Commodities 2026-04-29 10:20 5 minutes to read

Ole Hansen

Key points:

• Brent crude has rallied above USD 114 as the continued US-Iran blockade of the Strait of Hormuz prolongs a disruption that continues to tighten global energy markets

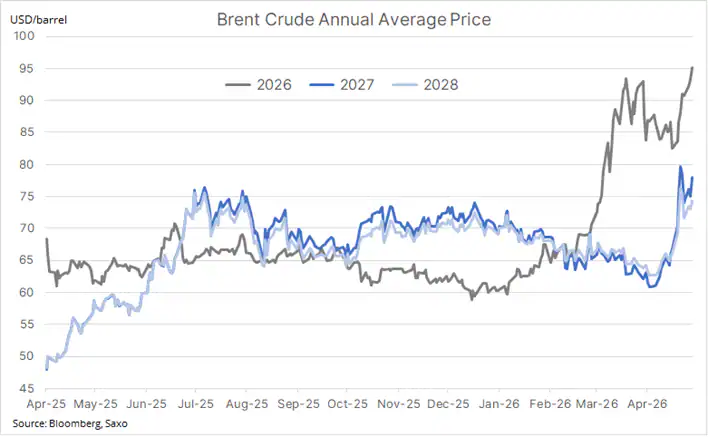

• The market is increasingly pricing a prolonged supply shock, with Brent’s 2027 annual average rising 25% over the past month and 2028 climbing 16%, signalling growing longer-term inflation risks.

• UAE's decision to leave OPEC from 1 May is unlikely to have a major short- to medium-term market impact, as depleted inventories and future reserve rebuilding demand should absorb additional barrels.

• Longer term, the exit raises questions about OPEC’s ability to manage supply and prices if more producers begin prioritising market share and capacity utilisation over quota discipline.

Crude oil has resumed its war-driven rally, with Brent rising almost non-stop since a brief mid-month tumble to USD 86, when hopes for a peace deal and a short-lived reopening of the Strait of Hormuz triggered a sharp but temporary correction. Since then, a renewed US and Iranian blockage of the strait has pushed prices sharply higher, with Brent now trading near USD 115 and heading for the highest daily close of the current cycle.

Brent crude trades near USD 115 - Source: Saxo

The near closure of the Strait of Hormuz continues to prolong a disruption that is steadily tightening global energy markets. With flows through one of the world’s most important oil arteries still severely restricted, traders are focused on the next steps in peace talks and today’s US inventory report for further signs of how quickly stockpiles are being drawn down amid robust export demand.

The market is no longer pricing the disruption as a short-lived front-month squeeze. While the 2026 Brent annual average has only edged higher over the past month to USD 95 per barrel, the bigger move has occurred further out the curve, with 2027 rising 25% to USD 78 and 2028 climbing 16% to USD 74. This points to growing expectations of a prolonged supply shock driven by damaged Middle East infrastructure, lower production capacity, and the eventual need to rebuild depleted commercial and strategic reserves.

Brent crude annual average prices for 2027 and 2028 has risen strongly in the past month - Source: Bloomberg & Saxo

Against that backdrop, the UAE’s decision to leave OPEC from 1 May marks a major strategic shift, freeing it from production quotas that for years limited its ability to fully utilise expanding capacity. In the short to medium term, the market should be able to absorb additional UAE barrels given depleted inventories and strong future reserve rebuilding demand. Longer term, however, the departure raises a broader strategic question: if more producers begin prioritising market share over quota discipline, OPEC’s ability to manage orderly markets through coordinated supply adjustments may increasingly be called into question.

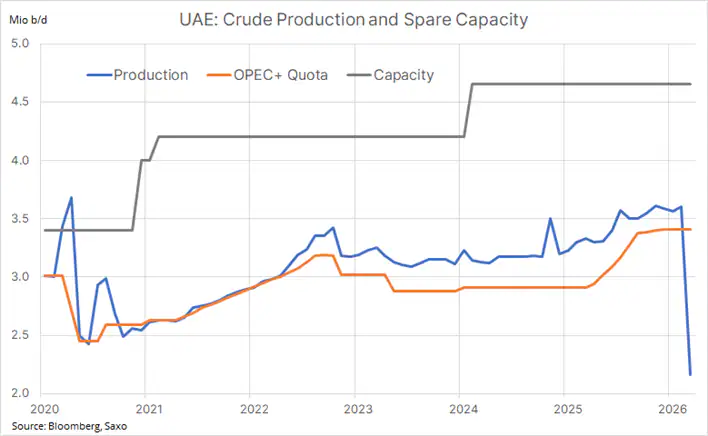

As per the chart below, UAE production reached 3.6 million b/d just ahead of the war before slumping by 1.44 million b/d last month to 2.16 million b/d, a 17-year low. It is also worth noting that, to the frustration of other members, the UAE has for several years produced above its OPEC quota. With its announced exit, the oil-rich nation can now pursue full utilisation of its expanding production base, with current capacity around 4.7 million b/d and a target of 5.0 million b/d through continued upstream investment led by ADNOC.

UAE production and capacity estimates - Source: Bloomberg & Saxo

This content is marketing material and should not be regarded as investment advice. Trading financial instruments carries risks and historic performance is not a guarantee of future results.

The instrument(s) referenced in this content may be issued by a partner, from whom Saxo receives promotional fees, payment or retrocessions. While Saxo may receive compensation from these partnerships, all content is created with the aim of providing clients with valuable information and options..