MARKET REPORT

UK jobs data adds to GBP uncertainty ahead of tomorrow's CPI

To talk to us about your next trade, call 020 7778 7500 or hit the button below

Email us

- USD falls for the first time in six days as reports of a potential US-Iran oil sanctions waiver moderate crude prices and pull global bond yields off recent highs.

- UK jobs data shows shock payroll number keeps GBP under pressure ahead of tomorrow's CPI.

Recap

USD lost ground for the first time in six days on Monday, with the Bloomberg Dollar Spot Index falling 0.2-0.3% after reports that the US proposed a temporary waiver of Iranian oil sanctions, moderating oil prices and pulling global bond yields off recent highs.

GBP gained across the board, further supported by the IMF upgrading its 2026 UK GDP growth forecast to 1.0% from 0.8%, and a late session boost as Andy Burnham pledged to reject any changes to UK fiscal rules, calming bond markets and giving Labour a rare vote of confidence on fiscal outlay. The move is nonetheless best treated as a tactical bounce. The political situation remains fluid.

This morning's UK jobs data has added fresh uncertainty. Payrolled employees dropped 100,000 in April, far worse than the 10,000 expected and the largest single-month fall since the pandemic. The ILO unemployment rate ticked up to 5.0%. GBP sold off on the release and BoE rate hike pricing was trimmed to 57bps from 62bps, though sterling has since stabilised, given the data's known reliability issues. Tomorrow's CPI print is now the next key test.

Today

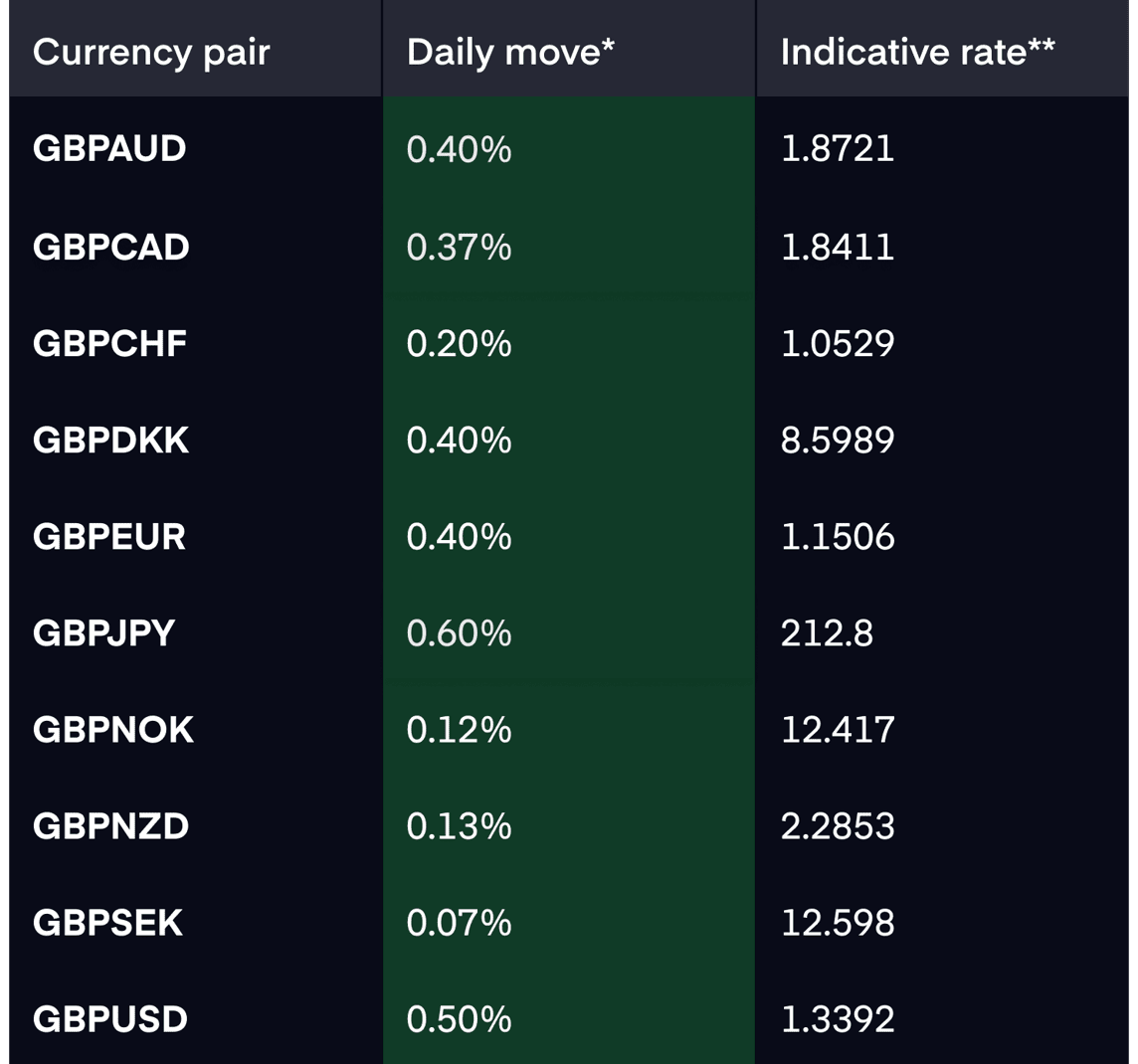

Market rates

*Daily move - against G10 rates as of 5pm BST on 18.05.26

** Indicative rates - interbank rates as of 5pm BST on 18.05.26

Market rates

*Daily move - against G10 rates as of 5pm BST on 18.05.26

** Indicative rates - interbank rates as of 5pm BST on 18.05.26

Our thoughts

Overnight, USD edged higher versus major peers as President Trump holding off on a planned Iran strike failed to lift market sentiment, with markets still viewing Middle East developments as fluid and preferring to see further progress before adding risk.

CAD is in focus at 13:30, with headline CPI expected to jump sharply to 3.1% YoY from 2.4%, a significant move that would reinforce the Bank of Canada's cautious stance and provide a meaningful tailwind for the loonie. Core measures are seen as broadly stable, so the headline print will do the talking.

Oil and Iran headlines remain the broader macro factor. Yesterday's report of a potential US temporary sanctions waiver moderated oil prices and pulled USD lower but the market remains sceptical given how drawn-out negotiations have been. Any reversal of that narrative would see oil push higher again, supporting USD and weighing on risk sentiment.

For GBP, all eyes now turn to tomorrow's CPI print at 07:00. A hotter-than-expected reading could claw back some of this morning's losses and reassert BoE rate hike expectations. A soft print would compound the pressure from today's weak payrolls and leave GBP vulnerable heading into the weekend.

How we can help

Our team of currency experts are here to help you get more from your money when making international payments. We will work with you to understand your payment needs and offer specialised guidance on the best options available to you. Over the last 20 years we’ve helped over a million customers and last year alone processed over £12bn. We’re tried and trusted, and we’re ready to help you.

Get in touch with our team today on +44 (0)20 7778 7500 or email dealingdesk@equalsmoney.com.