just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

The S&P 500 finally ran into the one thing equity bulls had been ignoring for weeks: the bond market.

Friday’s selloff was not driven by earnings weakness or a sudden collapse in AI enthusiasm. It was a repricing event caused by rising yields, renewed inflation fears, and a sharp move higher in oil prices. The clean macro chain driving markets was straightforward:

oil spike + inflation fears → Treasury yields surge → Fed hike odds rise → valuation pressure on growth stocks → SPX and Nasdaq sell off.

Markets had spent the last month aggressively pricing a “goldilocks” scenario where inflation cooled enough for the Fed to eventually ease while AI-driven growth continued to push equities higher. Bonds are now challenging that narrative.

As inflation concerns resurfaced, Treasury yields broke higher across the curve. The US 10-year yield climbed toward 4.60%, the 30-year pushed above 5.10%, and the 2-year also moved sharply higher. That combination signals the market is beginning to reprice both inflation risk and the possibility of tighter Fed policy later this year.

At the same time, crude oil surged as geopolitical tensions in the Middle East added another layer of inflation anxiety. Higher energy prices threaten to feed directly into future CPI readings, particularly after earlier inflation data already showed price pressures remaining sticky.

The result was classic multiple compression.

When yields rise, especially real yields, the discount rate on future earnings increases. That matters most for long-duration assets — mega-cap tech, semiconductors, software, and AI-related equities that had led the rally to record highs. Nasdaq underperformed because those sectors are the most sensitive to changes in rates.

There was also a positioning issue underneath the surface. Equity markets had become heavily concentrated in the AI momentum trade, and sentiment was extended. Once yields broke higher, traders quickly moved to reduce exposure in crowded growth names.

This is why the move matters beyond a simple one-day pullback.

The first-order reaction is straightforward: higher yields pressure equities. The second-order question is whether rising rates begin triggering broader de-risking across positioning, market breadth, and credit. If yields continue climbing while leadership deteriorates, the probability of a deeper SPX correction rises significantly.

For now, this still looks more like a rates shock than an earnings shock. But the bond market is now firmly back in control of macro pricing.

It is a relatively quiet week for US economic data, with the primary focus turning toward housing activity.

Housing starts data will provide another read on how elevated mortgage rates and affordability pressures are impacting the broader economy. The housing market remains one of the most rate-sensitive sectors, and current financing conditions continue to act as a major headwind for new construction and buyer demand.

If housing data weakens further, it would reinforce the idea that tighter financial conditions are beginning to slow growth more materially.

Markets will also closely watch the latest FOMC minutes.

The minutes are expected to reinforce the hawkish shift that emerged during April’s meeting, particularly after several Fed officials pushed for more neutral language regarding future rate cuts. Traders are increasingly focused on whether policymakers are becoming more concerned about inflation persistence rather than slowing growth.

With rate hike odds rising again, any indication that the Fed is uncomfortable with easing financial conditions could keep pressure on equities and bonds alike.

UK inflation will be the key international macro release next week.

Headline CPI is expected to dip slightly in April despite higher energy prices, largely because of temporary distortions tied to Easter timing and the absence of some regulatory price increases that boosted inflation last year.

Markets will also focus heavily on services inflation and wage-sensitive components of the report. Signs that wage growth is cooling and economic slack is increasing could support the argument that domestic inflation pressures are finally moderating.

If inflation comes in softer than expected, it may allow some Bank of England officials to become less concerned about second-round inflation effects stemming from the recent energy shock.

That would likely support expectations for eventual policy easing later this year.

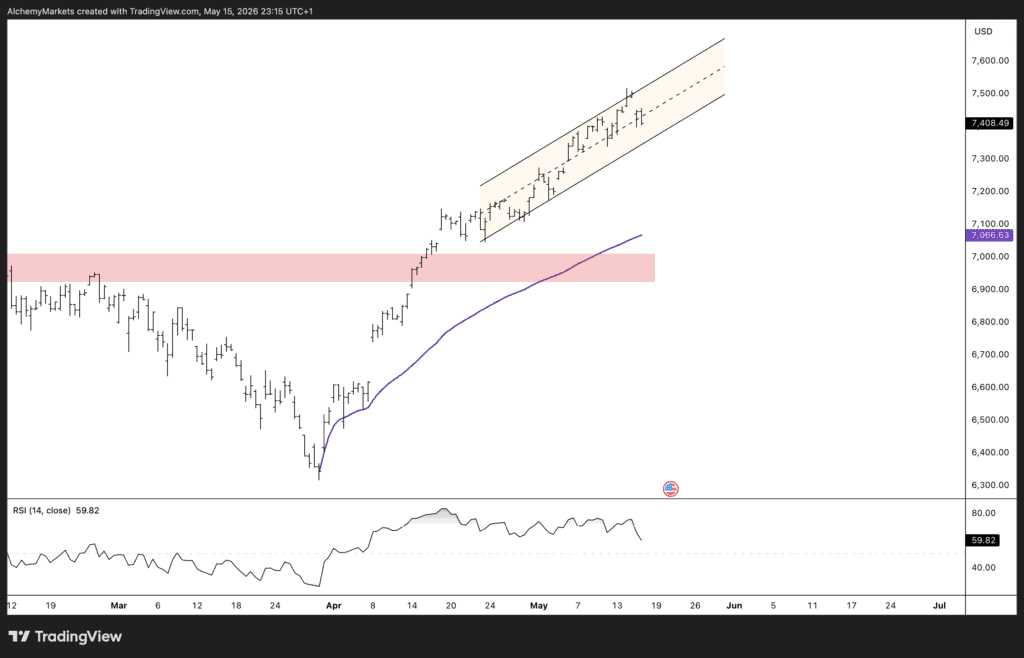

From a technical perspective, SPX remains trapped inside a well-defined rising channel following its sharp breakout above the 7000 region earlier in the quarter.

The problem for bulls is that momentum is beginning to stall precisely as macro conditions deteriorate.

Inflation concerns are returning, oil prices are pushing higher, and the bond market is now tightening financial conditions independently of the Fed. That creates a difficult backdrop for equities, especially after such an aggressive AI-led rally.

Price action is now respecting the upper and lower boundaries of the rising channel almost perfectly. Recent highs failed to generate strong continuation momentum, while RSI has also started to cool from elevated levels, suggesting upside momentum may be fading.

The key level to watch is the lower boundary of the channel.

If SPX breaks below that structure decisively, it would likely confirm that yields are beginning to overpower equity momentum. In that scenario, the market could quickly unlock a deeper correction back toward the 7000 region, which now acts as a major psychological and structural support zone.

Technically, 7000 is important because it aligns with:

As long as SPX holds inside the channel, bulls still maintain control of the broader trend. But the margin for error is narrowing.

The market is no longer trading purely on AI optimism.

It is trading on whether yields continue rising faster than earnings expectations can compensate.

That makes the bond market the most important chart in the world heading into next week.

Alchemy Markets is a multi-asset brokerage providing retail traders with the same elite trading conditions, tools, and transparency typically reserved for institutions.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.

Want to master the markets? A winning trading mindset beats a perfect strategy. Learn how emotional discipline helps you conquer fear and avoid heavy losses.