just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

In a post fact rationalisation the FT put the reason for the dramatic drop in precious metals on Friday down to the nomination of Kevin Warsh as Federal Reserve chair. It is more likely that the timing of the 2 events was more coincidence than related. All parabolic moves end in a dramatic fashion, the timing of the pullback is what keeps people (dealers) on the edge of their seats. It's just a question of when, and how deep your pockets are to outlive any sustained rally.

The gold rally in persepctive. Weekly Gold price from 2004-2026, source: TradingView (click chart to see live chart)

The gold rally in persepctive. Weekly Gold price from 2004-2026, source: TradingView (click chart to see live chart)

Hope is not a strategy. But everyone knows (don't they) that gold and silver move in very mysterious ways and should be treated with extreme caution. There are some well known examples of where this went wrong a couple of years ago which should have been a big enough warning to others. Maybe a lot of brokers we are yet to hear about ‘closed the stable doors after the horse had bolted’, but for others, they were lucky. The pullback must have saved a few who must have been teetering on the edge. Many are now waiting to hear what the fallout may have been with smaller brokers without the deep pockets or nerves of steel.

In

, there are some nuggets of wisdom.Lesson Number 1: “Don’t underestimate the other guy’s greed”

Lesson Number 2: “Don’t get high on your own supply”

No successful dealer should get high on their own supply.

An asset manager asking their broker “Is it safe?”

The move in Gold has been challenging not just for brokers, but also for major market makers and liquidity providers, because it combined speed, size, and leverage. When precious metals move sharply, the pressure escalates quickly from the retail client level to the broker level, then to the broker’s margin and credit lines with liquidity providers and even the exchange (CME). The key question is: ‘Can every link in the chain can meet its obligations?’ As the MD of a B2B LP told me over the weekend, in stressed conditions, trust disappears and cash becomes the priority. Risk management turns from ‘commercial flexibility’ (trust) into “pay now” behaviour, pushing clients to top up immediately, reducing willingness to extend credit, and tightening operational controls.

Having deep capital behind the business, and flow coming from multiple regions and client types, helps smooth the impact of one-way retail positioning or concentrated exposure. This is what will have saved some brokers last week, but not all.

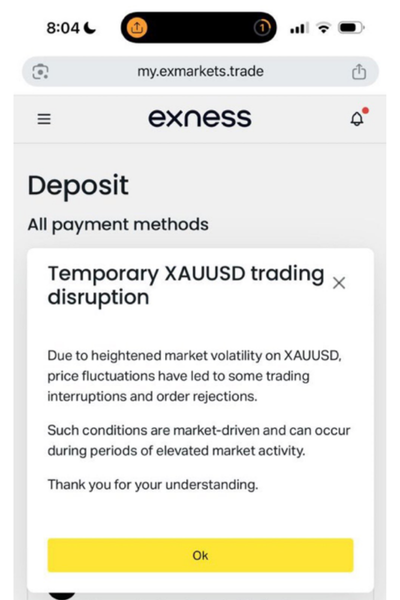

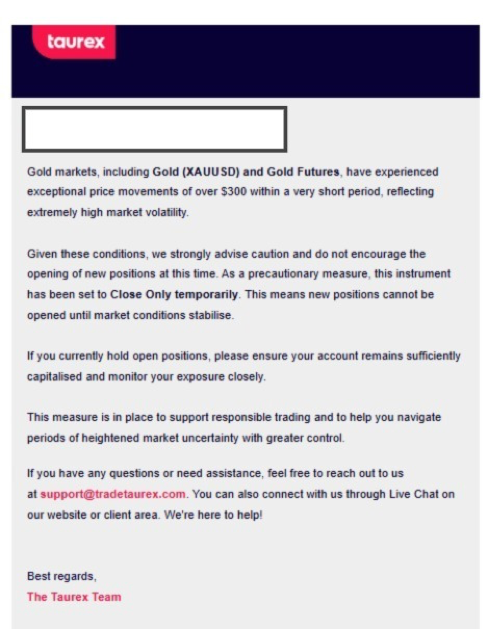

There was a screenshot doing the rounds on Friday from an FCA regulated (and multi-other jurisdictions regulated) broker who had gone close-only on Gold “to support responsible trading”. Exness, who are notorious for shockingly high leverage offered to clients, were being complained about on X for informing clients about “Temporary XAUUSD trading disruption”, which some were (mis-)interpreting as being shut-out of trading Gold.

This reminds me of the ‘degens’ reaction to Robinhood literally shutting traders out of Gamestop (if you haven’t seen the “Eat The Rich” series on Netflix, I highly recommend it).

Rumours and screenshots matter because they influence sentiment. Even if information is unverified, market rumours about brokers accelerate client anxiety, liquidity demand, and precautionary de-risking across the ecosystem which is what was happening last week. I was getting unsolicited calls from brokers letting me know about the market chatter.

So – the more prudent professional clients are getting vocal about concerns they have with the stability of brokers they are trading with (against). A very active fund contacted me to ask whether the broker they are going live with next week are safe. Just to reassure the new client, I checked in with their LP. The LP concerened told me they had taken a lot of risk-off at the end of December, decreased NOPs, increased margins and sent most of the risk external rather than on the books. Good to hear.

Joe Roeder, CEO of MarketsVox, another LiquidityFinder listed broker, who has (according to them) exceptional gold liquidity (spreads and top of book depth) told me also they went risk-off some time ago. These guys have many years in the market and know when to spot the signs.

The risk of getting it wrong with gold is well known. There are cautionary tales out there (IYKYK).

I checked in with Youssef Bouz from GCC Brokers, one of the A-book brokers who participated in our recent webinar on A-book v B-book, to see how he his business has been faring over the past few days.

“Absolutely abnormal. These are dates many in the market won’t forget. While the moves put pressure on everyone, at GCC Brokers our priority was keeping trading conditions and execution as stable and uninterrupted as possible, allowing clients to make informed decisions, while ensuring client safety and responsible risk management remained intact at all times. By communicating timely updates and clear information throughout the period, clients became more aware of the market realities, more sensible in their approach, and we genuinely saw appreciation for the efforts taken to protect them during these conditions.”

Our Webinar on B-book/A-book covered the fact that pure A-book brokers are the exception rather than the nor. However, A-book brokers on the call consistently framed their decision as one driven by alignment and survivability: passing all client flow directly to liquidity providers removes directional exposure, reduces “black swan” tail risk, and allows management to sleep at night. Several of the ‘A-team’ referenced historic stress events (notably SNB 2015 and recent gold volatility) as proof that brokers running warehoused risk can survive by luck, but are always one event away from failure. You can watch a recording of the webinar here.

Coming in on the other side of the debate is an article from Anya Aratovskaya who pitches the case that an A-book is not necessarily a recipe for a good night’s sleep: The A-Book Comfort Lie: Risk Never Left the Building (My view – Although she is correct, an A-book is not a panacea for all risk, there are degrees of risk though. A-book brokers decrease market risk, the largest and most obvious of all risk).

Bitcoin is off sharply, and there is talk that people are liquidating BTC holdings to cover margin calls in Gold.

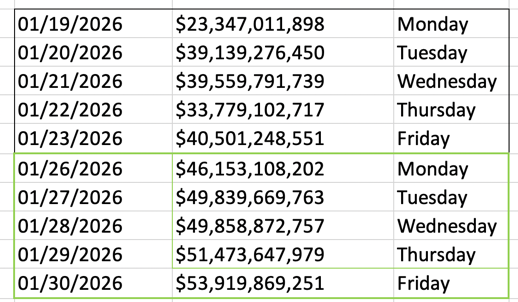

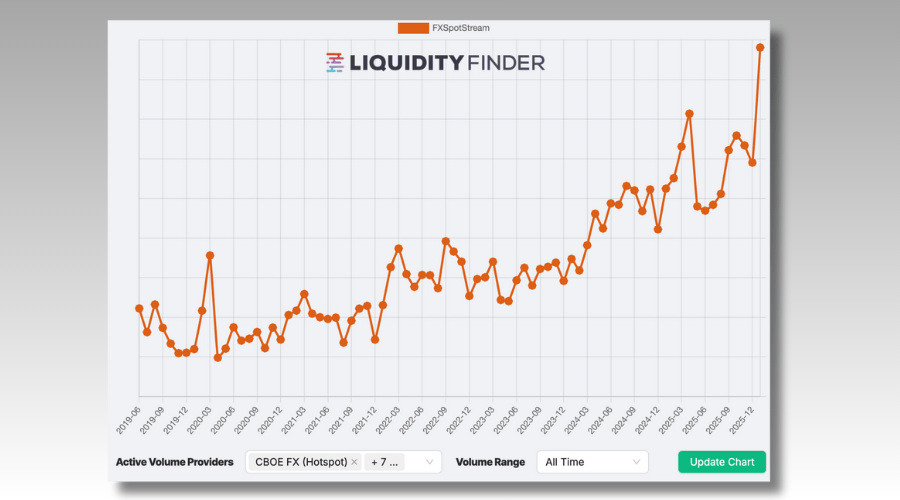

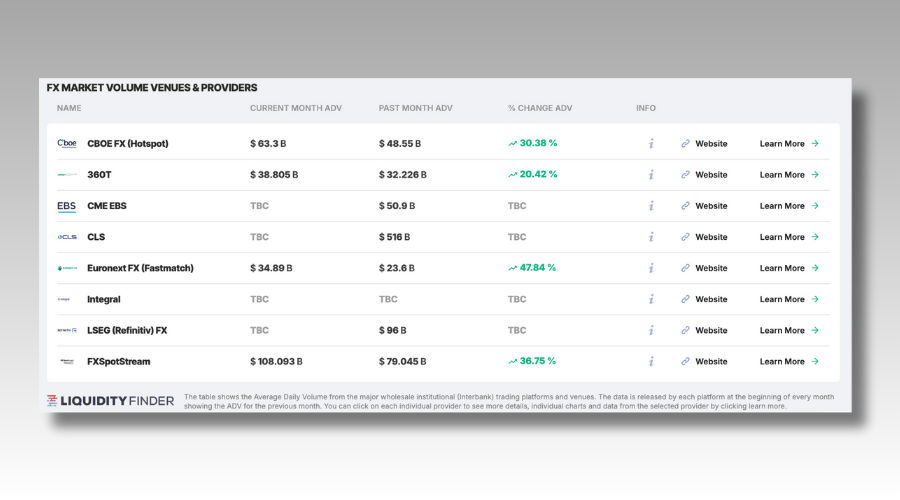

SpotFX volumes also rose dramatically last week, and monthly ADVs for January are coming in. FXSpotStream has reported all-time high record average daily volumes in January. Most of the venues picked up spead in the last 2 weeks, with last week going nuts. As an example, looking at the daily volumes from Euronext Fastmatch over the last 2 weeks:

Euronext Fastmatch SpotFX ADV in last 2 weeks of January

Euronext Fastmatch SpotFX ADV in last 2 weeks of January

FXSpotStream's Average Daily Volumessince 2019, reaching a record in January 2026

The ADVs for the major interbank SpotFX platforms can be viewed here

Shout out to Ricardo Dias from Spotware who is now posting his insights in to LiquidityFinder’s feed. I am all in favour of the arguments set out in this post explaining why unscrupulous brokers and prop firms will never use cTrader. You can follow him here.

WikiFX like to portray themselves as the guardians of safety. See this press release from last week where ‘WikiFX announced the further clarification and standardization of its broker evaluation…’ https://finance.yahoo.com/news/wikifx-announced-further-clarification-standardization-055600717.html I noticed none of the financial industry news sites covered this. I wonder why they felt it necessary to push this out? Very intriguing. It is well known how they treat 'clients' to get their reviews in shape. The evidence would seem to contradict the words in this press release.

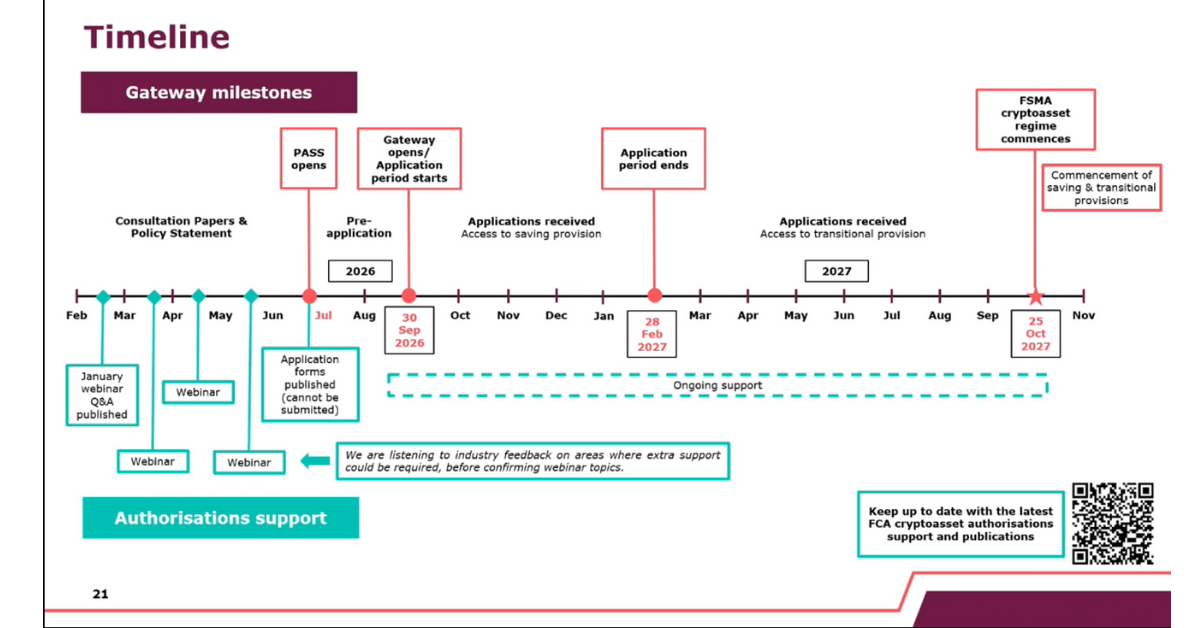

The real “Guardians of the (Financial Trading Industry) Galaxy” are the unsung heroes in the back office, the SMFs. This occurred to me while I listened in to the ‘New regime for cryptoassets regulation – Authorisations introductory webinar’ last week. Billed as: “Hosted by the FCA’s Authorisations team, this webinar will introduce the upcoming changes to the regulatory regime for cryptoassets under the Financial Services and Markets Act 2000 (FSMA). We’ll cover who will be affected by these changes and outline our expectations when assessing applications.” It sort of sounded exciting.

The FCA's timeline for implementation of the new regime for Cryptoassets

The new FCA Cryptoasset authorisation regime has started (“But the horse has already bolted to Dubai!” I hear you say?) and is set to go live in October 2027.

In preparation for this, the Heads of Back office functions with code names like SMF4 (Chief Risk Officer), SMF10 (Chair of the Risk Committee), SMF16 (Head of Compliance), SMF17 (MLRO) have to navigate this timeline and prepare documentation for the FCA ahead of any permissions to offer Cryptoasset trading in the UK.

I feel for them. Without these unsung heroes wading through all these webinars and supplying the right documents, and eventually being ultimately responsible should things go wrong, the industry doesn’t move forward. The rest of us can go outside in the sunshine (have beers) and have fun (do Sales) while the people keeping us all ‘safe’ beaver away at all the documentation. They will rarely make the headlines, and if they do it will be for the wrong reasons.

I hope the markets go your way this week.

Sam

P.S. I recommend following Ipek Ozkardeskaya from Swissquote on YouTube who helps make sense of the markets on a daily basis.

We're the largest marketplace to connect with brokers, Fintech companies & digital asset firms. Want to partner? Let's get in touch.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.