Taiwan Semiconductor Manufacturing Company delivered the blowout earnings investors had been waiting for.

However, the expected celebration did not follow.

TSM fell, and the contradiction offers the clearest update on the AI trade: investors still believe in the demand, but they are becoming less willing to pay as though today’s scarcity and margins will last indefinitely.

| Key takeaway: The market is not pricing an immediate collapse in AI spending. It is beginning to test how long chip scarcity can last, how much new capacity will cost, and whether customers can earn enough from the infrastructure they are buying. |

TSMC’s Q2 Revenue and Gross Margins

| Q2 revenue | Gross margin | Operating margin | Q3 revenue guide |

| $40.2bn | 67.7% | 60.3% | $44.6bn-$45.8bn |

Part of the profit increase came from a NT$63.2 billion disposal and mark-to-market gain on Vanguard International Semiconductor shares. The operating picture was still strong, with higher utilisation, 12% sequential revenue growth and a 65.4% annual increase in operating income.

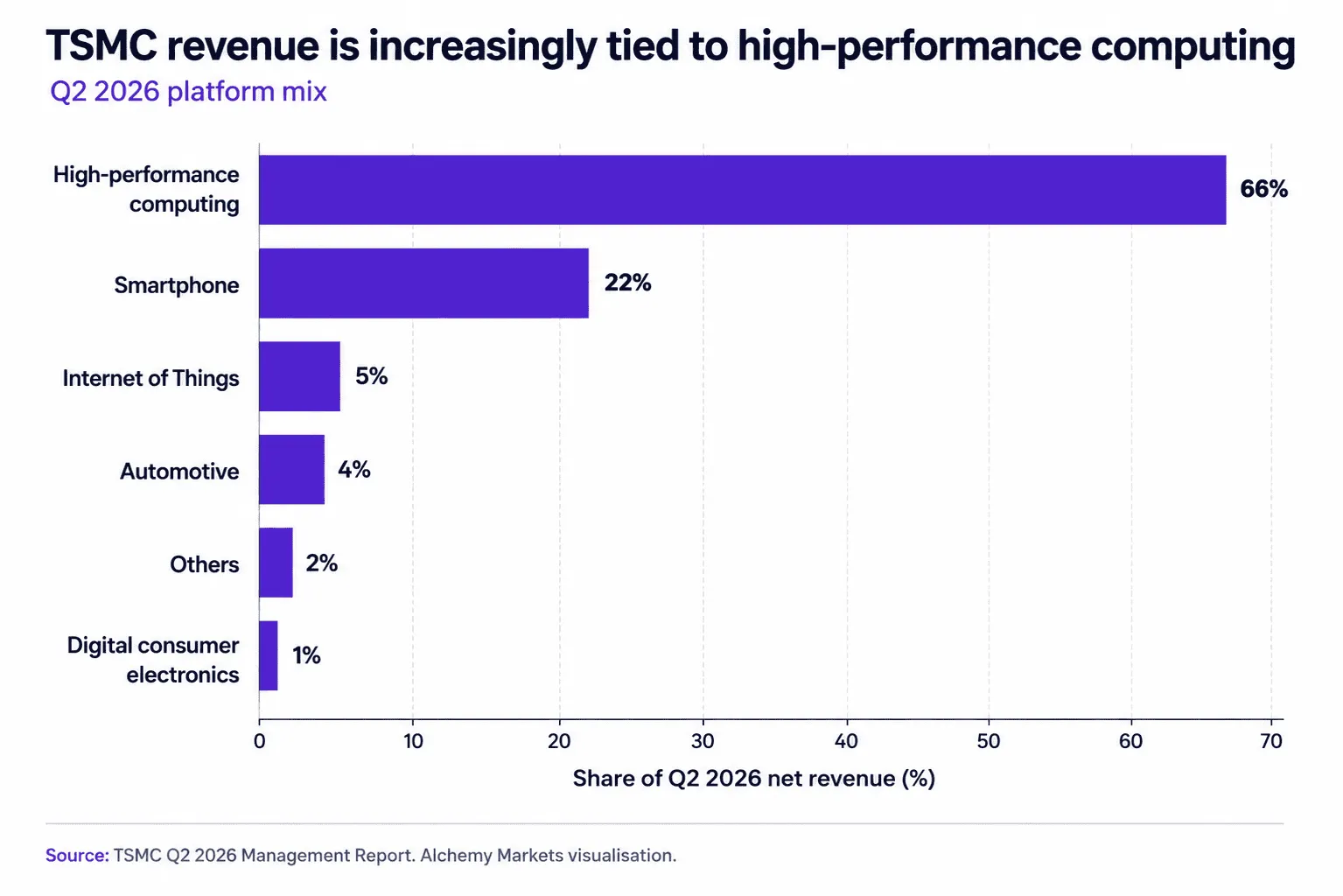

High-performance computing accounted for 66% of revenue, up from 61% in Q1. That concentration makes TSMC a more direct gauge of the AI buildout, but it also ties the valuation more closely to one demanding growth story.

Capital expenditure reached $15.7 billion during Q2 and $26.8 billion in the first half. Capacity is expanding because orders are strong, although free cash flow fell sequentially as investment grew faster than operating cash flow. Investors are therefore looking beyond sales and asking what return each new factory and packaging line will produce.

Sources: TSMC Q2 2026 quarterly results; TSMC Q2 management report; ASML Q2 2026 results.