just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

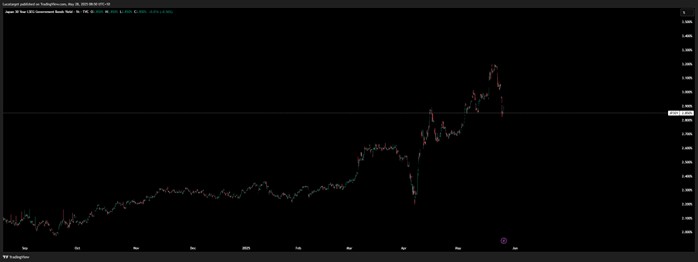

We begin the week with another display of macro-market contradiction: long-end Japanese government bond yields collapsed, yet USD/JPY soared. The culprit? Reports that Japan’s Ministry of Finance is considering scaling back issuance of super-long JGBs an effort to stabilize the bond market after the sharp 90bp rise in 30-year yields since April. That spike prompted the MoF to send an unusually broad questionnaire to market participants and plan a primary dealer meeting for June 20. The signal is clear: Tokyo is worried about investor appetite. But in FX terms, the knee-jerk yen weakness may be short-lived.

Governor Ueda’s comments at a BoJ event added nuance. He sounded incrementally more confident that the central bank could lift rates later this year, assuming the inflation trajectory holds. That’s a big "if," but the OIS market is already pricing in a modest 16bps of tightening by December. Against a backdrop of shaky USD sentiment fuelled by political risk and anticipation of Fed cuts—the yen still looks poised to claw back some ground if yields stabilize and sentiment on US assets continues to deteriorate.

Elsewhere, Trump’s trade policy flip-flops returned to centre stage. After threatening to slap 50% tariffs on all EU imports starting June 1, he reversed course following a weekend call with EU Commission President Ursula von der Leyen. The new deadline? July 9 ironically the same day the current reciprocal tariff truce expires. This delay injected a dose of optimism into markets, as both sides now scramble to cobble together a trade deal. Still, the sheer unpredictability of US policy continues to undermine global confidence in the greenback.

The euro, while initially rattled by Friday’s tariff threat, has regained ground, reflecting not just hope for a trade compromise, but also a growing narrative around de-dollarization. ECB President Lagarde’s Berlin speech framed this moment as a chance for the euro to reclaim a more dominant role in global reserves arguing that erratic US leadership could open the door for Europe to build out the kind of integrated fiscal, economic, and security framework needed to elevate the euro’s status. That’s a long-term vision, but markets are paying attention.

Back in the UK, GBP continues to trade with remarkable resilience. Cable has punched through 1.35 and now eyes 1.3650 as the next resistance. The pound's strength especially relative to the euro has forced traders to rethink cross positions. The 0.8380/85 area (home to the 200-day moving average) has been holding firm, but a sustained break could target 0.8330. Month-end flows are near, which could trigger bouts of USD demand, but overall, there’s little reason to abandon core USD shorts unless we get meaningful shifts in data or Fed tone.

Speaking of data, it’s a light week though eyes are on US durable goods and consumer confidence prints. For Canada, last week’s hotter-than-expected CPI and strong retail sales dragged USDCAD below the 1.3700 mark. With some residual pricing for a BoC hike still in play, the loonie’s path from here likely depends more on global risk appetite than domestic surprises.

In the Antipodes, AUDUSD flirted with a breakout above 0.6510 before collapsing back to the 0.6450 region, once again frustrating bulls. The 200-day moving average near 0.6447 is holding for now, but confidence is fragile. Meanwhile, NZD faces a pivotal RBNZ meeting tonight, with markets fully pricing a 25bp cut to 3.25%. The key will be the forward guidance particularly any changes to the terminal rate. A dovish signal could push AUD/NZD higher, but the market has been long this cross for some time, and expectations are high.

The dollar remains under pressure from political instability, weak macro surprises, and global scepticism. The yen’s dip looks vulnerable, the euro has narrative support, and the pound continues to outperform. In this environment, selective USD shorts still make sense particularly against currencies with improving domestic narratives or less political noise.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.