MARKET REPORT

Oil Surge and Fed Split Drive Dollar Strength Amid Iran Tensions

To talk to us about your next trade, call 020 7778 7500 or hit the button below

Email us

Brent crude jumps 7% to $126 per barrel on reports of potential US military action against Iran - dollar strengthens broadly across G10

- Fed holds but records deepest policy split since 1992 - BoE and ECB both decide today alongside critical US PCE and GDP data

Recap

The Fed held rates steady on April 29 but delivered its deepest policy split since 1992 - eight members voting to hold, four dissenting - as oil-driven inflation risks increasingly cloud the economic outlook. Overnight, the situation escalated dramatically. Brent crude surged as much as 7.1% to $126.41 per barrel following reports that Trump is set to receive a briefing on potential military strikes against Iran, as negotiations to reopen the Strait of Hormuz remain firmly stalled. USD strengthened broadly.

EURUSD fell to two week lows heading for its third consecutive daily decline despite the ECB now priced for three rate hikes by year end. Spanish CPI came in hotter than expected at 3.5% YoY, adding to the inflation picture ahead of today's ECB decision. German CPI came in line with expecations at 2.9% YoY.

GBPUSD slipped to a week low with UK gilt yields briefly hit session highs after Greater Manchester mayor Burnham warned next week's local elections would be "challenging" for Labour adding the growing political risk premium on GBP. Worth noting that rising oil prices have driven markets to price in three BoE rate hikes this year - a significant hawkish repricing ahead of today's MPC decision.

The BoC held at 2.25% as expected with Macklem striking a hawkish tone on oil, warning persistently elevated energy prices could require consecutive rate hikes. Markets are now pricing 54 bps worth of hikes this year.

Today

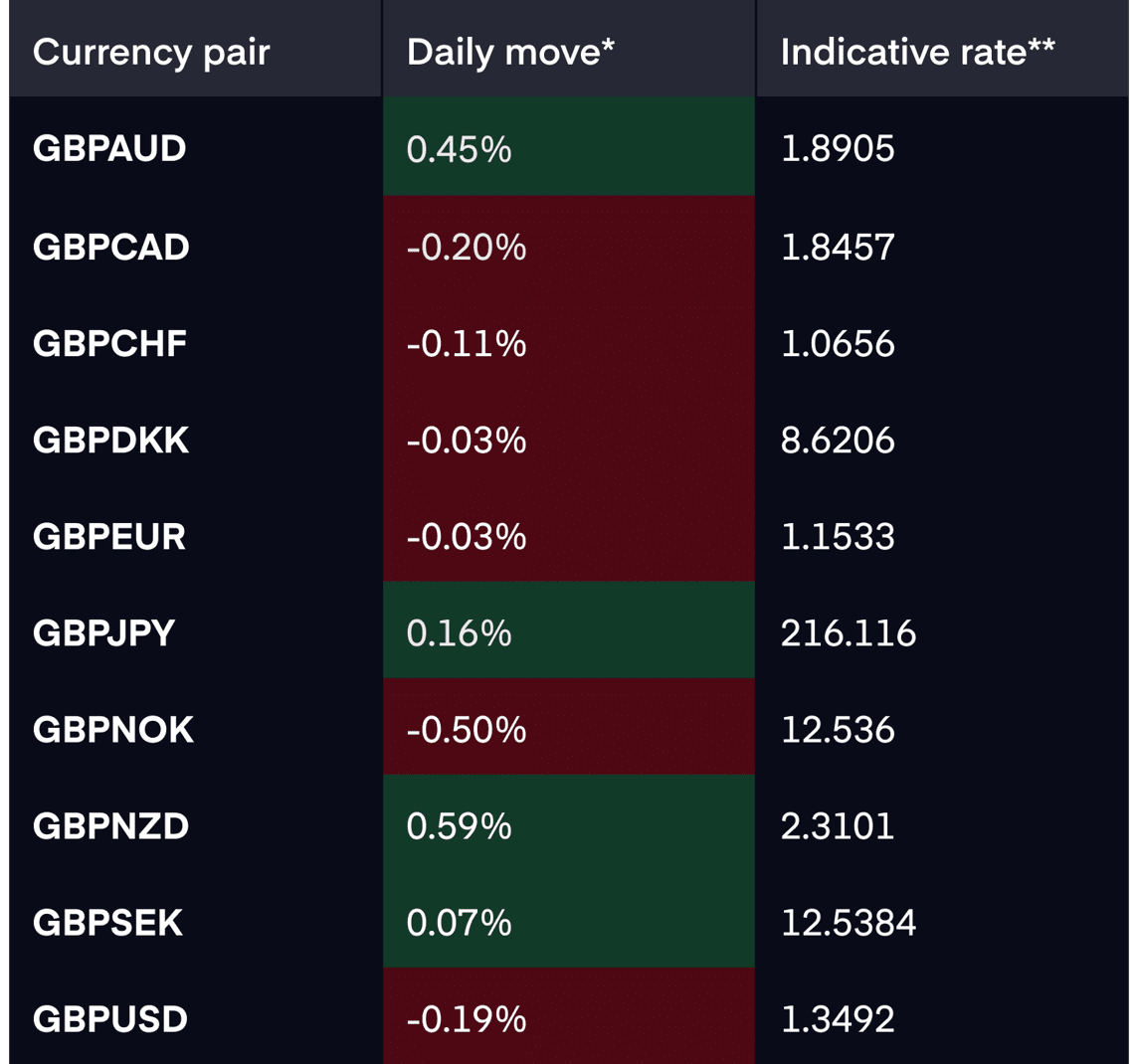

Market rates

*Daily move - against G10 rates as of 5pm BST on 29.04.26

** Indicative rates - interbank rates as of 5pm BST on 29.4.26

Data points

Click here for a calendar of upcoming economic events

Click here for a calendar of upcoming economic events Our thoughts

The US data is the immediate focus. Core PCE for Q1 is expected to surge to 4.1% from 2.7% - a dramatic acceleration that would significantly reinforce the Fed's hawkish dissent and provide further USD support. Q1 GDP is expected to rebound to 2.25% from 0.5%. If both print hot, the higher-for-longer narrative becomes very difficult to argue against and USD could move sharply higher across the board.

For the BoE, markets are pricing an 8-1 vote split with three hikes by year end. The tone of the statement and the MPC's new inflation forecasts will be everything for GBP - any acknowledgement that the oil shock warrants a more aggressive response would support GBP, whilst a cautious tone would quickly unwind recent hawkish positioning.

For the ECB, the risk remains that EUR falls sharply if Lagarde fails to commit to a June rate hike. Eurozone inflation data is due before the meeting and expected to show prices pressures reaccelerating - a strong reading would reinforce the case for the ECB to act and provide EUR with support going into the decision.

The dominant driver remains oil. With Brent at $126 and reports of potential US military action against Iran, the risk of further escalation is very real. USD is likely to remain well supported in this environment - the question is whether today's central bank decisions can provide enough of a hawkish signal to offset the safe-haven USD bid.

How we can help

Our team of currency experts are here to help you get more from your money when making international payments. We will work with you to understand your payment needs and offer specialised guidance on the best options available to you. Over the last 20 years we’ve helped over a million customers and last year alone processed over £12bn. We’re tried and trusted, and we’re ready to help you.

Get in touch with our team today on +44 (0)20 7778 7500 or email dealingdesk@equalsmoney.com.