MARKET REPORT

Ceasefire Optimism Fades as Middle East Tensions Resurface

To talk to us about your next trade, call 020 7778 7500 or hit the button below

Email us

USD rebounds after Wednesday's sharp sell-off as fragile US-Iran ceasefire shows cracks with Tehran claiming violations

- Oil whipsaws from 13% plunge to recovery as Strait of Hormuz remains blocked despite truce agreement

Recap

Wednesday's powerful risk rally has quickly unravelled. The ceasefire optimism that sent USD down 0.8% and oil plunging 13% evaporated overnight after Iranian officials claimed three clauses of the agreement had been breached, with Israel launching major strikes on Lebanon adding further fuel to the fire. GBPUSD surged 1.4% on the day – its largest single-day gain since March 19; whilst EURUSD jumped 1.04%.

GBPEUR was marginally softer, as ECB hike expectations are proving stickier than BoE bets, with traders pricing less than 50 basis points of ECB hikes for the year. CAD was the notable G10 laggard, with WTI crude plunging 17% on the ceasefire news stripping away the oil premium that had been supporting CAD.

However, those gains have since been tempered. Crude has rebounded toward $97 and USD edged higher through Asian trading, leaving markets on edge this morning and highlighting just how fragile the truce remains.

Today

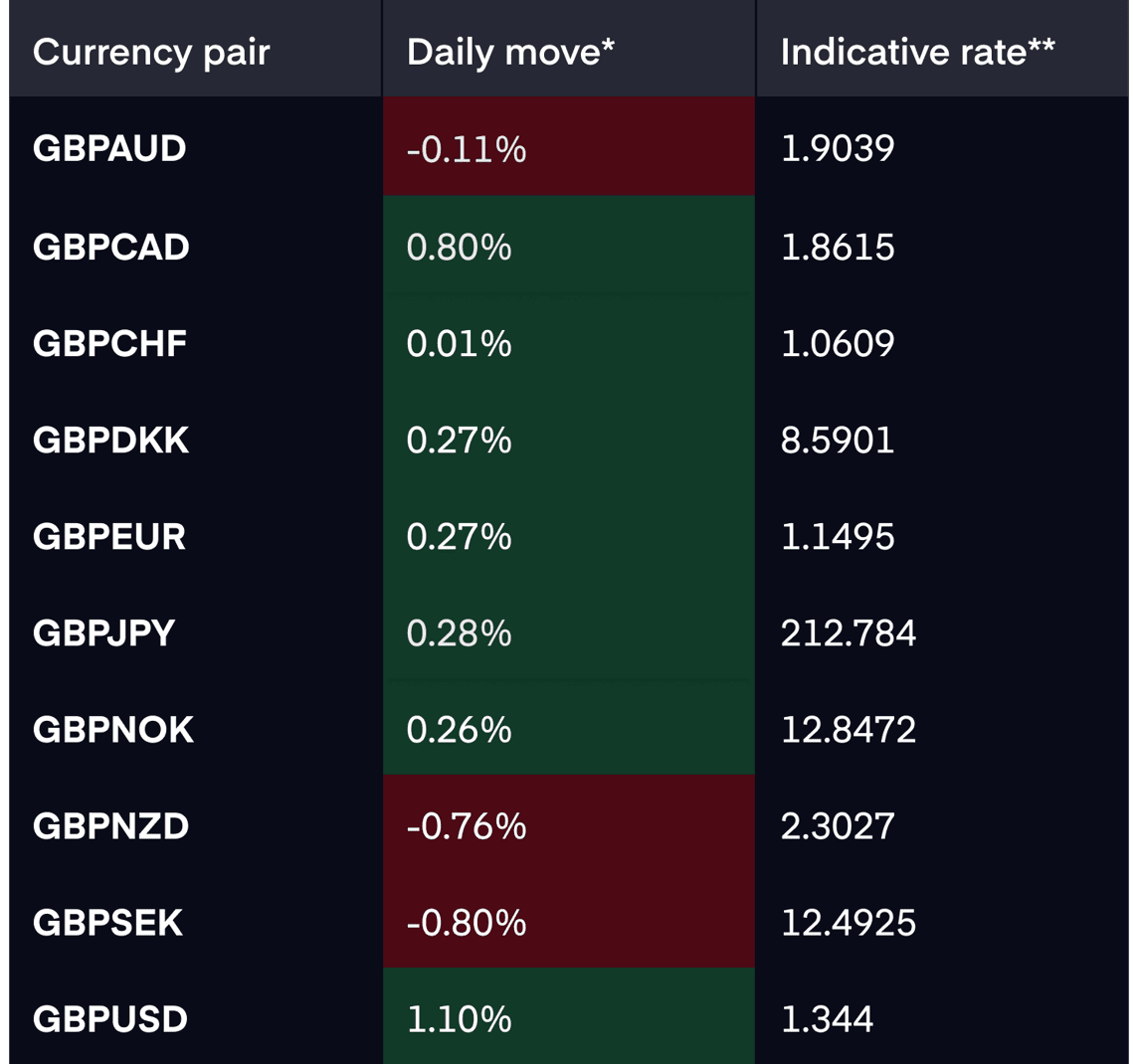

Market rates

*Daily move - against G10 rates as of 5pm BST on 08.04.26

** Indicative rates - interbank rates as of 5pm BST on 08.4.26

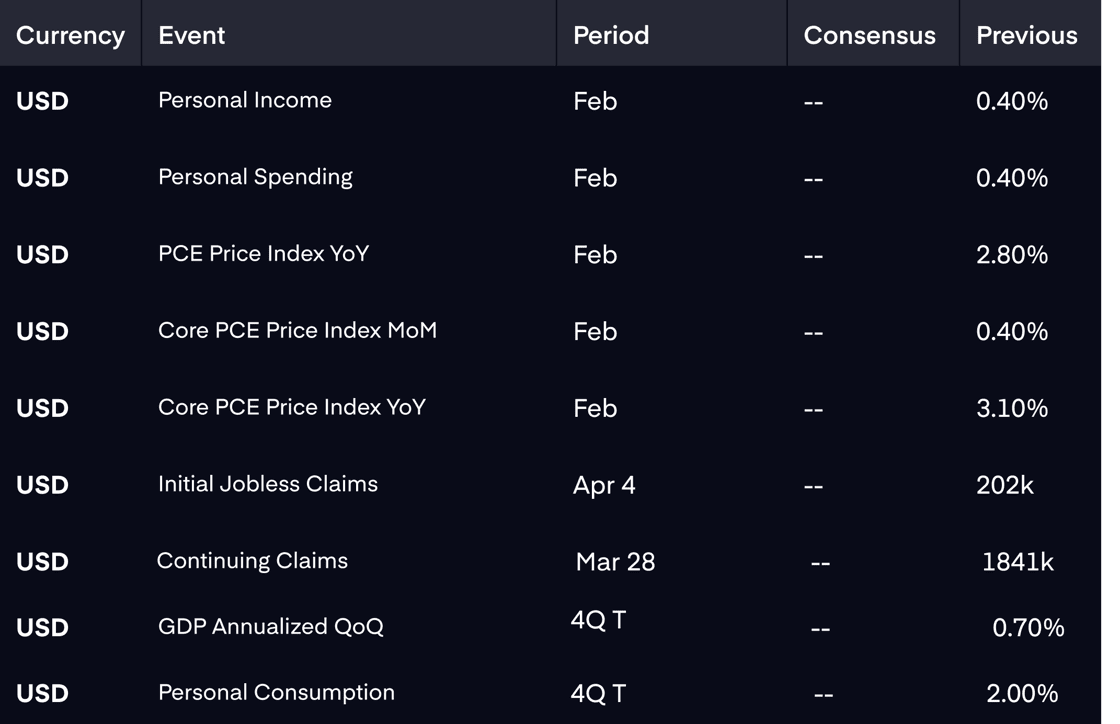

Data points

Click here for a calendar of upcoming economic events

Click here for a calendar of upcoming economic events Our thoughts

Today's session is dominated by US data.

Core PCE (the Fed's preferred inflation gauge) is expected to cool modestly to 3.00% YoY from 3.06%, which would offer some support to the rate cut narrative. Any upside surprise, however, would add fresh momentum to USD at a time when the geopolitical backdrop is already lending it support. Initial jobless claims are forecast to tick up to 210k from 202k – a modest deterioration but still historically low, and unlikely to move the needle significantly on its own. Q4 GDP is expected to be confirmed at 0.70% with no revision, making Core PCE the number to watch.

On the European side, German industrial production is forecast to rebound 0.65% after February's -0.50% contraction, which would offer EUR some modest support. That said, the single currency continues to face headwinds from diverging monetary policy expectations.

The dominant risk remains geopolitical. If the ceasefire deteriorates further, safe-haven flows will support USD, JPY and CHF at the expense of risk-sensitive currencies. Oil holding above $95-100 keeps inflation concerns very much alive and complicates the rate cut picture across G10. GBP has shown resilience, but with growth risks from the conflict mounting, any dovish signals from UK data or BoE policymakers could weigh on GBPUSD in the sessions ahead. Tomorrow's US CPI remains the week's defining release.

How we can help

Our team of currency experts are here to help you get more from your money when making international payments. We will work with you to understand your payment needs and offer specialised guidance on the best options available to you. Over the last 20 years we’ve helped over a million customers and last year alone processed over £12bn. We’re tried and trusted, and we’re ready to help you.

Get in touch with our team today on +44 (0)20 7778 7500 or email dealingdesk@equalsmoney.com.