just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

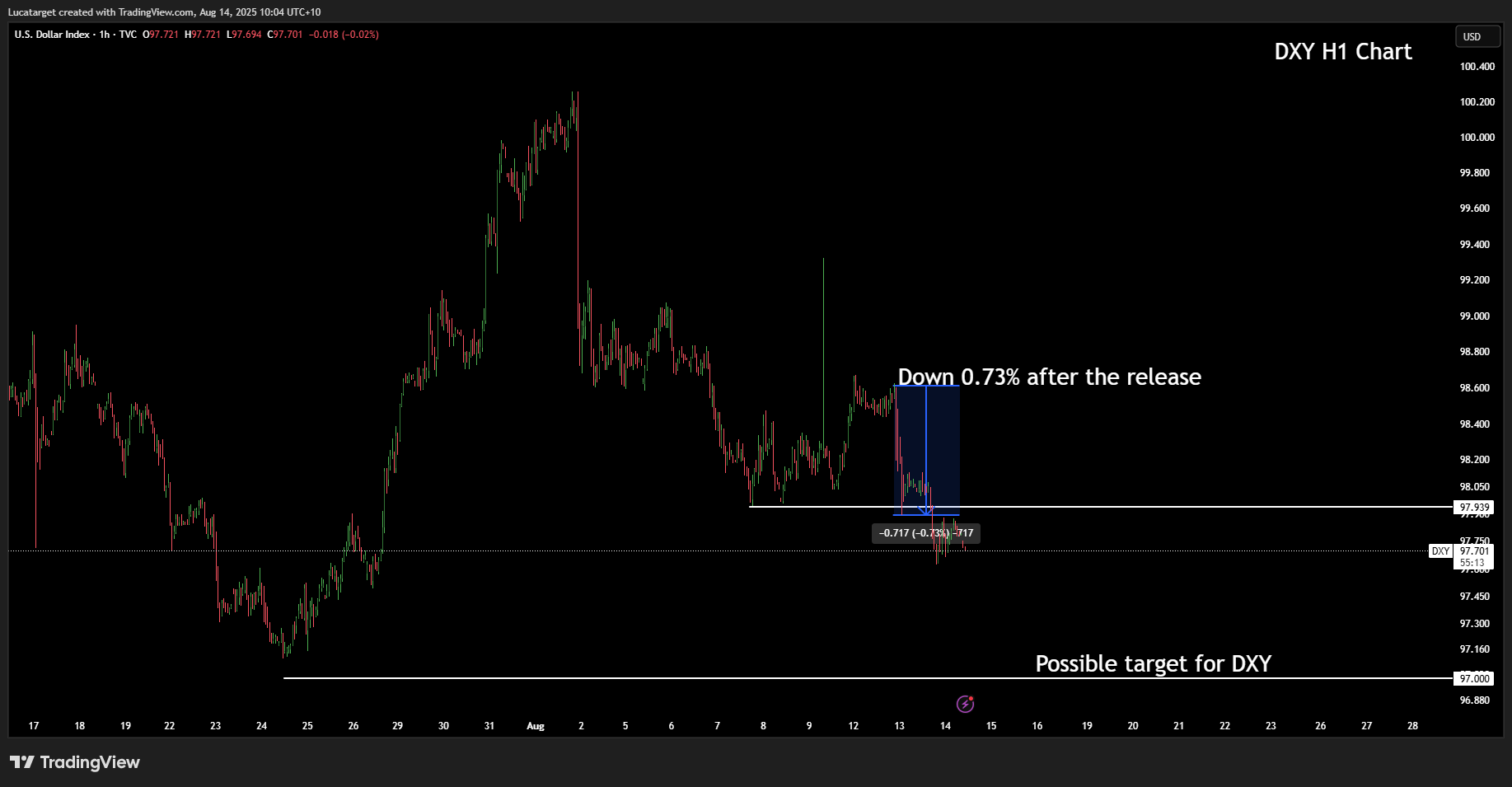

I woke up today with the same question everyone in FX space is asking now: does yesterday’s "in-line" US CPI meaningfully change the dollar’s path, or did it simply clear the way for the market to refocus on policy and politics?

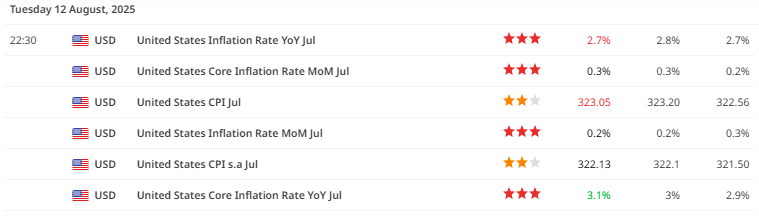

My base case is the latter. Headline CPI at +0.2% m/m and core at +0.3% m/m didn’t shock positioning; instead, it removed upside-inflation tail risk and put the spotlight back on the Fed’s reaction function and the political risk premium embedded in USD. That combination, policy glide path plus politics, will set the tone into the September FOMC.

From a market-mechanics standpoint, the immediate effect has been straightforward: softer US front-end rates, firmer rate-cut pricing into September, and another test of support on broad USD indices. When CPI lands in line, the market hunts for the second-order drivers: the labor data trend, the composition of inflation under the surface, and the degree to which the Fed can ease without reigniting price pressures.

This is where the micro details matter. Core goods (ex-autos) cooled again, while core services showed a firmer monthly print, with airline fares rebounding and medical services firming, offset by further easing in shelter. That mix supports a “disinflation, not deflation” narrative: enough deceleration to validate gradual cuts, not enough softness to force emergency easing.

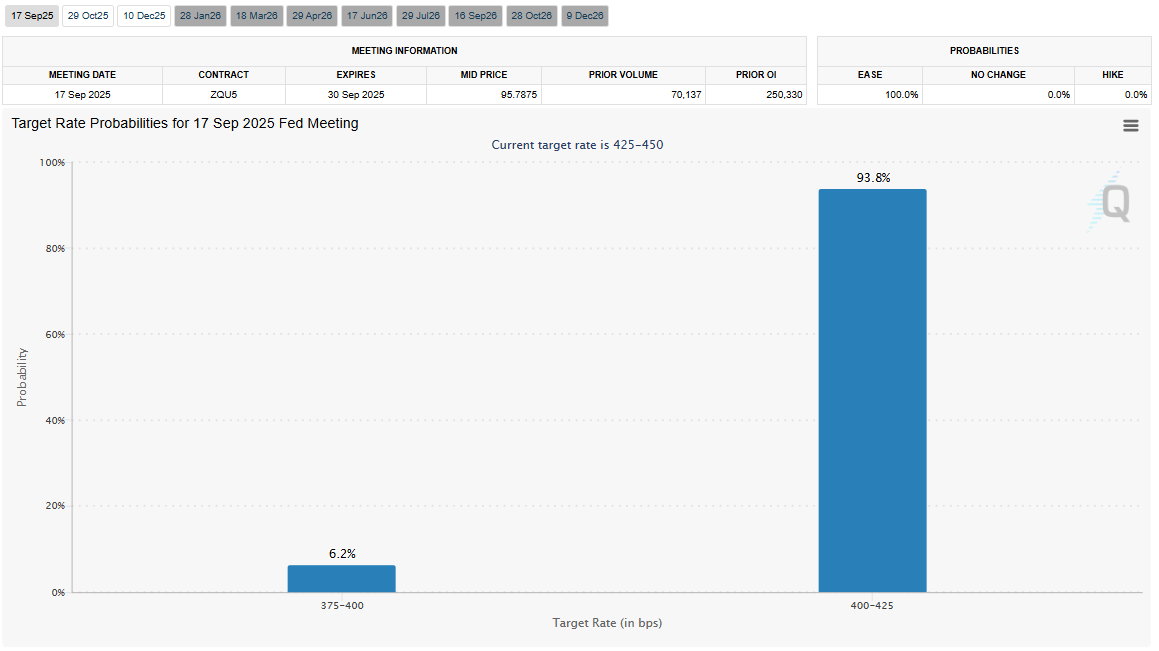

Policy communication risk is the second pillar. The market is now leaning toward at least a 25 bp cut by September, with scope for additional easing by year-end if labor slackening persists. What complicates the curve, and the dollar, are the political cross-currents around the Fed’s leadership and the data infrastructure (think: commentary about the BLS and the optics of personnel changes).

Regardless of one’s politics, the market reads these headlines through a single lens: institutional predictability. When predictability is questioned, the term premium on “policy noise” rises, and that can cheapen USD on a risk-adjusted basis even if macro prints are benign.

Where does that leave positioning? In my playbook, two things dominate the next two to four weeks:

First, the dollar as a funding currency. Implied volatility across G10 has drifted toward cycle lows, and carry is being rewarded again. That regime is fragile, it thrives on calm rates and narrow event risk windows, but while it persists, high-carry FX continues to attract flows at the dollar’s expense. I’m tactically respectful of that dynamic. I don’t need to love every carry expression; I just need to recognize that lower vol plus a clearer easing path is a tailwind for it.

Second, the composition of inflation. Shelter disinflation is doing work, but services ex-shelter is sticky. If September’s narrative is “growth cooling, inflation mixed, but trending lower,” the Fed has air cover to ease gradually. The risk to that story is a services-inflation surprise or a labor-market wobble sharp enough to re-price a larger cut in one meeting, which would shift the dollar’s reaction from “orderly drift” to “abrupt regime change.” I’m on watch for that asymmetry: benign data grinds USD lower; a downside labor shock cheapens the dollar faster; an upside services shock arrests the slide.

Tactically, here’s how I’m framing it for the days ahead:

I remain biased to sell USD strength into known supply zones rather than chase weakness. In practice, that means I prefer to fade relief rallies on US-centric headlines that don’t alter the rates path. The exception is if we get a credible upside surprise in services inflation proxies or a hawkish rhetorical pivot from key Fed speakers, particularly if it comes alongside a backup in front-end yields. In that scenario, I stand aside, because the market will quickly test whether the “carry + low vol” regime was over-owned.

Cross-sectionally, I’m selective. For higher-beta carry, I want confirmation from volatility: if front-end rate vol rises, I reduce exposure and favor quality carry (currencies with credible policy frameworks and cleaner external balances) over the highest nominal yields. Conversely, if vol stays muted, I’m comfortable letting winners run, but I rotate toward expressions with fundamental buffers, think pairs where disinflation is more advanced and current-account dynamics are not a headwind.

On the G3, I’m attentive to relative policy timelines. If the Fed leans into gradualism while other central banks are closer to terminal, or have already telegraphed a shallow easing path, the dollar’s cyclical premium can compress further without a dramatic macro shock. That doesn’t guarantee a one-way move, but it caps upside unless US growth materially re-accelerates. Put differently: without a growth surprise, the dollar needs inflation re-acceleration or policy hawkishness to sustain a durable rebound.

Risk management is the non-negotiable. This is a headline-sensitive tape, and the left-tail comes from politics as much as macro. I’m structuring exposure with optionality where possible, short-dated options financed by range trades in pairs I already like, so I can participate in the grind while being paid if the regime breaks. Into key speaker slots and data (Fed speakers, BoC deliberations, and the PCE deflator later this month), I scale, not swing. The goal is to be long convexity when the narrative changes, not after.

In-line CPI didn’t “save” the dollar; it removed a speed bump. The real drivers into September are (1) the credibility of a measured Fed easing path and (2) the market’s assessment of institutional predictability amid political noise. As long as volatility stays suppressed and the data allow the Fed to cut methodically, USD rallies are to be sold and carry remains supported. I’ll keep leaning into that regime, selectively, with tight risk, until the data or the policy signal tells me the story has changed.

Q1: How did the in-line US CPI print affect the USD?

A: The in-line CPI removed upside inflation tail risk and allowed markets to focus back on the Fed’s reaction function and political risk premium. This led to softer US front-end rates, firmer rate-cut pricing for September, and a test of support on broad USD indices.

Q2: Why is the Fed’s policy communication important now?

A: The market is leaning toward at least a 25 bp cut in September, but political noise and questions about institutional predictability can impact term premiums and risk-adjusted USD valuations, even without significant macro surprises.

Q3: What market dynamics are currently supporting USD weakness?

A: Low implied volatility and a clearer Fed easing path are encouraging carry trades, which are being funded partly by USD selling. This dynamic remains fragile and dependent on calm rates and narrow event-risk windows.

Q4: What are the main risks to the current USD drift lower?

A: A sharp services inflation surprise, a significant labor market downturn, or a hawkish Fed pivot could abruptly change the narrative, potentially ending the carry-friendly, low-volatility environment that is weighing on USD.

Q5: How is the current USD strategy framed?

A: The approach is to sell USD rallies into resistance zones while being selective in carry exposure. Positions are structured with optionality and scaled around key events to capture the grind lower while protecting against abrupt regime changes.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feedjust now

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.