MARKET REPORT

Sterling Steadies as Markets Brace for Central Bank Super Week

To talk to us about your next trade, call 020 7778 7500 or hit the button below

Email us

Five major central banks announce policy this week – Fed, BoE, ECB, BoJ and BoC all in focus against a backdrop of elevated geopolitical uncertainty and energy-driven inflation

- Iran offers new proposal to reopen Strait of Hormuz – dollar slips for a second consecutive session as haven flows recede

Recap

Two themes dominated last week – UK economic outperformance and the ongoing US-Iran conflict reshaping global FX.

The week opened with the Strait of Hormuz effectively shut, oil pushing toward $104 and USD supported on haven demand. Mid-week, Trump extended the ceasefire indefinitely, driving broad USD weakness – but the selloff was repeatedly interrupted by Iranian gunboat incidents and cancelled peace talks, keeping the geopolitical premium alive throughout.

The UK data story was a genuine positive surprise. PMIs smashed forecasts at 52.0 versus 49.8, retail sales beat, and BoE rate hike expectations repriced sharply to 61 basis points – markets now fully price two hikes this year. GBPEUR pushed to its best levels since March 27. The Eurozone told the opposite story – PMIs collapsed to 48.6, Nomura flagged stagflation risks, and ECB commentary turned increasingly divided.

GBP was the best performing G10 currency on Friday, gaining 0.36% against USD, with leveraged funds trimming bullish dollar bets for a second consecutive week.

This morning, the USD has slipped further following an Axios report that Iran has offered a new proposal to reopen the Strait of Hormuz. Market reaction has been more muted than previous headlines however, with some fatigue creeping into geopolitical-driven trades. Meanwhile, Kevin Warsh's confirmation as the next Fed Chair is advancing, with the Senate Banking Committee scheduling a vote on his nomination for April 29.

Today

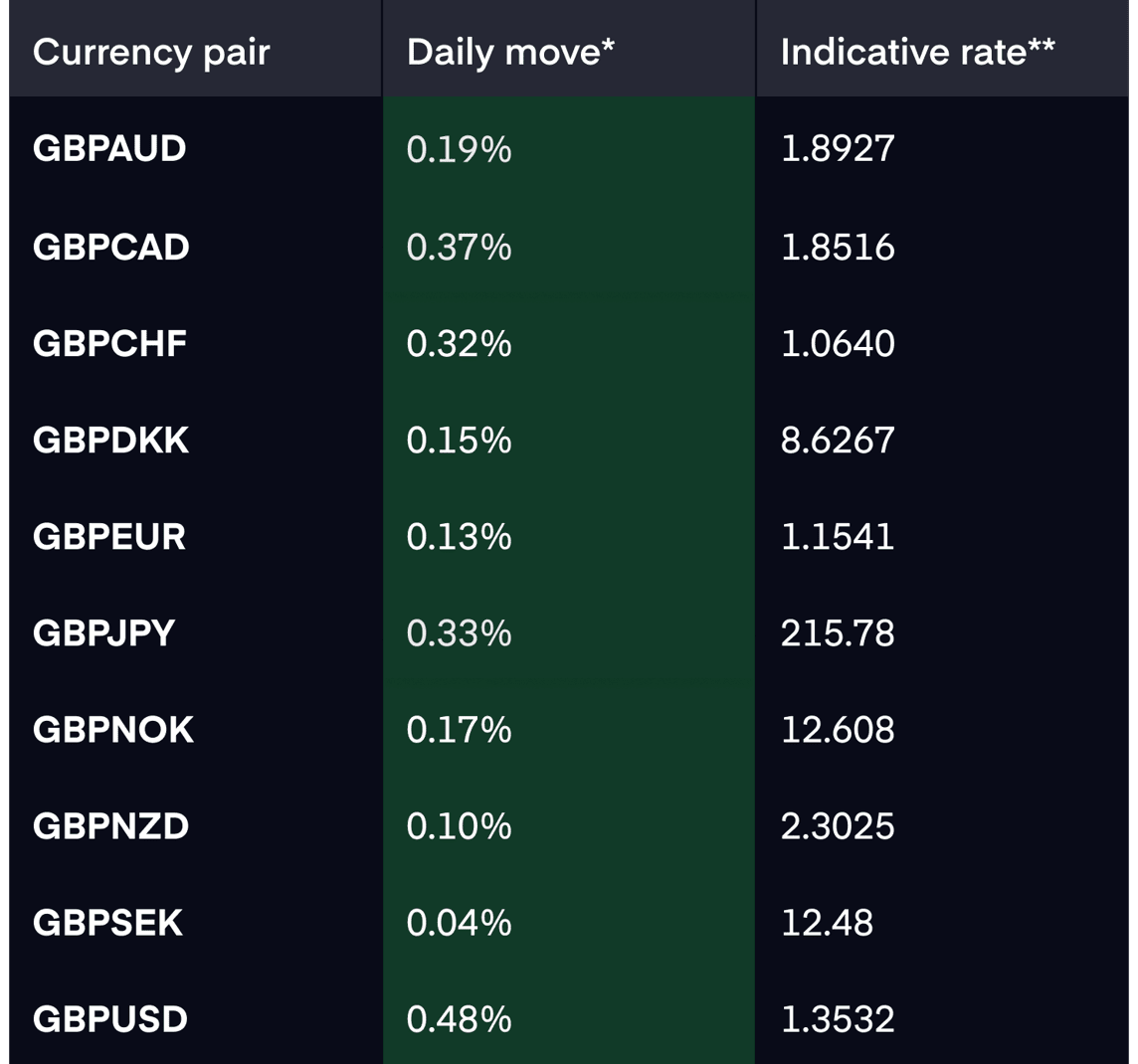

Market rates

*Daily move - against G10 rates as of 5pm BST on 24.04.26

** Indicative rates - interbank rates as of 5pm BST on 24.4.26

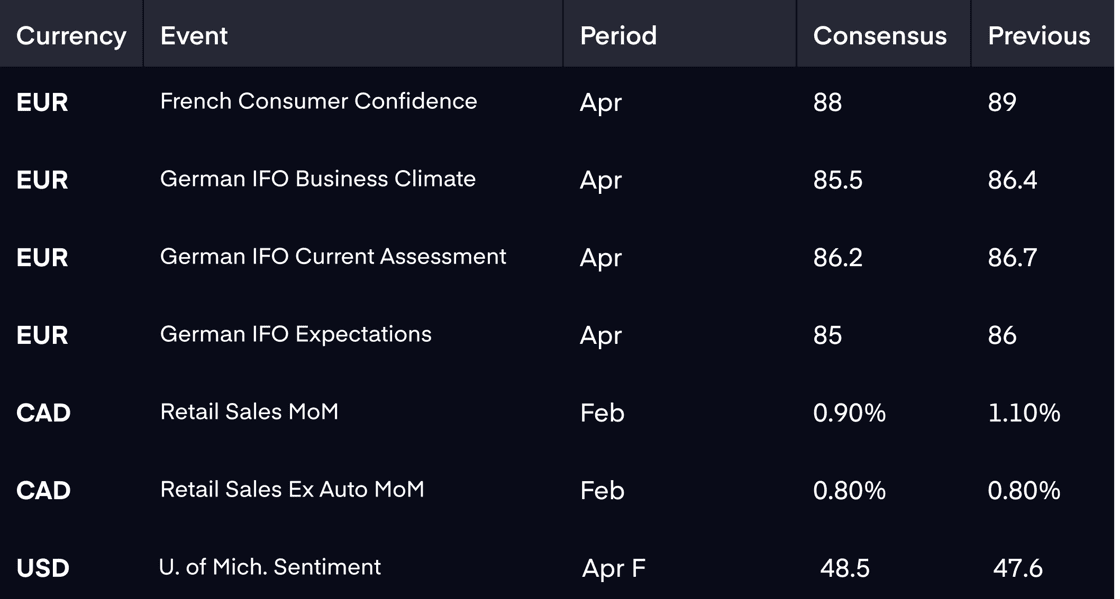

Data points

Click here for a calendar of upcoming economic events

Click here for a calendar of upcoming economic events Our thoughts

This is central bank super week – the BoJ, Fed, BoC, BoE and ECB all announce within 48 hours, making this one of the most concentrated periods of central bank firepower in recent memory.

Iran's new Hormuz proposal this morning adds a further layer of complexity to an already busy week. If the proposal gains traction and traffic begins flowing through the strait, haven demand for USD would recede further – a tailwind for GBPUSD and EURUSD. However, as the market reaction this morning suggests, traders are becoming increasingly fatigued by geopolitical headlines that have yet to deliver a lasting resolution.

The BoJ kicks things off Tuesday, expected to hold at 0.75%. With USDJPY near intervention levels, the setup is binary – dovish signals could trigger sharp JPY weakness whilst a hawkish tone could finally provide some support.

Wednesday is the main event. The Fed holds at 3.50-3.75% with Powell's press conference the key moment for USD direction. US housing and durable goods data also print. Australian CPI is Wednesday's wildcard – a jump to 4.8% YoY from 3.7% would put the RBA firmly back on alert and drive AUD strength.

Thursday is the busiest day. The BoE and ECB both announce alongside US Core PCE – expected at 3.2% YoY from 3.0%. An upside surprise would cement higher-for-longer expectations and send USD surging. US Q1 GDP also prints at 2.0% expected versus a prior 0.5% – a beat would add further USD support. For GBP, the BoE vote split and forward guidance will be everything after last week's data outperformance – any disappointment would quickly reverse recent GBP gains.

The bottom line – with central bank decisions, inflation data and GDP all converging this week, volatility is set to spike.

How we can help

Our team of currency experts are here to help you get more from your money when making international payments. We will work with you to understand your payment needs and offer specialised guidance on the best options available to you. Over the last 20 years we’ve helped over a million customers and last year alone processed over £12bn. We’re tried and trusted, and we’re ready to help you.

Get in touch with our team today on +44 (0)20 7778 7500 or email dealingdesk@equalsmoney.com.