MARKET REPORT

Iran Deal Collapses as Trump Rejects Tehran's Response

To talk to us about your next trade, call 020 7778 7500 or hit the button below

Email us

- Trump calls Iran's peace proposal "totally unacceptable"

- Oil up 3.1% as geopolitical tensions escalate overnight

- GBP under pressure as Starmer faces calls to step down

Recap

Last week was dominated by US-Iran geopolitical swings, central bank decisions, UK politics and a bumper US jobs report.

Oil was the week's defining variable, swinging from above $115 at the start to below $97 on US-Iran peace deal optimism, before recovering after US military strikes on Iranian targets overnight Thursday. Despite a volatile week, USD finished close to where it started, with robust non-farm payrolls overshooting expectations and renewed US-Iran military escalation partially reversing earlier losses into the weekend close.

JPY was the most volatile G10 currency of the week – Japan confirmed a record intervention campaign estimated at $65 billion to defend the yen after USDJPY breached 160, with suspected further operations later in the week keeping the pair on edge around the 157 level.

GBP showed mixed performance, outperforming North American currencies whilst underperforming against Scandinavian and Antipodean currencies that benefited from rate hikes. UK local election results proved devastating for Labour, with the party losing heavily across England, Scotland and Wales.

Both the Reserve Bank of Australia and Norway’s Norges Bank delivered rate hikes last week, with the RBA's third consecutive increase, now to 4.35%. The move reinforced the appeal of higher-yielding currencies, driving sustained AUD and NOK strength against GBP throughout the week.

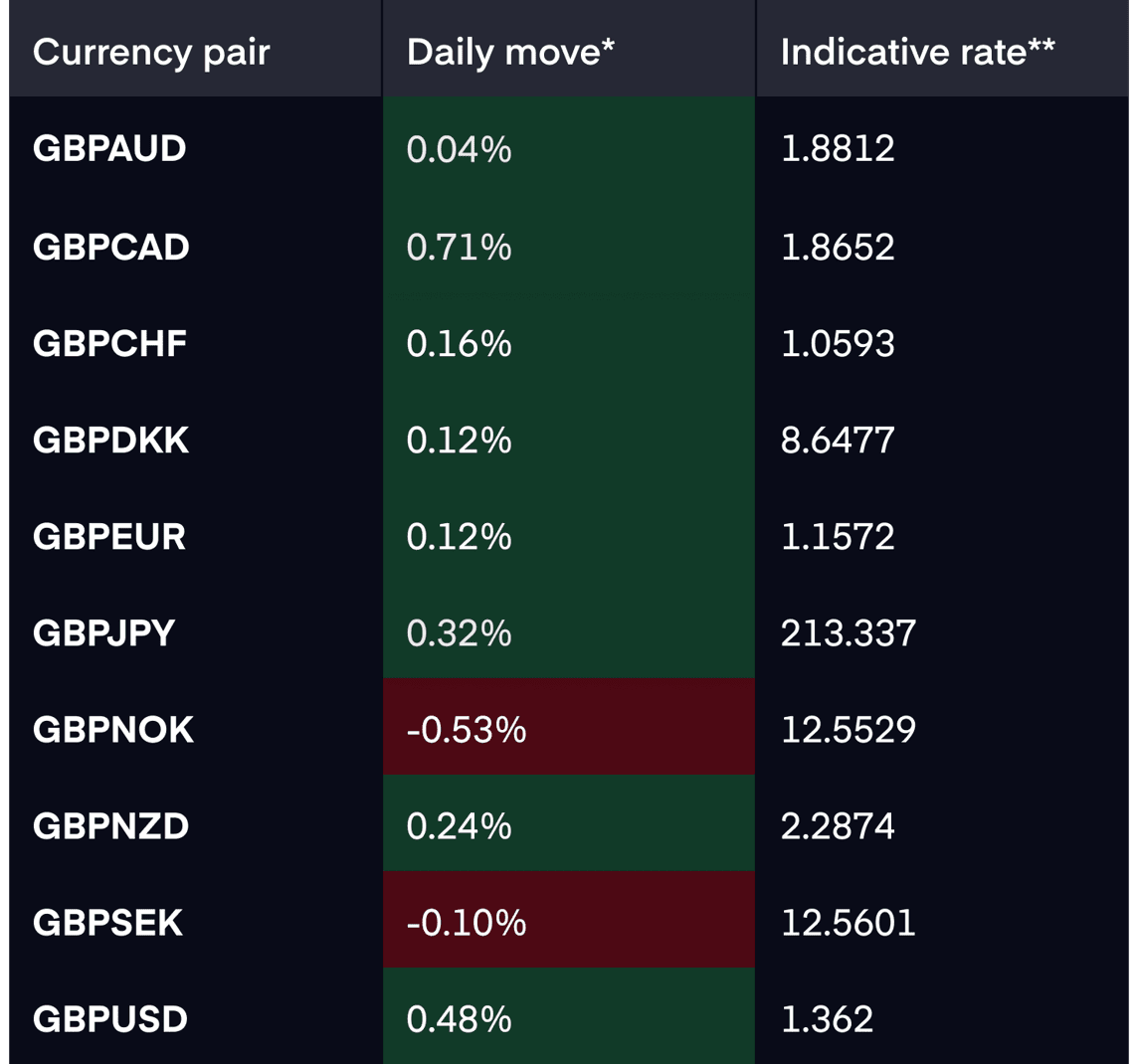

Today

Market rates

*Daily move - against G10 rates as of 5pm BST on 08.05.26

** Indicative rates - interbank rates as of 5pm BST on 08.05.26

Data points

Click here for a calendar of upcoming economic events

Click here for a calendar of upcoming economic events Our thoughts

USD is climbing this morning after Trump rejected Iran's peace deal response as "totally unacceptable". Iran had offered to transfer some enriched uranium to a third country but refused to dismantle its nuclear facilities. Oil is up 3.1% and GBP is among the biggest laggards as PM Starmer faces growing pressure to step down following the weekend's poor local election results.

Geopolitical tensions have escalated further after a drone strike set a cargo vessel ablaze off Qatar overnight and both the UAE and Kuwait intercepted hostile drones. Analysts are warning the risk of further escalation has increased significantly.

USD: CPI on Tuesday is the standout release this week US CPI for April prints Tuesday at 13:30 BST, headline expected at 3.7% YoY from 3.3%, with core at 2.7% from 2.6%. The key question is whether energy-driven price pressures are broadening into the wider economy. A hot print reinforces higher-for-longer and supports USD. PPI follows on Wednesday and retail sales on Thursday – expected to slow sharply to 0.5% from 1.7%.

GBP: UK GDP on Thursday is the key domestic release UK Q1 GDP prints on Thursday at 07:00 BST, with consensus at 0.6% QoQ – a strong improvement from the stagnation seen in the second half of 2025. A beat provides Starmer with some political respite, though higher energy costs are expected to squeeze growth through the rest of the year. A cabinet reshuffle and policy reset are expected, but whether that is enough to fend off a leadership challenge remains uncertain.

EUR: ZEW and GDP revision in focus. German ZEW expectations print on Tuesday is forecast to deteriorate further to -19.9 from -17.2. Wednesday brings the second estimate of Eurozone Q1 GDP, expected to confirm the 0.1% QoQ reading.

Geopolitics:US–China summit: the key wildcard this week. President Trump meets President Xi in Beijing on Thursday and Friday, a high-stakes engagement that could quickly be overshadowed by geopolitics if a US–Iran agreement is not secured beforehand. US Treasury Secretary Bessent is also meeting senior Japanese officials Monday through Wednesday, keeping JPY intervention risk in focus to start the week.

How we can help

Our team of currency experts are here to help you get more from your money when making international payments. We will work with you to understand your payment needs and offer specialised guidance on the best options available to you. Over the last 20 years we’ve helped over a million customers and last year alone processed over £12bn. We’re tried and trusted, and we’re ready to help you.

Get in touch with our team today on +44 (0)20 7778 7500 or email dealingdesk@equalsmoney.com.