just now

Liquidity Finder Ltd is incorporated in England and Wales, company number 10610740, registered address 167-169 Great Portland Street, Fifth Floor, London W1W 5PF, United Kingdom.

Published: just now

I woke up to a market re-pricing that feels more about policy signalling than data surprises. The yen led in Asia, with USD/JPY slipping back toward the mid-146s and rigth after coming back to 147s after the Jobless Claims release from USA, as traders leaned into the idea that BoJ normalization is not done.

The immediate catalyst was ongoing chatter around Tokyo’s communications framework and whether the Bank shifts emphasis from “underlying inflation” to realised price dynamics, subtle, but the kind of tweak that invites markets to price additional hikes at the margin.

Layer on Washington’s persistent push for easier Fed policy and a stronger yen narrative has oxygen, at least tactically.

In Europe, the UK printed a sturdier-than-feared Q2: +0.3% q/q (after +0.7% in Q1) with June GDP +0.4% m/m. That mix doesn’t scream boom, but it does complicate the case for rapid BoE easing, especially with services momentum still carrying weight.

Markets have faded some of the cut pricing and the pound has been bid on the crosses as a result. For me, the takeaway isn’t that growth is taking off; it’s that Britain’s cyclical floor held into summer, keeping the BoE in “data-dependent dawdle” mode rather than a pre-set quarterly cutting cycle.

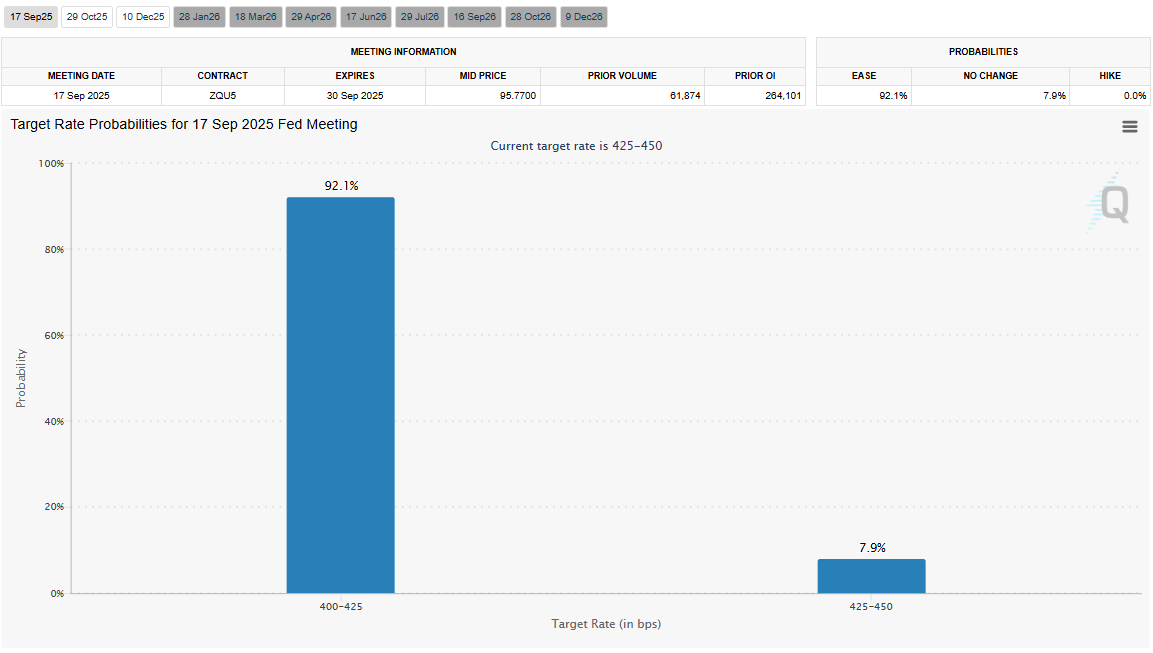

Across the Atlantic, the debate has pivoted from “if” to “how much” the Fed delivers in September. Treasury messaging has leaned openly dovish through July, and while money markets are comfortable with 25bp, the rhetorical space for a larger opening move remains part of the narrative.

My base case: the Fed opts for a conventional 25bp in September unless incoming inflation (PPI/CPI) and labour prints roll over more abruptly; the bar for 50bp is higher and would likely require a clean downside shock across both prices and jobs in the next few weeks.

JPY: I prefer to fade sharp USD/JPY rallies into 147–148 while the market stress-tests the BoJ’s guidance. Wage trends and the BoJ’s communication tweaks matter more than spot intervention rumours; if the Bank nudges its narrative toward realised inflation and tolerance for further normalisation, rate differentials can grind in JPY’s favour without fireworks. Risk: a hawkish Fed repricing that re-widens the front-end spread.

GBP: With Q2 growth firm enough to avoid a “must-cut” narrative, I like GBP on dips vs. low-beta Europe (e.g., EUR/GBP rallies toward 0.87 look sellable) while we wait for UK services and pay data to confirm. If UK domestic demand wobbles in Q3, this view softens, but for now the BoE can afford patience.

The yen’s bid, the UK’s sturdier growth prints, and the Fed’s open debate over the size of its September move are not isolated stories, they’re different expressions of the same market mood: policy is in transition, but the pace and scale remain contested.

In this environment, patience matters as much as positioning. I’m staying tactical rather than directional, letting the data decide the next sustained move, and looking to exploit short-term dislocations rather than make long-term bets on imperfect signals.

Q1: Why did the yen strengthen today?

A: The move was driven by speculation that the Bank of Japan may shift its policy language toward realised inflation, which traders interpret as keeping the door open for further policy normalisation.

Q2: How does UK growth affect Bank of England policy?

A: Stronger-than-expected GDP reduces the urgency for rapid rate cuts, giving the BoE room to move cautiously and remain data-dependent.

Q3: What is the market expecting from the Fed in September?

A: Most pricing is for a 25bp cut, but softer inflation and labour data in the coming weeks could revive talk of a larger 50bp move.

Q4: How do these policy shifts impact currency markets?

A: Currency values often move on relative interest rate expectations, when one central bank is seen tightening or staying on hold while another moves toward easing, rate differentials adjust and drive FX flows.

Q5: What’s the main takeaway for traders right now?

A: This is a period of policy transition across major economies, which means opportunities will come from short-term dislocations rather than long, one-directional trends.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis.

Select the categories and companies you wish to follow directly to your person rss feed.

Create Custom RSS FeedSign up and join over 5,000 professional members who receive personalized news alerts, curated professional connections, and more for free!

Sydney-based multi-asset broker ACY Securities has introduced PAXGUSD, a new CFD instrument that allows clients to trade tokenised gold against the US Dollar 24 hours a day, seven days a week. The instrument is available across MetaTrader 4, MetaTrader 5, and the ACY Trading Platform.

Binance has lowered its VIP 3 Wallet Assets threshold from $3 million to $1 million and will now count OTC Spot Trading Volume at a 4x multiplier toward VIP qualification, removing the previous VIP 4 cap and allowing eligible users to progress through the full tier framework up to VIP 9.

Retail futures trading leader NinjaTrader Group has appointed Mark Omens as Senior Vice President, Commercial Strategy, bringing a 25-year veteran of derivatives marketplace CME Group into a newly created role focused on exchange partnerships and enterprise growth.

Gold Price Action Forecast: Will XAU/USD Drop to $3930? Meta Description: Read our Gold price action forecast to see if XAU/USD will drop to $3930.

BitDelta Securities Financial Services LLC (“BitDelta Securities”) today announced that it has received full regulatory approval from the Capital Market Authority (“CMA”) of the United Arab Emirates under the Category 5 — Arrangement and Advice license framework (License No. 20200000439). The approval follows the firm's receipt of In-Principal Approval earlier this year and represents the successful conclusion of the CMA's full licensing process, including the satisfaction of capital requirements, governance appointments, and operational setup.

Crypto.com has received a $400 million strategic investment from Citadel Securities, valuing the firm at $20 billion. It marks the first institutional funding round in the company's history, aimed at accelerating its expansion into tokenised securities, derivatives and other asset classes.

WTI’s pullback into $79–82 is the first major test of the bullish Elliott Wave count, with buyers targeting a renewed break above $85.

BitDelta Securities has secured a full CMA Category 5 licence in the UAE and opened a regulated office in Business Bay, Dubai. The firm operates as an introducing broker, connecting investors with licensed international brokers across multiple asset classes, with CEO Dr. Demetrios Zamboglou commenting on the milestone.

Index volatility is asleep while single stocks fight it out underneath, credit refuses to confirm the equity rally, and a bare macro calendar hands next week to oil.

Digital assets and FX brokerage GC Exchange FZE (GCEX) has appointed Mohammed A. Mulla as a Board Member of its Dubai-based entity, part of the wider GCEX Group.