just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

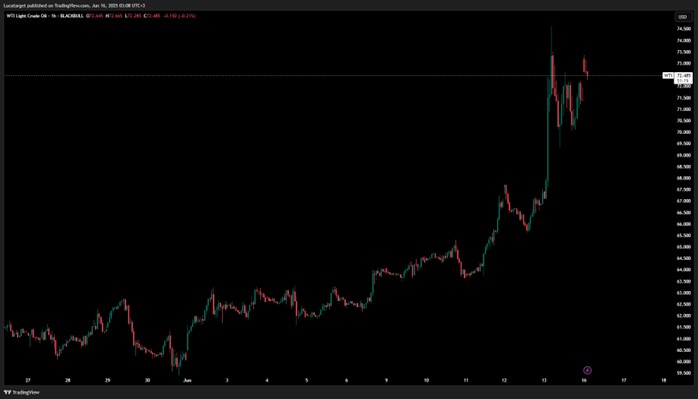

The currency market has been thrown into disarray after Israel launched a wave of coordinated airstrikes on Iran’s nuclear and ballistic missile infrastructure a move that marks the most dangerous escalation in the region in years. Within minutes, Brent crude spiked over 11% before partially retracing, and traders rushed out of risk assets and into havens.

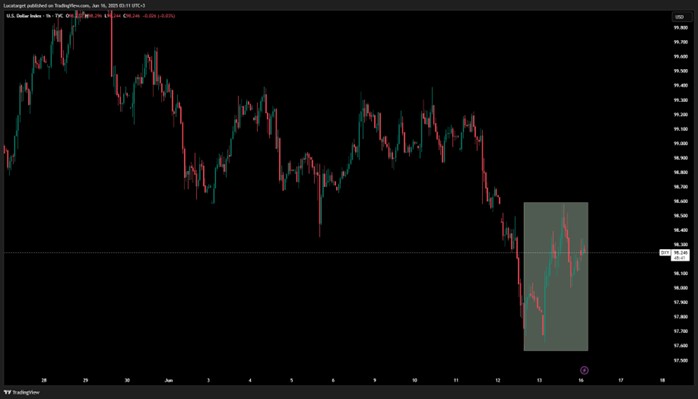

The surge in oil reversed all its losses since April when Trump’s new tariffs were first announced, snapping back above $74 before settling near $71. Meanwhile, the Swiss franc, yen, and US dollar were the prime beneficiaries of the classic risk-off play. High-beta FX like the AUD, NZD, ZAR, and MXN were punished, particularly as carry trades unwound aggressively heading into a very uncertain weekend.

From a geopolitical standpoint, things are still unfolding quickly. Netanyahu has promised continued strikes "as long as necessary," while Iran has already retaliated with over 100 drones and is promising much more. The situation has the potential to deteriorate into a wider regional conflict, and with Iranian nuclear enrichment back in the spotlight and nuclear deal talks already looking shaky this isn’t going to de-escalate quietly.

For the USD (DXY), the timing couldn’t be more interesting. Just before the missiles flew, the greenback was plumbing new year-to-date lows, driven by weak US CPI and PPI data, softening labour market prints, and growing calls for the Fed to cut. But geopolitical risk trumps everything in the short term. Now, the dollar is back in demand, even as macro headwinds remain.

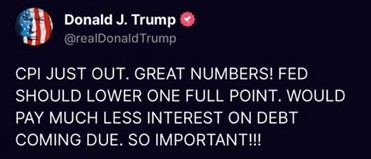

President Trump has doubled down on his pressure campaign against the Fed, calling for a two-percentage-point rate cut (up from his previous demand of one). His argument? Lower rates would ease US debt burdens by $600 billion annually. The real pressure point, however, is political: the Fed now faces a credibility test if Trump names a new chair nominee ahead of Powell's 2026 exit, as markets will have to gauge not just policy, but politics.

On that front, rate cuts still look unlikely in the very near term. While inflation is softening core PCE likely rose just 0.1% in May policymakers remain cautious due to trade uncertainty and rising energy costs. Labor market data is sending mixed signals: continuing jobless claims are now at their highest since November 2021, and while it’s not yet a trend, it could become one fast.

Across the Atlantic, the UK economy is cooling sharply. After a surprisingly strong start to 2025, GDP shrank 0.3% in April the worst print since late 2023 driven by a reversal in trade and distortions in domestic spending (think car sales and stamp duty-related activity). With front-loaded US demand fading, UK exports to the US fell by £2 billion in a single month.

Labor market slack is also building. Payroll employment is dropping, vacancies are down across sectors, and wage growth is easing. The BoE will likely stick to its quarterly easing cycle come August, but the risk now is that energy shocks from the Middle East delay disinflation progress. The government’s fiscal headroom is minimal, and tax hikes are almost certainly on the way if growth disappoints or the geopolitical crisis worsens.

This is one of those moments where geopolitical risk and macro fragility collide. The USD may have found a temporary floor thanks to war premiums, but with softer inflation and labour data still piling up, markets will have to choose which narrative dominates safety or stimulus.

Carry trades are vulnerable, risk assets are fragile, and oil volatility is now the wildcard. We’re heading into the weekend with tension rising in both Tehran and trading desks.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS Feed

just now

Sign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.