MARKET REPORT

Dollar Tumbles as Japan Intervenes and Central Banks Signal Rate Hikes Ahead

To talk to us about your next trade, call 020 7778 7500 or hit the button below

Email us

- JPY surges 3% as BoJ and Japanese government confirm yen-buying operation after USDJPY breaches 160.

- BoE scraps central inflation forecast – all three scenarios point to rate hikes ahead as oil approaches worst-case levels.

Recap

It was a dramatic session dominated by Japanese intervention, central bank decisions and weak US data — all combining to deliver the USD largest single-day decline since April 17.

JPY was the standout performer, surging as much as 3% after the Japanese government and BoJ confirmed a yen-buying operation following USDJPY breaching 160. Finance Minister Katayama warned "the time is finally approaching to take the decisive action we have consistently signalled" – markets took notice immediately. USDJPY fell 2.3% – its biggest intraday advance in almost two years.

US data added further pressure on USD. Q1 GDP missed expectations whilst March PCE came in at 3.5% YoY – above consensus – alongside a Conference Board leading index falling 0.6%, well below all estimates. Weak growth and persistent inflation in the same print. Oil also retreated from earlier four-year highs, removing a key pillar of USD support.

The BoE held at 3.75% in an 8-1 vote but scrapped its central inflation forecast entirely – replacing it with three scenarios, all of which point to rate hikes ahead. Bailey's base case sees inflation peaking at 3.7% by year end. The most pessimistic scenario – which Bailey places "some weight" on – sees inflation hitting 6.2% in early 2027. GBPUSD rose 0.5%.

The ECB held at 2.00%, with Lagarde revealing a June hike was discussed "in depth" and signalling it remains firmly on the table. Eurozone Q1 GDP grew just 0.1% and April CPI accelerated to 3.0% – the fastest since autumn 2023. EURUSD rose 0.2%.

Today

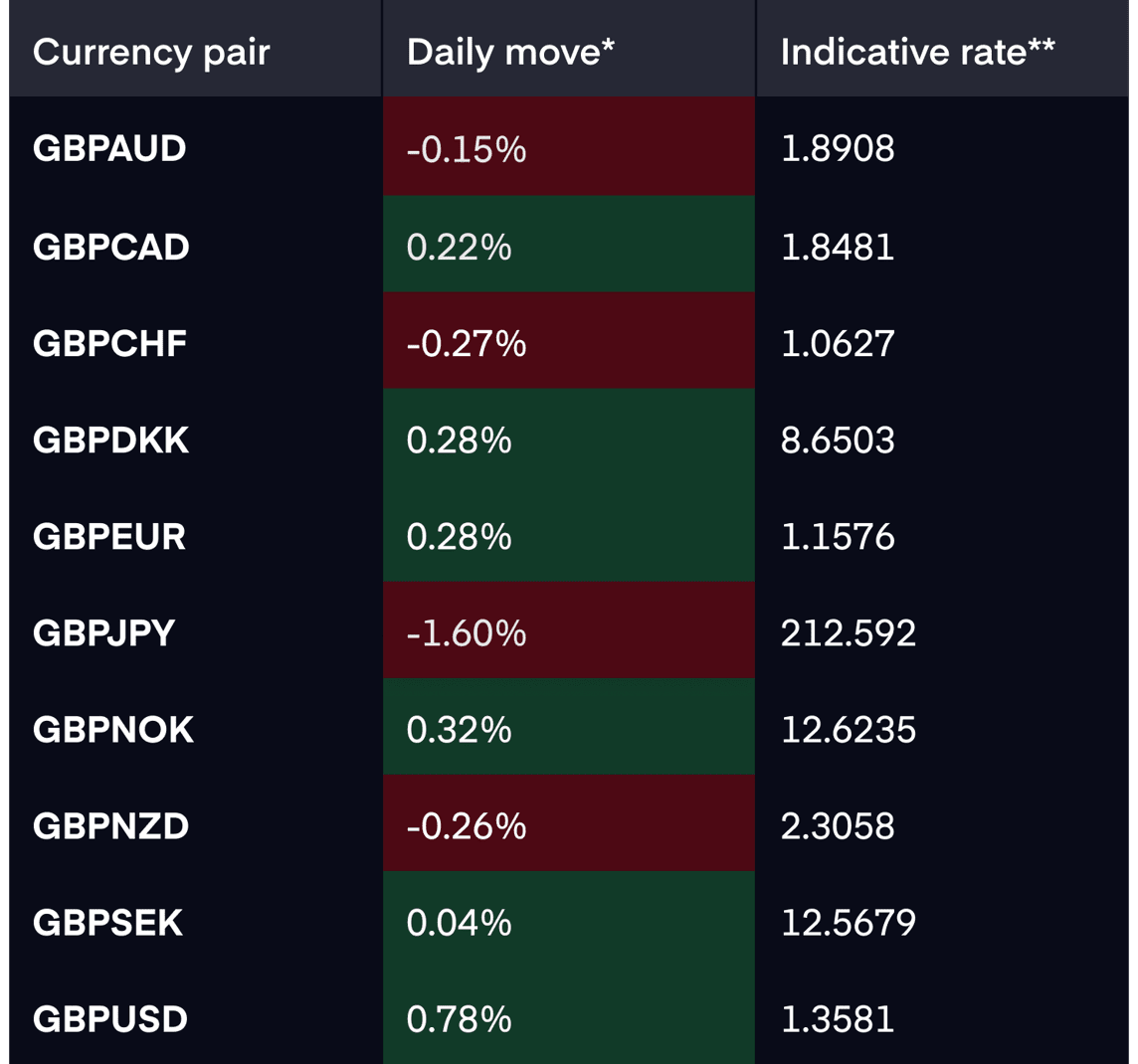

Market rates

*Daily move - against G10 rates as of 5pm BST on 30.04.26

** Indicative rates - interbank rates as of 5pm BST on 30.4.26

Data points

Click here for a calendar of upcoming economic events

Click here for a calendar of upcoming economic events Our thoughts

Today's session is relatively light on data, with US ISM Manufacturing the standout release. Consensus expects a modest improvement to 53.3 from 52.7 – continued expansion that would provide some USD support after yesterday's broad selloff. The ISM Prices Paid component is worth watching closely – forecast at 82 from 78.3, a hot reading would reinforce the inflation picture and complicate the Fed's already difficult position.

The dominant question for FX markets today is whether Japanese authorities follow through with additional intervention. Currency chief Mimura's warning that holidays won't prevent action signals officials remain on high alert – with Japan entering a holiday period next week, the risk of further JPY moves is elevated. USDJPY at current levels is a very different conversation to 160, but the pair remains sensitive to any shift in geopolitical or market sentiment.

For GBP, yesterday's BoE decision has set a hawkish tone heading into the coming weeks. With multiple MPC members signalling readiness to hike and all three inflation scenarios pointing higher, June is now a live meeting. GBPUSD at Aprils highs and GBPEUR at March highs reflect that repricing – UK mortgage approvals and the final manufacturing PMI print this morning are unlikely to shift the picture materially.

For EUR, Lagarde's clear signal that a June hike was discussed "in depth" gives ECB hawks a platform to build on over the next few weeks. With oil still elevated and CPI accelerating, EUR has fundamental support – though yesterday's modest reaction to the ECB decision suggests markets had already priced in much of the hawkish signal.

How we can help

Our team of currency experts are here to help you get more from your money when making international payments. We will work with you to understand your payment needs and offer specialised guidance on the best options available to you. Over the last 20 years we’ve helped over a million customers and last year alone processed over £12bn. We’re tried and trusted, and we’re ready to help you.

Get in touch with our team today on +44 (0)20 7778 7500 or email dealingdesk@equalsmoney.com.