just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

There’s something brewing beneath the surface, something bigger than just short-term noise. Over the past couple of weeks, we’ve witnessed a rare alignment: the US dollar falling sharply, equities retreating, and Treasury yields rising. That trifecta signals more than volatility it suggests we may be staring into the early phases of a confidence crisis in US assets.

To be clear, this isn’t just about currency moves or speculative trading. It’s about global investors starting to question the very underpinnings of the US macroeconomic and policy environment. And that could reshape the FX landscape for months ahead.

Let’s start with what triggered the market tremors: the Trump administration’s aggressive tariff hike on Chinese imports 145%, to be exact. Beijing didn’t hesitate to respond, raising its own to 125%. These aren’t just numbers; they represent a tectonic shift in global trade dynamics. The risk here isn’t just about bilateral tensions it’s about systemic shock to supply chains, corporate margins, and inflation expectations worldwide.

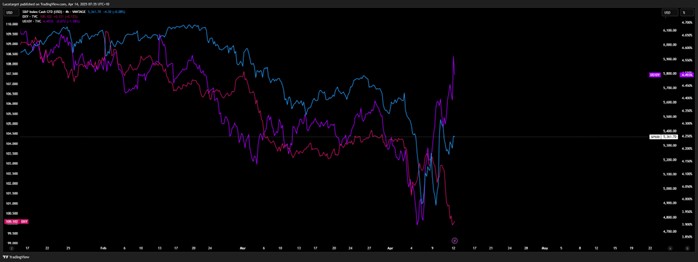

The S&P 500 fell over 7% since early April, and the DXY dollar index has dropped to levels not seen since the early days of the Russia-Ukraine war. This time, however, yields have moved higher, not lower further cementing the notion that confidence is cracking, not just in the currency, but in the broader US macro framework.

While some are asking whether the Fed will step in to calm bond markets, the reality is more sobering. This is not your classic exogenous shock. The current disarray has been largely self-inflicted. The Fed has already slowed the pace of quantitative tightening, and while ending QT entirely might be on the table, a return to QE feels like a stretch especially with inflation risks still lingering.

In fact, it’s becoming clear that monetary policy alone won’t restore order. Until there’s a shift in fiscal posture be it a walk-back on tariffs, or clarity on US debt sustainability—any Fed action would likely have limited impact.

There’s a growing narrative that this dollar weakness might not be accidental. The recent buzz around Stephen Miran’s “Mar-a-Lago Accord” proposal has drawn attention. While not official policy, the idea of realigning the global trade system through a weaker dollar lens seems to be gaining traction within Trump’s orbit. The question is whether markets are now pricing in the possibility that a softer dollar is part of the plan.

If that perception grows, we could see extended dollar declines, especially in a context where policymakers refuse to send a clear “strong dollar” message.

With capital flowing out of US assets, where is it going? The euro and the Swiss franc are clearly in demand. EUR/USD has blasted through prior resistance and could soon test levels not seen since early 2022. Even with the European Central Bank expected to cut rates again this week, the EUR remains well supported proof that yield spreads are no longer the dominant driver.

As for the CHF, the story is even more striking. USD/CHF has fallen to its lowest level since 2011. The Swiss National Bank now finds itself in a corner, with inflation still subdued and the currency surging. Intervention might be their next step negative rates are on the table again, though still seen as a last resort.

Japan is also attracting safe-haven flows, with the yen benefiting from both risk aversion and improving domestic yields. Japanese investors may have been net sellers of foreign bonds recently, but foreign buyers have returned to the JGB market in size—a sign that capital preservation is taking priority.

While the USD sell-off has extended to the broader G10, not every currency is reaping the same benefits. The AUD, NZD, NOK, and SEK continue to show more erratic patterns, caught in the tug-of-war between commodity volatility and global growth anxiety.

The RBA, for instance, held rates steady at 4.10% in its latest meeting, signalling caution despite moderating inflation. Yet with Trump’s tariff bombshell raising new recession risks globally, Australia’s interest rate path remains uncertain. Markets are already pricing in a cut by May, and all eyes will be on the next CPI report to see if that dovish turn materializes.

CFTC data reveals a notable trend: leveraged funds have cut back on long USD positions for nine straight weeks the longest streak in over a decade. Instead, we’re seeing renewed appetite for EUR, JPY, and even GBP, albeit cautiously. This kind of shift in positioning often precedes a sustained move not just a blip.

In portfolio terms, safe-haven demand is showing up clearly in trades like short NOK/JPY. The trade war narrative, paired with falling oil prices and increased OPEC+ supply, has put the NOK under pressure, while the JPY rides the wave of de-risking. Expect this theme to continue unless we see a meaningful shift in tone from Washington or signs of de-escalation from Beijing.

The key takeaway is this: we are entering a phase where the dollar is no longer benefiting from its traditional safe-haven role. The market is repricing not just risks, but fundamentals. Fiscal uncertainty, trade aggression, and political gridlock are now the dominant themes—overshadowing yield differentials or rate path assumptions.

Unless the US makes a clear policy, pivot be it on tariffs, fiscal discipline, or dollar communication the path of least resistance for the greenback remains lower. In this context, the EUR, CHF, and JPY are likely to remain in favour.

For traders and strategists, this is no time to rely on outdated playbooks. We’re in a macro environment where capital allocation decisions are being reshaped by geopolitical noise, fiscal dysfunction, and the erosion of US policy credibility. Navigate it wisely.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feedjust now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.