just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

From my perspective, this was not about signaling a pivot or even a confirmation of policy success. It was about optionality.

The ECB is choosing to stay data-dependent, flexible, and strategically quiet heading into a summer that could significantly reshape the European macro landscape.

The latest data paints a nuanced picture. On one hand, short-term growth expectations have improved marginally.

Industrial production suggests that the eurozone may have skirted a deeper Q2 slowdown, and PMI releases point to some resilience as we step into the second half of the year. The manufacturing shows lot of resilience, as it stand in the 50 area.

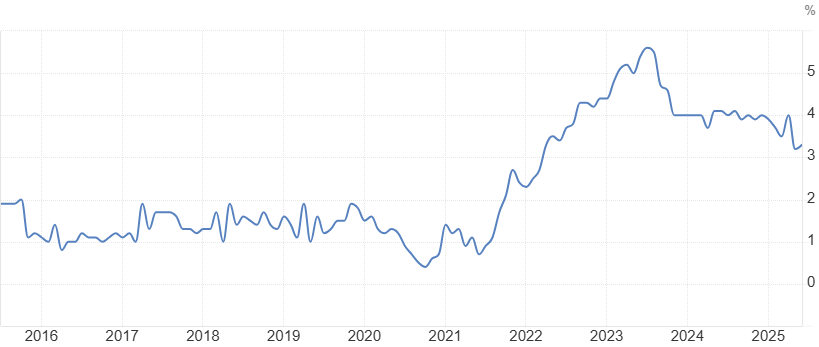

But on the other hand, there are visible cracks forming under the surface. Wage growth is softening. Labour market momentum is starting to cool.

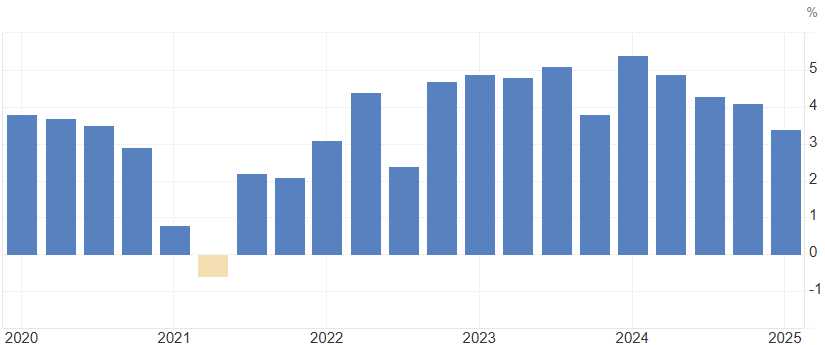

Services inflation once the stubborn outlier is also showing signs of easing. This isn’t the end of the inflation fight, but it’s a moment of recalibration.

One of the key narratives I’m watching is the potential for a trade agreement between the EU and the US.

While the ECB was quick to call current negotiations “conjecture,” markets are already starting to price in optimism.

If a deal is reached particularly one that caps reciprocal tariffs at or below the 15% mark being discussed it could reduce external uncertainty dramatically.

Why does that matter? Because trade friction has been one of the core variables driving risk premiums and growth revisions in the eurozone.

A resolution here could, in theory, provide just enough macro relief to delay or even eliminate further rate cuts. But let’s not get ahead of ourselves the durability and details of any deal will be critical.

The euro’s behavior has been fascinating. It started strengthening ahead of the ECB meeting and has largely maintained that momentum.

In my view, the lack of strong pushback from the ECB against euro strength says a lot. While President Lagarde noted they “monitor exchange rates,” it’s clear that the ECB isn’t particularly uncomfortable with current levels.

That said, a stronger euro can be a double-edged sword. On the one hand, it helps dampen imported inflation supportive of the disinflation narrative.

But on the other, it could make the ECB’s life more complicated if it triggers weaker export performance or premature tightening of financial conditions.

The balance is delicate, and it will only become more so if the euro breaks to new highs.

While the July decision felt like a non-event on the surface, the real inflection point will be in September. By then, we’ll have fresh data on wage growth, inflation, and potentially, the resolution (or escalation) of trade negotiations with the US.

Personally, I think policymakers are hoping to use the summer as a buffer letting the data speak while avoiding premature commitments.

If inflation undershoots and expectations keep drifting lower, the argument for at least one more cut remains strong. But a benign trade outcome could blunt that urgency.

To me, the ECB isn’t pivoting. It’s waiting. And that’s not a sign of weakness it’s strategic.

The risks ahead are still real, from potential supply chain disruptions to political volatility in the US.

But for now, the central bank appears content to let the current policy stance breathe, watching how the eurozone and the global economy navigates the next few months.

The next meeting may bring the clarity everyone’s waiting for. Until then, this pause is less about policy fatigue and more about creating space to reassess.

And in these markets, patience might just be the most powerful tool the ECB has left.

1. Why did the ECB kept the rates unchanged in July 2025?

The ECB paused its rate hikes primarily to preserve flexibility. Although inflation is easing and growth has shown modest resilience, the overall macro landscape remains uncertain particularly with ongoing trade negotiations between the EU and the US. The ECB maintained its data-dependent stance, choosing not to pre-commit before more evidence becomes available in the coming months.

2. What role do EU-US trade talks play in the ECB’s decision-making?

The potential for a trade agreement between the EU and the US is a key macro variable. If tariffs are capped at levels close to current assumptions (around 10–15%), that could reduce economic uncertainty and ease downside risks. However, the ECB isn’t factoring in an outcome just yet they’re waiting for official confirmation before adjusting the policy trajectory.

3. How has the euro reacted to the ECB’s latest announcement?

The euro has continued its upward trend, supported by growing optimism around a possible trade deal. Interestingly, the ECB didn’t push back hard against this strength. While President Lagarde noted the importance of monitoring exchange rates, the lack of strong resistance implies that current levels are not a policy concern at least for now.

4. What economic signals is the ECB watching most closely right now?

The ECB is closely monitoring wage growth, services inflation, and labour market conditions. Recent data suggests that domestic price pressures are easing and wage growth is slowing both of which support the disinflation narrative. These metrics, along with Q2 inflation and updated projections, will be key inputs for the September meeting.

5. Could we still see more rate cuts this year from the ECB?

Yes, but it depends on how the data evolves. If inflation continues to undershoot expectations and economic uncertainty remains elevated, another rate cut is likely. However, if a trade deal materializes and stabilizes the outlook, the ECB may scale back its easing path. As of now, markets are pricing in a very modest chance of additional cuts signaling growing confidence in a policy pause.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.