed Almadhoun as Head of Middle East and Osama Hamdan as Head of Sales, strengthening its regional leadership team as the FX and CFD brokerage continues its expansion across the UAE, GCC and wider MENA region following its Dubai office launch.

Payments company Stripe and private equity group Advent International have launched a joint offer to acquire New York-listed payments group PayPal in a deal that would value the business at around $53bn, according to the Financial Times.

ATFX has launched the World Trading Cup, a three-stage trading competition offering up to USD 210,000 in prizes. Pre-registration opens 20 July 2026, with regional qualifiers and finals leading to a global final in December, where 15 traders from five regions will compete for the championship title.

Feed