just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

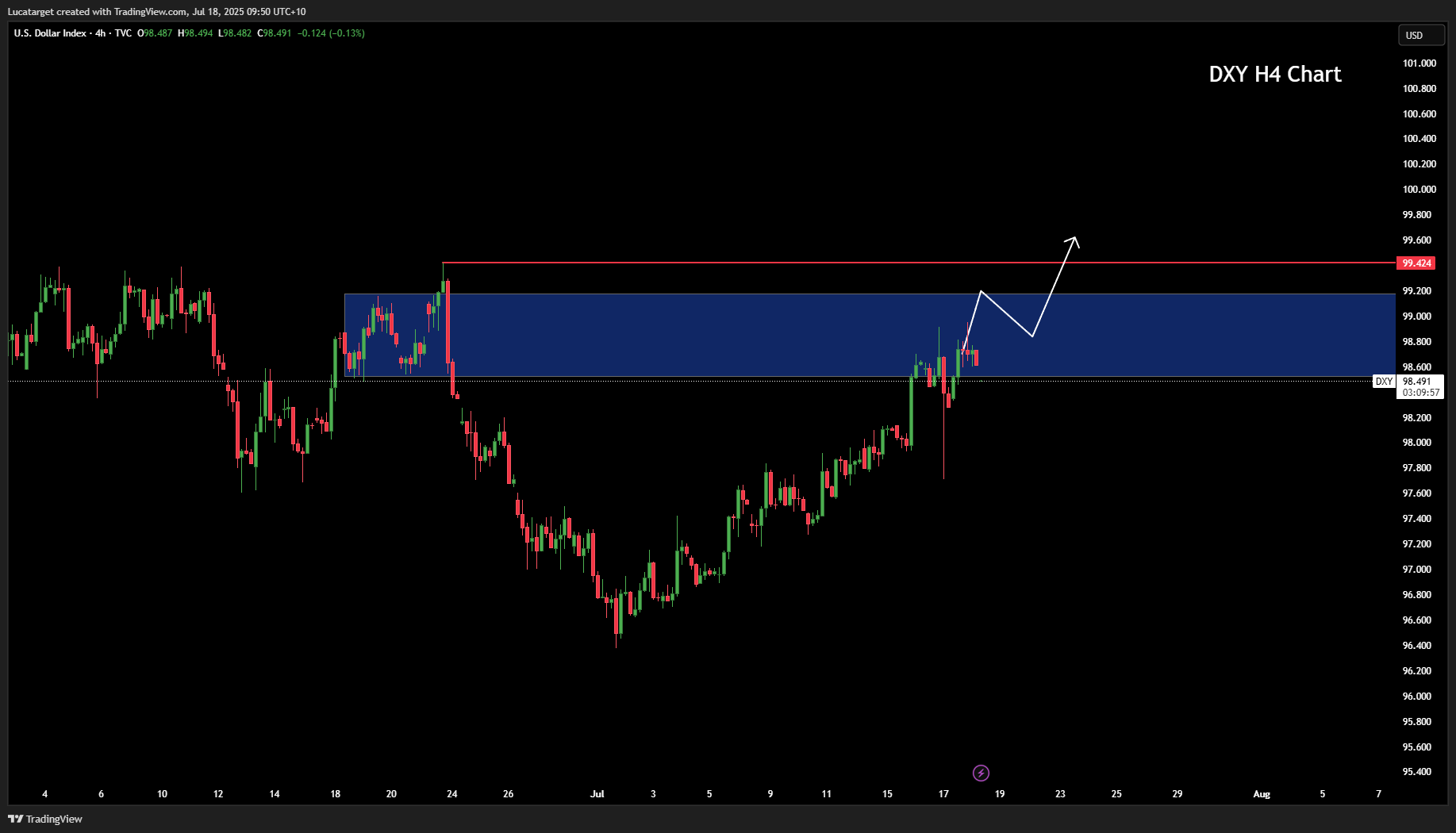

Markets were jolted midweek by a sudden political shock: reports emerged that President Trump considered firing Federal Reserve Chair Jerome Powell.

Although the White House quickly walked back on this narrative, the damage was already done yield curves steepened, equities dipped, and the dollar took a sharp hit before partially recovering.

This episode serves as a stark reminder that political interference in monetary policy remains a real risk to the Fed's independence, and by extension, to USD stability.

But Thursday opened with calmer markets, and the dollar regained some ground, bolstered by cross-asset stabilization and cautious optimism ahead of U.S. economic data.

Even though Powell’s dismissal remains speculative, the incident underscored a broader risk premium markets may begin to price into the dollar: institutional independence under strain.

The widening of U.S. inflation expectations and a steeper yield curve suggest that the market is already adjusting to this possibility.

If political influence becomes a recurring theme, the USD could face more structural headwinds over the coming months.

The euro came under pressure, even as eurozone inflation figures confirmed earlier estimates, holding steady at 2.0% year-over-year.

The real drag, however, appears to be the persistent lack of progress on EU-U.S. trade negotiations. With Brussels signaling readiness to counter U.S. tech interests via taxation and investment curbs, geopolitical friction could weigh on EUR sentiment.

Despite that, expectations of an ECB rate hold continue to anchor support in the medium term.

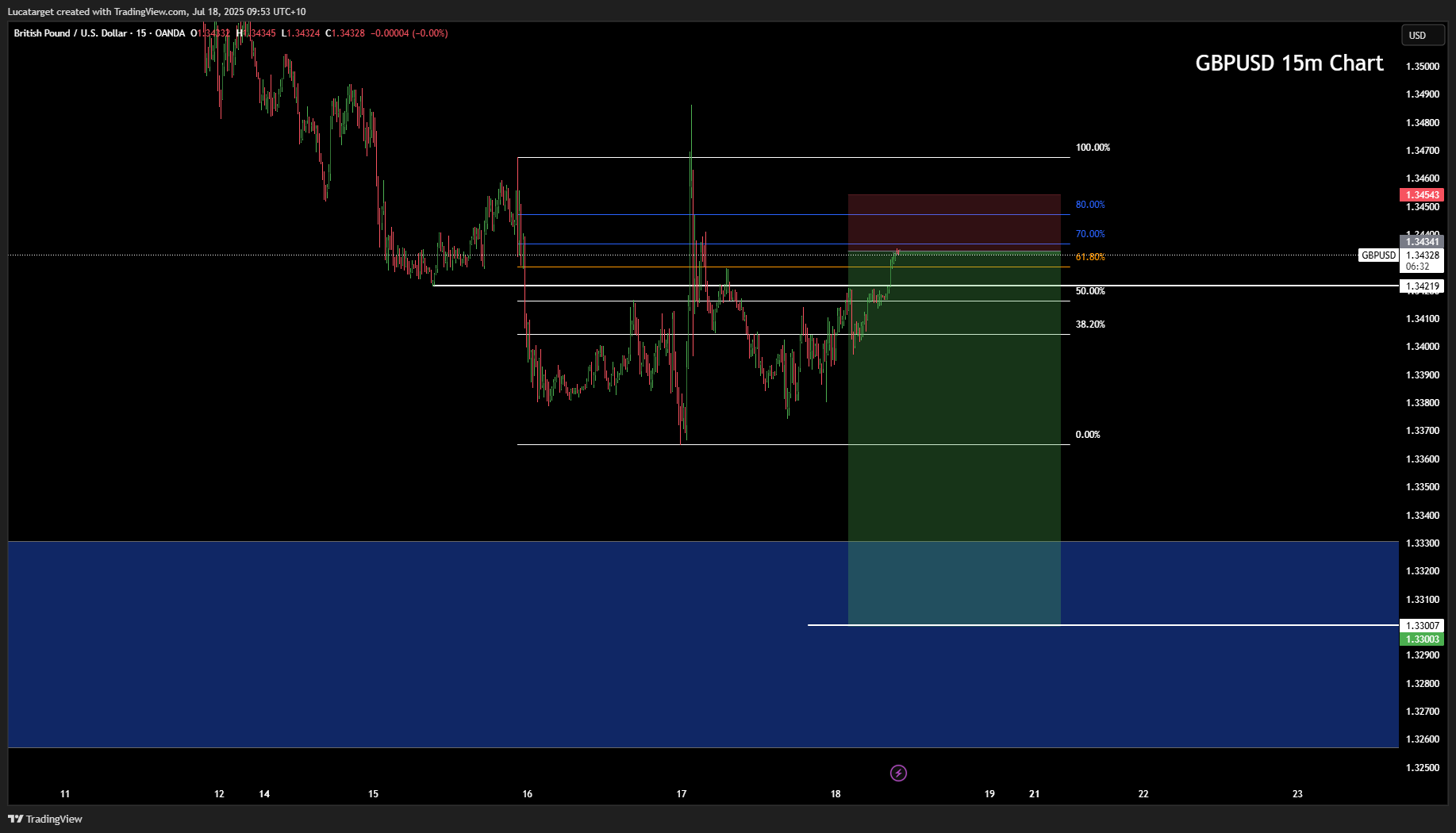

Sterling outperformed its G10 peers after stronger-than-expected U.K. labor data, particularly wage growth. This comes as a relief for the Bank of England, which has cited employment trends as central to its policy direction.

Markets are now less convinced that rate cuts will materialize in the short term, offering support to the pound. However, technical indicators suggest caution: the pair has broken below key moving averages, indicating that downside risks remain.

The Canadian dollar declined, driven less by domestic developments and more by a resurgent greenback. U.S. dollar strength overshadowed narrowing U.S.-Canada rate differentials, despite the two-year yield spread favoring CAD more than it has since December.

Fair value estimates continue to point toward a slightly stronger loonie, but momentum in the USD remains the overriding force for now.

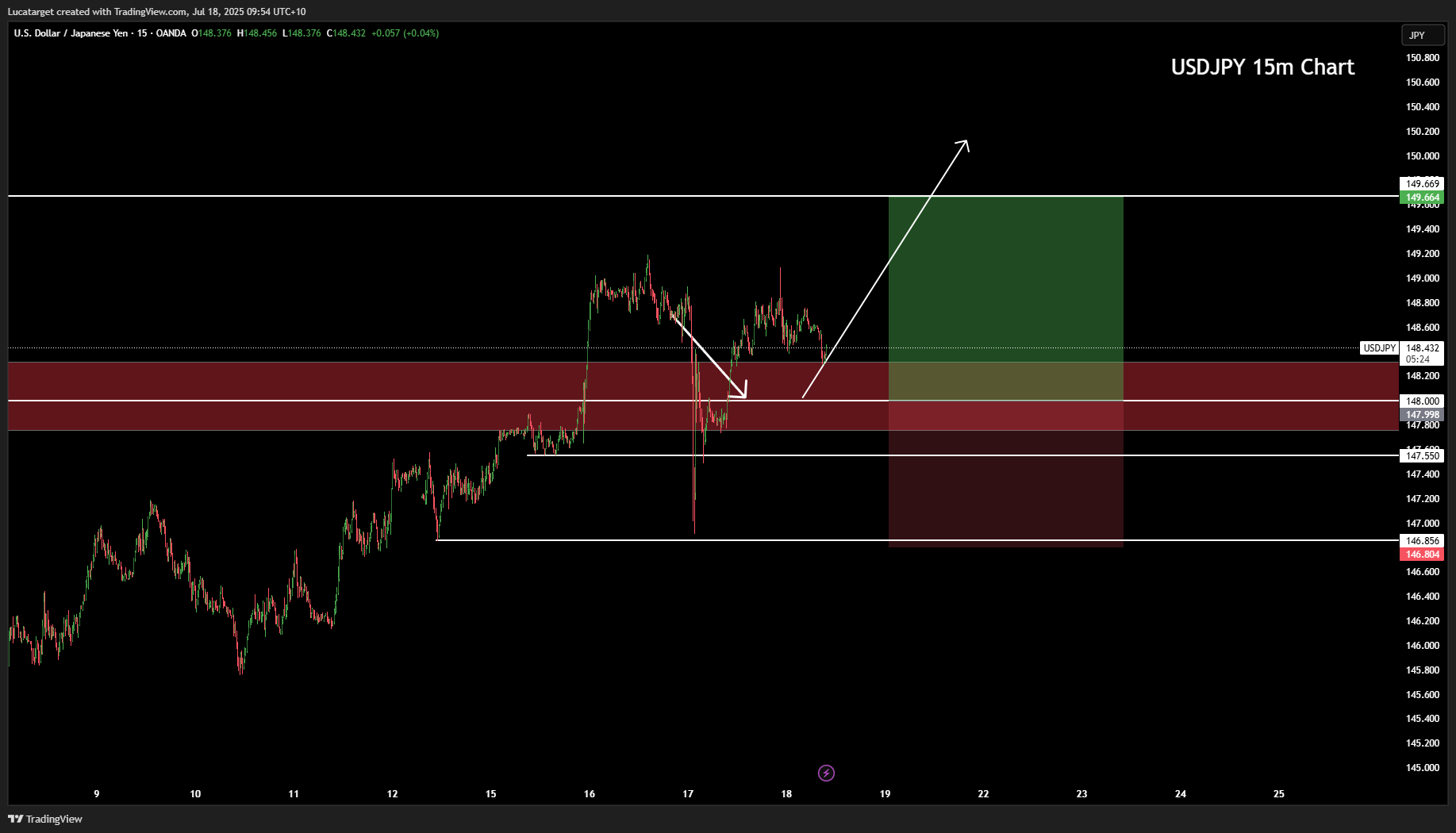

The yen lagged as Japan posted weak trade data and braced for upper house elections. An unexpected drop in exports added to economic uncertainty, while local banks expressed concern over sovereign credit ratings.

With the options market showing reduced demand for JPY downside protection, short-term risks appear skewed to further weakness. All eyes are now on upcoming CPI data, which may offer clarity on the BoJ’s next steps.

Australian job numbers disappointed, reviving speculation of a potential RBA rate cut next month. This sent the Aussie nearly 1% lower, marking it as the worst-performing G10 currency on the day.

As domestic growth prospects dim, and external headwinds from China persist, the AUD may continue to struggle without a material shift in economic momentum.

Markets remain sensitive to any signs of political overreach into central bank independence. As long as this remains a live issue, the dollar may trade with elevated volatility and reduced conviction, even amid supportive data.

Meanwhile, currency-specific narratives are diverging. While some economies are anchored by labor resilience (U.K.), others face downside risks from external trade disputes (EU) or domestic softness (Australia, Japan). The interplay between monetary policy credibility and geopolitical friction will likely define near-term currency performance.

Q: Why did the USD initially fall and then rebound this week?

A: The dollar came under pressure after reports suggested President Trump considered firing Fed Chair Powell raising fears over central bank independence. However, markets stabilized after the White House denied the move, and the USD rebounded as traders refocused on fundamentals like inflation swaps and Treasury yields.

Q: What’s weighing on the euro despite steady inflation?

A: Even though eurozone CPI came in as expected at 2.0%, the euro weakened due to stalled progress in EU-U.S. trade talks. The EU’s potential retaliatory measures against U.S. tech companies have raised geopolitical tension, dampening investor appetite for EUR exposure.

Q: How did U.K. labor data impact the pound?

A: Positive surprises in wage growth and job creation helped the pound outperform peers. While markets still expect one rate cut from the BoE by year-end, the stronger labor report has softened near-term easing expectations, offering support to GBP.

Q: What explains the Canadian dollar's underperformance?

A: The loonie slipped primarily due to broad USD strength. This happened despite narrowing U.S.-Canada yield spreads, which typically support CAD. Fair value models still suggest the CAD is undervalued, but momentum remains USD-driven for now.

Q: Why is the Japanese yen under pressure ahead of the weekend?

A: Weak trade data, credit rating concerns, and uncertainty surrounding the upper house elections are all weighing on JPY. The market is also anticipating softer CPI data, and with little demand for downside protection in options markets, JPY remains vulnerable in the short term.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sterling steadies after political uncertainty rattled gilt markets, while EUR/USD and EUR/GBP approach key technical levels ahead of today's European session.

GBP/AUD remains trapped in a well-defined bearish trend on both the weekly and daily timeframes.

Discover the key drivers, technical levels, and central bank expectations shaping the EUR/USD trend as the ECB prepares to hold rates and markets watch for a potential breakout.

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.