just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

Over the past two weeks, markets have aggressively shifted back toward a more hawkish central bank outlook.

The catalyst has been straightforward:

Only a few weeks ago, markets were confidently pricing multiple rate cuts for later this year. Now, expectations have shifted materially higher, with cuts being pushed further into the future and some traders even reopening the discussion around additional tightening risks.

But the key question heading into this week is whether markets are reacting to the right inflation driver — or potentially overestimating the persistence of this latest energy shock.

The current market narrative assumes that higher oil prices automatically translate into broader inflation pressure and therefore force central banks to remain restrictive for longer.

That logic makes sense on the surface.

However, this environment still looks materially different from the 2022 energy crisis.

Back then, the inflation shock was not driven by crude oil alone. Europe experienced a full-spectrum energy crisis as:

That broader energy transmission mechanism created persistent inflation pressure across nearly every sector of the economy.

This time, however, the picture is more contained.

While crude oil prices have moved sharply higher due to geopolitical tensions, natural gas prices remain relatively stable compared with the extreme levels seen in 2022.

That distinction matters enormously for central banks.

Policymakers are not simply reacting to oil prices in isolation. What they care about is whether higher energy prices begin feeding into:

So far, that transmission effect still appears limited.

At the same time, several underlying economic indicators continue pointing toward slower growth conditions beneath the headline data.

The US labour market still appears resilient at first glance, but internally the picture is becoming less convincing.

Several softer trends continue developing:

This creates an important divergence in market expectations.

Right now:

focuses on:

suggests:

That tension will likely define market direction over the next several months.

The Bank of England is facing many of the same concerns.

Markets have aggressively repriced UK rate expectations higher because Britain remains highly sensitive to energy shocks.

But again, the current backdrop differs significantly from 2022.

Natural gas prices have not experienced the same type of parabolic move that previously triggered the broader UK inflation spiral.

That weakens the argument for the Bank of England needing to tighten aggressively again.

If inflation expectations remain relatively anchored while growth continues slowing, markets may eventually need to reverse some of this hawkish repricing.

The biggest macro question now is whether this latest oil surge becomes:

or

That distinction will likely determine:

If inflation expectations remain contained, central banks may tolerate temporarily elevated oil prices without tightening further.

But if energy prices remain elevated long enough to impact consumer behaviour and inflation psychology again, markets may ultimately be correct to expect a more hawkish policy path.

Markets are expecting another strong headline inflation print.

The primary drivers are expected to be:

However, the broader view remains that this inflation acceleration may still prove temporary if underlying demand conditions continue weakening.

The critical market focus will be whether inflation broadens beyond energy-related categories.

Retail sales may appear stronger at the headline level primarily because gasoline prices mechanically boost nominal spending figures.

However, underlying discretionary demand may remain softer.

Potential areas of weakness:

Markets will watch closely for signs that consumers are beginning to pull back under higher financing costs and slower income growth.

Industrial production is expected to rebound modestly, helped by continued strength in manufacturing activity and stabilization within supply chains.

The ISM manufacturing data has recently shown signs of resilience, though broader industrial momentum still remains mixed.

One of the most important developments this week is political and symbolic.

Jerome Powell enters his final days as Federal Reserve Chair before Kevin Warsh officially takes over on Friday, May 15.

Markets will be closely monitoring:

Any signal that the incoming leadership may tolerate higher inflation or prioritize growth stabilization differently could materially impact yields, equities, and the dollar.

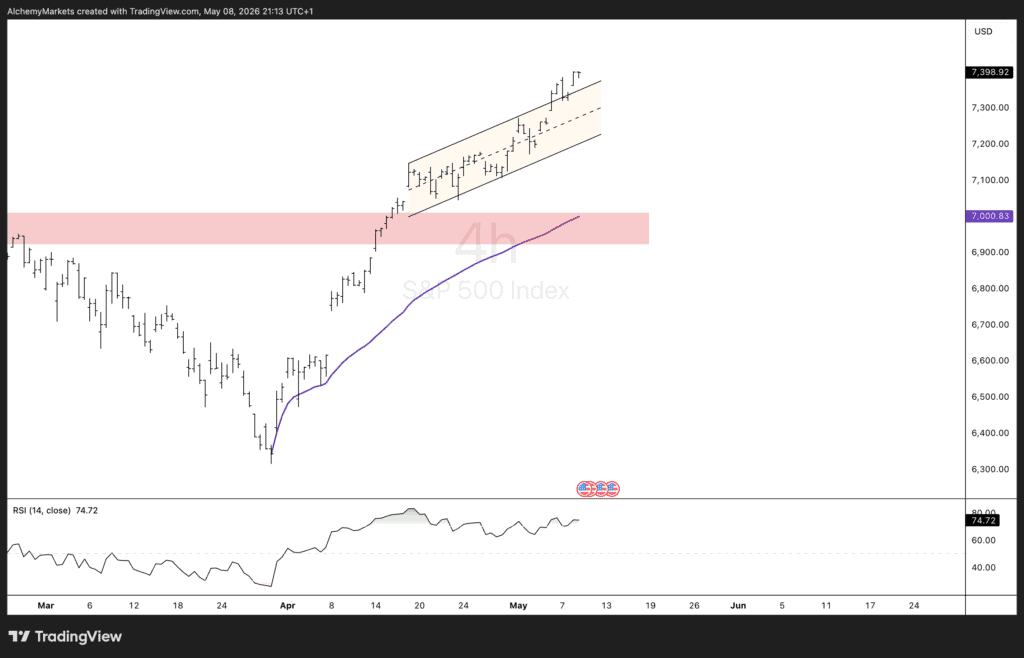

The SPX continues trading inside a strong ascending channel structure on the 4-hour timeframe, with momentum remaining firmly bullish despite increasingly overbought conditions.

The index has now broken significantly above prior resistance and continues respecting higher lows while riding above anchored VWAP support.

RSI remains elevated near overbought territory, reflecting strong momentum but also increasing sensitivity to any macro disappointment.

The bullish case remains structurally intact as long as:

Under this scenario, markets may conclude:

Technically, the chart structure still favours continuation higher.

The ascending channel remains intact, and buyers continue stepping in at shallow pullbacks.

If momentum persists:

A softer inflation interpretation this week could act as another catalyst for upside continuation.

The bearish risk emerges if markets begin believing this oil shock is evolving into a broader inflation regime shift.

That would likely require:

Under that scenario:

Technically, the market is already extended.

RSI is elevated, positioning is increasingly crowded, and price is trading near the upper boundary of the channel.

If a correction develops, the first major downside area becomes:

This zone aligns closely with:

The anchored VWAP currently acts as a critical institutional support area.

A clean hold there would likely preserve the broader bullish trend structure.

However, if price loses both:

then a deeper corrective phase could begin as momentum positioning unwinds.

Markets are entering a critical macro phase where the debate is no longer simply about inflation.

The real debate is whether:

That distinction will drive:

For now, SPX remains technically bullish — but increasingly sensitive to macro data surprises and inflation expectations.

This week’s inflation data and central bank communication may determine whether the rally extends further or finally enters a corrective phase.

Alchemy Markets is a multi-asset brokerage providing retail traders with the same elite trading conditions, tools, and transparency typically reserved for institutions.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.

Learn what Blockchain-as-a-Service is, how it works, and why businesses are using BaaS to build blockchain applications without managing infrastructure.

CFDs vs stocks compared on leverage, ownership, costs, dividends, taxes, and risk. Learn the differences between stocks and CFDs and discover which suits your investing or trading goals.